5.26 The Dance of Volume and Price

Volume does not tell you direction, it tells you whether the move sticks. High volume means continuation, low volume means reversion. Use it as the regime switch on a directional signal, not as the signal.

Volume is the cheapest piece of information on the tape and the most underused. It tells you not where price is going but whether the next move is likely to stick or snap back. Predict volume and you get a conditional read on price: high volume tends to carry a move forward, low volume tends to let it revert. That conditional split is the trade.

Start with what volume is. It is the sum of trade sizes in a period, so it lives downstream of trades, the executed liquidity the old article "Using Trade Flow to Predict Short-Term Price Movement" treats as the maker's core signal. Trade flow signs that activity into buys and sells; raw volume throws the sign away and keeps the magnitude. The magnitude alone, it turns out, already carries a usable continuation-versus-reversion signal.

How volume behaves

Three statistical facts set up everything else, and none of them are exotic.

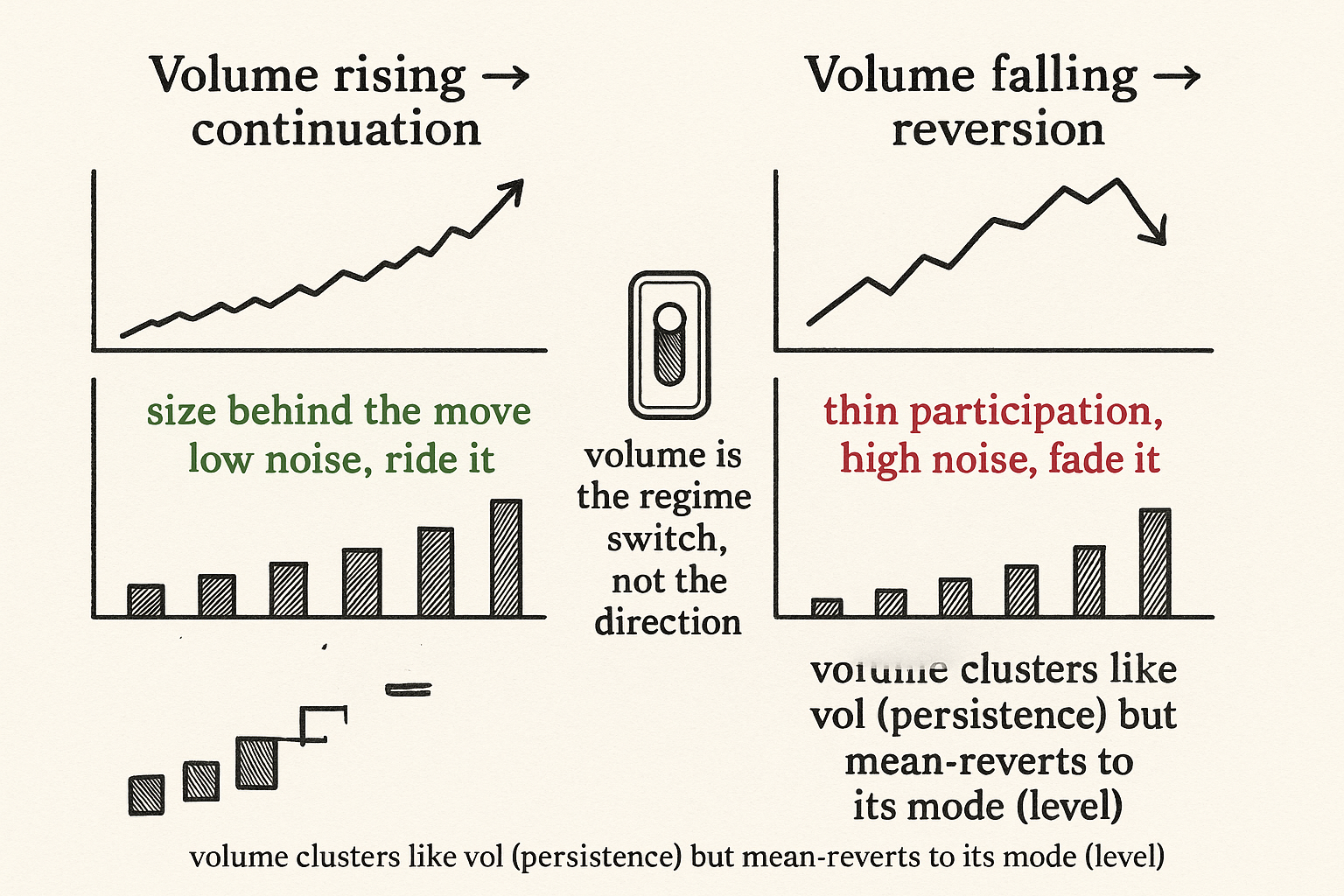

Volume clusters and has fat tails, the same shape as volatility. Quiet stretches sit near a low baseline, then a burst arrives and drags a run of high-volume bars behind it. So volume is forecastable in the weak sense that a high bar makes the next bar more likely high, the persistence you would model with the same machinery as vol.

Volume tracks the number of trades, but not linearly. For large trade counts the relationship is roughly linear; below that it bends, with positive convexity, because a handful of large trades can post big volume on few executions while many tiny trades post modest volume on high count. So volume and trade count are strongly correlated and not interchangeable, and which exchange's volume you use depends on what you are predicting, since the books differ.

Volume mean-reverts to its mode. Regress this bar's volume on last bar's and the slope pulls toward the center: a high bar tends to be followed by a lower one, a low bar by a higher one, both drifting back to the typical value. Persistence in the clusters, reversion in the level. Both are true at once because they describe different horizons.

The price link

The bridge to price is one observed regularity: price is more volatile when volume is high. More executed size means more information and more impact hitting the book, so the move is larger and, more usefully, more likely to be real rather than noise. The old article "Noise Is Not Volatility" is the tool that makes this precise: volatility is how far price travels, noise is how much of that travel cancels before producing net direction. High volume tends to come with cleaner, lower-noise travel, a move that nets out somewhere; low volume tends to come with high-noise chop that cancels.

That gives the conditional rule.

$$ \text{Volume} \uparrow \;\Rightarrow\; \text{continuation (price keeps going)} $$ $$ \text{Volume} \downarrow \;\Rightarrow\; \text{reversion (price snaps back)} $$

Read it as a regime switch on the magnitude of volume. When volume is rising, treat the current move as a trend to ride, because the size behind it says the move has backing and lower noise. When volume is falling, treat the current move as overextension to fade, because thin participation says the travel is noise that cancels. Volume is not the direction signal; it is the switch that tells you whether to apply a momentum rule or a reversion rule to whatever direction price is already showing.

Turning it into something tradable

The rule needs a volume forecast to act ahead of the move rather than after it. Use the two facts above: persistence says a high recent bar predicts a high next bar, reversion says an extreme bar predicts a pull toward the mode. A simple forecast blends them, predicting next-bar volume from recent bars while pulling extremes back toward the typical level. Then condition: if forecast volume is rising relative to its mode, run the continuation leg in the direction of the recent return; if forecast volume is falling, run the reversion leg against it.

Be honest about the limits. This is a coarse, two-state switch sitting on top of a noisy volume forecast, and volume's exchange-dependence means a signal fit on one venue's tape can evaporate on another. The continuation-reversion split is a real conditioning variable, not a standalone alpha; it sharpens a directional rule you already have by telling you which regime you are in, the same way the old article "Noise Is Not Volatility" uses the noise axis to pick the game while volatility only sizes the bet. Treat volume as the column that picks momentum versus reversion, and your existing signal as the bet inside it.

Visualizing the switch

KEY POINTS

- Volume is the sum of trade sizes, downstream of the trade flow from "Using Trade Flow to Predict Short-Term Price Movement," but it keeps magnitude and drops the buy/sell sign. The magnitude alone carries a continuation-versus-reversion read.

- Volume clusters with fat tails like volatility (persistence), tracks trade count nonlinearly with convexity at low counts, and mean-reverts to its mode (a high bar tends to be followed by a lower one). Persistence and reversion describe different horizons and both hold.

- Price is more volatile when volume is high, and high volume tends to mean lower-noise travel. "Noise Is Not Volatility" makes this exact: high volume carries cleaner net direction, low volume carries chop that cancels.

- The conditional rule: volume up means continuation (ride the move), volume down means reversion (fade it). Volume is the regime switch applied to whatever direction price already shows, not the direction itself.

- To trade it, forecast next-bar volume by blending persistence (high follows high) with mean reversion (extremes pull to the mode), then pick the momentum or reversion leg from that forecast.

- Limits: a coarse two-state switch on a noisy, exchange-dependent volume forecast. It sharpens an existing directional signal by naming the regime; it is not a standalone alpha.

References

- Trading Volume and Serial Correlation in Stock Returns (Campbell, Grossman, Wang)

- Volume, Volatility, and Price Continuation versus Reversal

- The Clustering and Fat Tails of Trading Volume

- Volume-Conditioned Momentum and Mean Reversion in Crypto

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Causality between Trading Volume and Returns: Evidence from Quantile Regressions

- Trading Volume and Prediction of Stock Return Reversals: Conditioning on Investor Types’ Trading

- Mean Reversion in Trading Volume and Informational Efficiency

- Limit Order Book Shape and Return Distribution

- Short-Horizon Excess Returns in Liquid Equities

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

- Order-Flow Filtration and Directional Association with Short-Horizon

- Persistence or reversal? The effects of abnormal trading volume on