4.70 Combining Three Weak Alphas on Cointegrated Futures

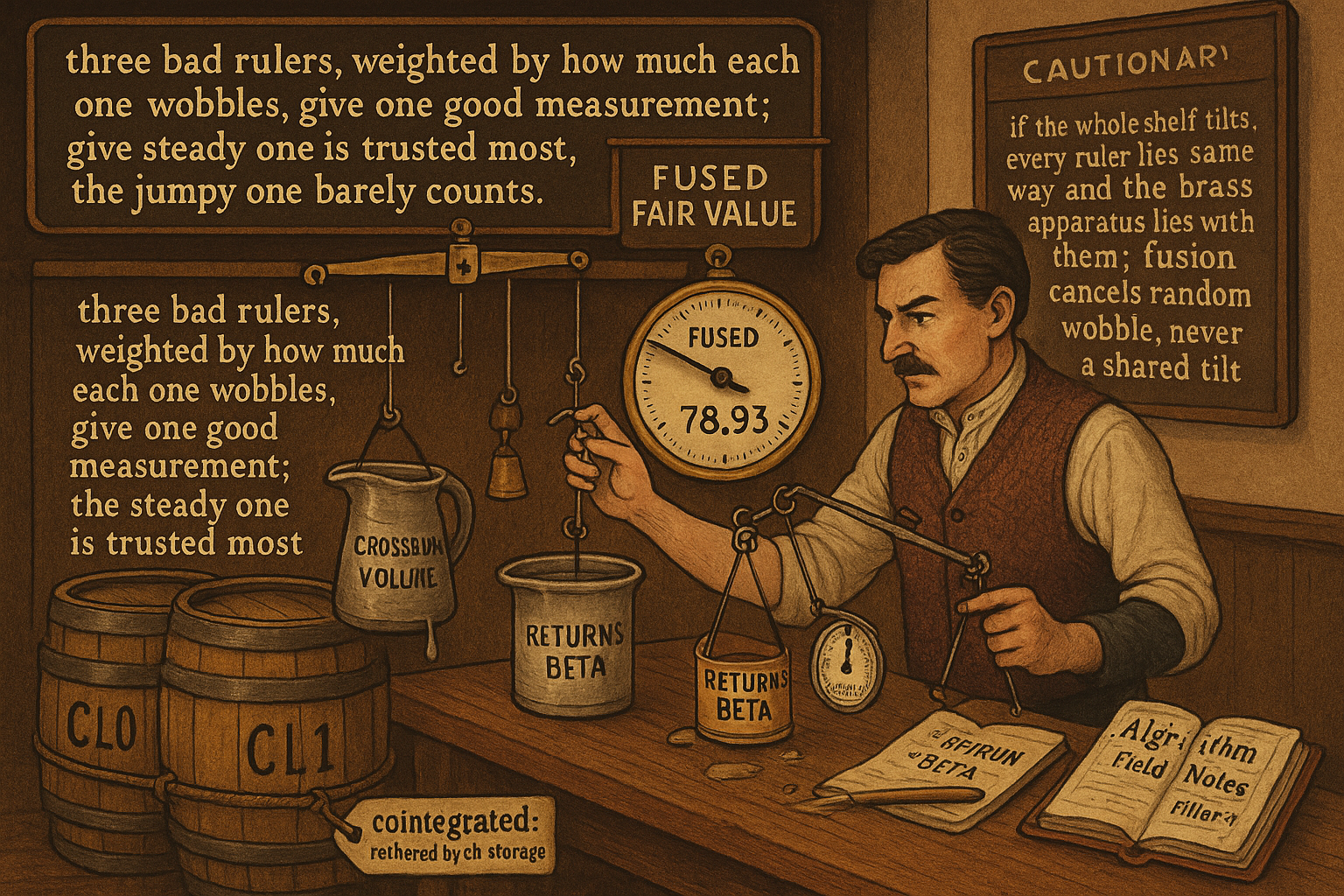

Three fair-value estimators for an adjacent crude future, each too weak alone: spread EMA, returns beta, cross-book volume. Weight each by one over its error variance and the shared signal survives while the noise cancels.

Take CME's WTI crude contract, ticker CL, a contract for physical delivery of light sweet crude at Cushing, Oklahoma. Call the front month CL0 and the next expiry CL1. Right now CL0 trades at 78.40 and CL1 at 78.95, a 0.55 contango. You want a fair value for CL1, the less liquid leg, that is sharper than its own wide, slow quote. Three separate ideas each take a swing at this, and each one, on its own, is too weak to trade. Combine all three and you can price the contract adjacent to the active month well enough to make markets in it. That is the whole exercise: three losers that add up to a winner.

This piece picks up where the old article "Using Ratios as Trading Signals" left off. A ratio nets two correlated series into one rotation signal. Here we go the other way and fuse several noisy estimators of the same fair price into one estimate that is more precise than any input. The intermarket gating from the old article "Intermarket Analysis for System Traders" is a cousin of this, but gating filters; fusion averages.

The setup: why adjacent futures are cointegrated

CL0 and CL1 are claims on the same barrel of oil, separated by one month of carry. The price difference between them cannot wander freely. If CL1 minus CL0 climbs far above the cost of storing oil for a month (warehouse, insurance, financing), a physical trader buys CL0, takes delivery, stores the barrel, and sells CL1 against it, pocketing the gap above storage cost. If the gap collapses too far, the reverse trade pays. Those trades carry frictions, so the spread is not pinned to a single number. It floats inside a band, and inside that band the two prices are cointegrated: they drift apart, then a physical arbitrageur drags them back.

Cointegration is the structural reason any of this works. It is also why the example needs a contract with several expiries trading real volume at once. CL gives you that overlap window. A market where only the front month trades leaves you nothing to fuse.