5.27 NYSE-Open Volume Momentum

When New York opens, a volume surge hits crypto. From 13:30 to 15:00 UTC, if volume keeps rising, ride the sign of the first half hour to the close of the window. Track the real open, not a frozen timestamp.

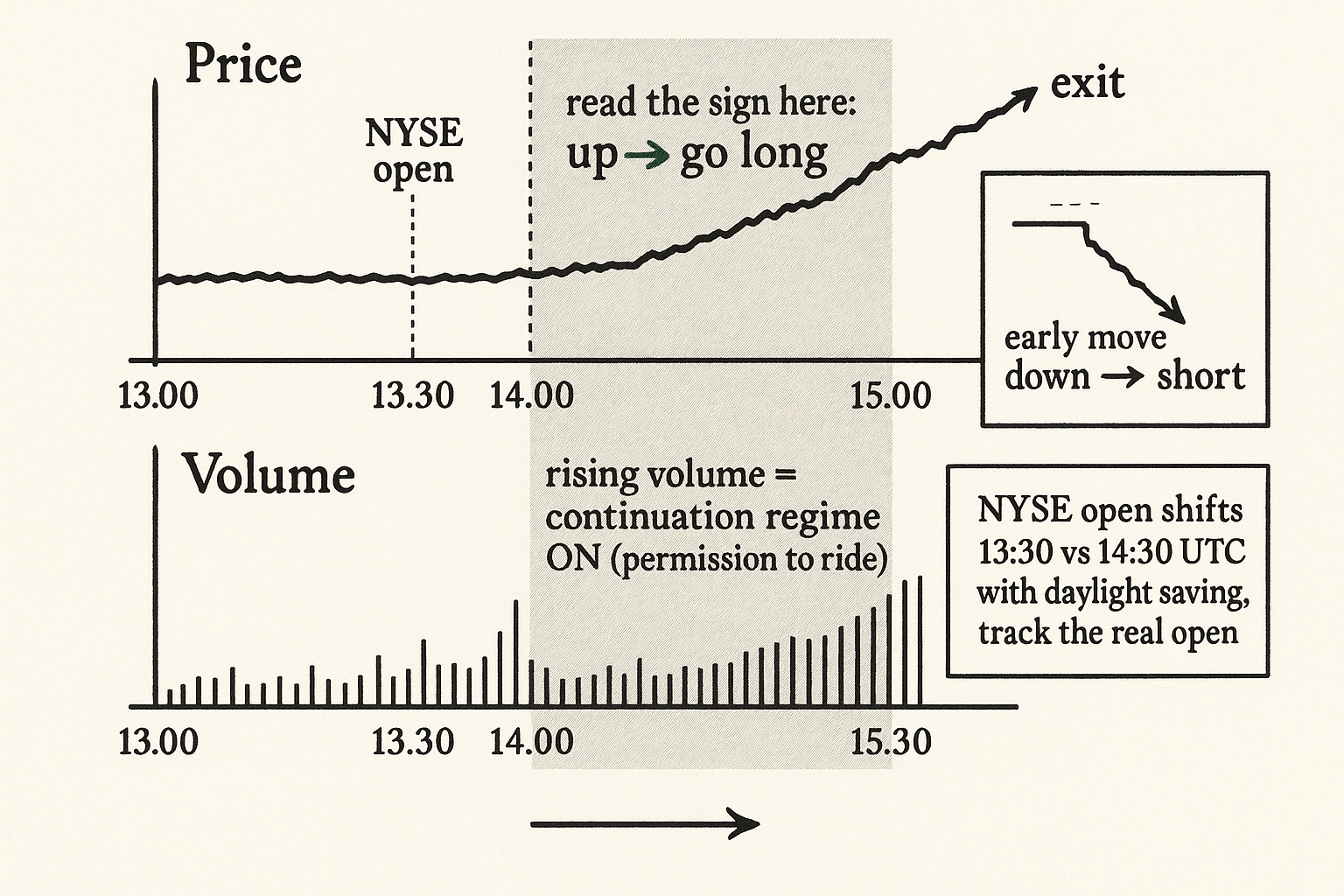

Crypto trades around the clock, but it does not trade evenly. When New York equities open, a wave of attention and flow hits the crypto book, and for the next ninety minutes the tape behaves differently than it does at 04:00 UTC. The specific claim is narrow and testable: from roughly 13:30 to 15:00 UTC, if volume keeps rising, price tends to trend, and the direction of the first half hour sets the direction for the rest of the window.

This is a time-of-day strategy, which means the old article "How to Choose the Right Timeframe for a Strategy" is the governing constraint. That piece argued the timeframe decides whether you see trend or chop, because noise itself is a function of timeframe and the window you pick is upstream of the trend-versus-reversion choice. Here the window is fixed by an external clock, the NYSE open, and the bet is that this particular window sits on the trending side of the noise threshold while the rest of the day does not.

The setup

The mechanism is the volume conditioning from the old article "The Dance of Volume and Price," pinned to a specific clock window. Rising volume signals continuation; the NYSE open is a reliable, recurring volume surge. Combine them and you get a window where the continuation regime is likely to be switched on, so a directional move that starts the window has backing to carry it.

Two conditions have to hold together. The window is 13:30 to 15:00 UTC. First, volume must be rising through the window, confirming the continuation regime rather than a fading one. Second, the sign of the early move sets the direction.

$$ \text{sign}\big(r_{13{:}30 \to 14{:}00}\big) > 0 \;\Rightarrow\; \text{long until } 15{:}00 $$ $$ \text{sign}\big(r_{13{:}30 \to 14{:}00}\big) < 0 \;\Rightarrow\; \text{short until } 15{:}00 $$

Read it straight: take the return over the first half hour of the window, 13:30 to 14:00 UTC. If it is positive, the open is pushing up, so go long and hold to 15:00. If it is negative, the open is pushing down, so go short and hold to 15:00. The early move is your direction read; the rising volume is your permission to treat it as momentum instead of fading it. Without the volume confirmation you are buying a thirty-minute move with no reason to think it continues, which is the chop the timeframe article warns the wrong window hands you.

Why this connects to flow

The deeper reason the open trends is order flow, the subject of the old article "Using Trade Flow to Predict Short-Term Price Movement." The NYSE open brings a burst of takers into crypto, and takers move price and cluster, buys following buys. A surge of one-sided taking on the book at a predictable time is the cleanest version of the continuation signal: you know roughly when the flow arrives (the open), you confirm it is arriving (rising volume), and you read its direction from the first thirty minutes. The strategy is a structured way to ride a recurring, time-stamped burst of taker flow.

Where it breaks

Be blunt about the soft spots. The "NYSE open" is not a fixed UTC time across the year, because US daylight-saving shifts the open between 13:30 and 14:30 UTC, so a hard-coded window will be an hour off for part of the year and you must track the actual open, not a frozen timestamp. The effect is also a crowded, well-documented intraday pattern, so the edge net of fees on a ninety-minute hold is thin and decays as more desks trade it. And it is a directional bet inside a single narrow window, so the sample of independent days accumulates slowly, which the timeframe article flags as the cost constraint: few trades means slow confirmation and a long wait to know whether the edge is real or you are reading noise from a handful of strong opens. Confirm the rising-volume condition is doing real work by testing the rule with and without it; if the volume filter does not improve the result, you are trading a plain open-momentum rule and should admit it.

Visualizing the window

KEY POINTS

- From about 13:30 to 15:00 UTC, when volume keeps rising, crypto price tends to trend, and the sign of the first half hour (13:30 to 14:00) sets the direction held to 15:00.

- This is the volume-continuation switch from "The Dance of Volume and Price" pinned to the recurring volume surge at the NYSE open: rising volume turns on the continuation regime, so the early move has backing to carry.

- The rule needs both conditions: volume rising through the window (regime confirmation) and the early-move sign (direction). Without the volume filter you are fading or chasing a thirty-minute move with no reason it continues.

- It works because the open brings a burst of clustered taker flow, the continuation logic of "Using Trade Flow to Predict Short-Term Price Movement," at a predictable, time-stamped moment.

- Time-of-day strategy, so "How to Choose the Right Timeframe for a Strategy" governs: the bet is that this window sits on the trending side of the noise threshold while the rest of the day does not.

- Breaks: the open shifts 13:30 vs 14:30 UTC with daylight saving (track the real open), the pattern is crowded and decays, and one narrow window per day accumulates independent samples slowly. Test with and without the volume filter to prove it earns its keep.

References

- How to Choose the Right Timeframe for a Strategy (old article)

- Intraday Momentum and the Market Open Effect

- Spillover of US Equity Market Open into Cryptocurrency Returns

- Volume and the Predictability of Intraday Returns

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Price Momentum and Trading Volume

- Trading volume and prediction of stock return reversals: Conditioning on investor types' trading

- Intraday return predictability in the cryptocurrency markets

- Deep Limit Order Book Forecasting A microstructural guide

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with Predictive Information

- Adverse selection in cryptocurrency markets

- Limit Order Book Shape and Return Distribution

- Market Simulation under Adverse Selection - arXiv