2.76 The Limits of Linear Models

The clean linear factor model fails because its weights are not constants. Momentum and carry only pay in the right vol regime, and interactions are the one thing a linear model cannot represent.

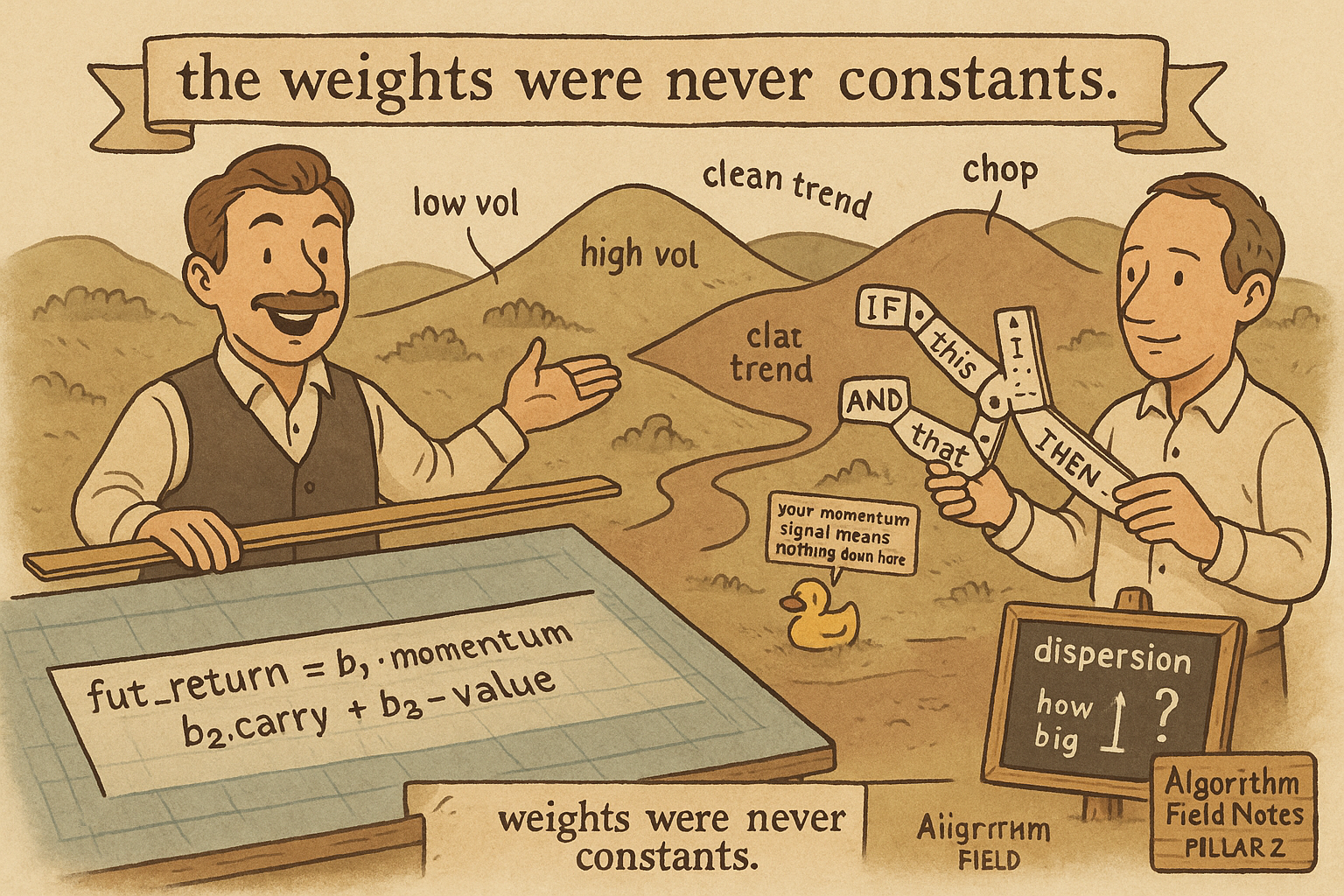

Write down the model every quant writes in their first month predicting cross-sectional returns. You take three signals, momentum, carry, and value, and you weight them.

$$ \text{fut\_return} = b_1 \cdot \text{momentum} + b_2 \cdot \text{carry} + b_3 \cdot \text{value} $$

You fit the three weights on history, you get a positive in-sample R-squared, and you feel like you have found something. The model is clean, the algebra is honest, and the fit looks real. It is also wrong in a way that no amount of data will fix, and the reason it is wrong is the whole subject of this article.

Quant equity desks moved off plain linear factor models as their final word years ago. They still run them as baselines and as components. They stopped trusting them on their own, because the relationship between a signal and the next return is not a fixed number. It is a number that changes with the regime.

The weights are not constants

Momentum, the trend signal, does not pay equally in all conditions. The same context dependence shows up at every frequency: the old article "Order Book Imbalance: The First Microstructure Feature to Test" makes the point for a microstructure feature, and momentum behaves the same way at medium frequency. In a low-volatility regime with a clean, persistent trend, momentum is a strong signal: the move has direction and it keeps going. In a high-volatility chop, the same momentum number means almost nothing, and past some level of stress it reverses, because crowded trends unwind hardest when vol spikes.

So the true coefficient on momentum is not the constant b1. It behaves more like momentum gated by the volatility regime, or momentum scaled by trend strength. The honest model is closer to this.