5.44 MFT Execution Is Built on HFT Market-Making

The cheapest way for an MFT shop to enter a small position is to act like a market maker: feed your quoting engine a phantom short so it skews and fills you long, collecting the spread instead of paying it.

A mid-frequency shop wants to get long 250k of something. The naive move is to cross the spread and take it. The cheaper move, the one the good execution stacks actually use, is to become a market maker for the duration of the entry. Market makers have the best execution in the world for orders of trivially small size, because providing liquidity at a tight spread is their entire business. So the lowest-cost execution systems for MFT shops get built on the HFT side, by borrowing the market-making machinery and pointing it at a single goal: putting on the position instead of staying flat.

"Trivially small size" is the load-bearing qualifier. Once your order is large relative to the venue, a new problem appears, disguising your flow so the market does not front-run your remaining size, and that is a different discipline. Below that threshold, the cheapest way in is to act like the maker who would have quoted you, and capture the spread you would otherwise have paid.

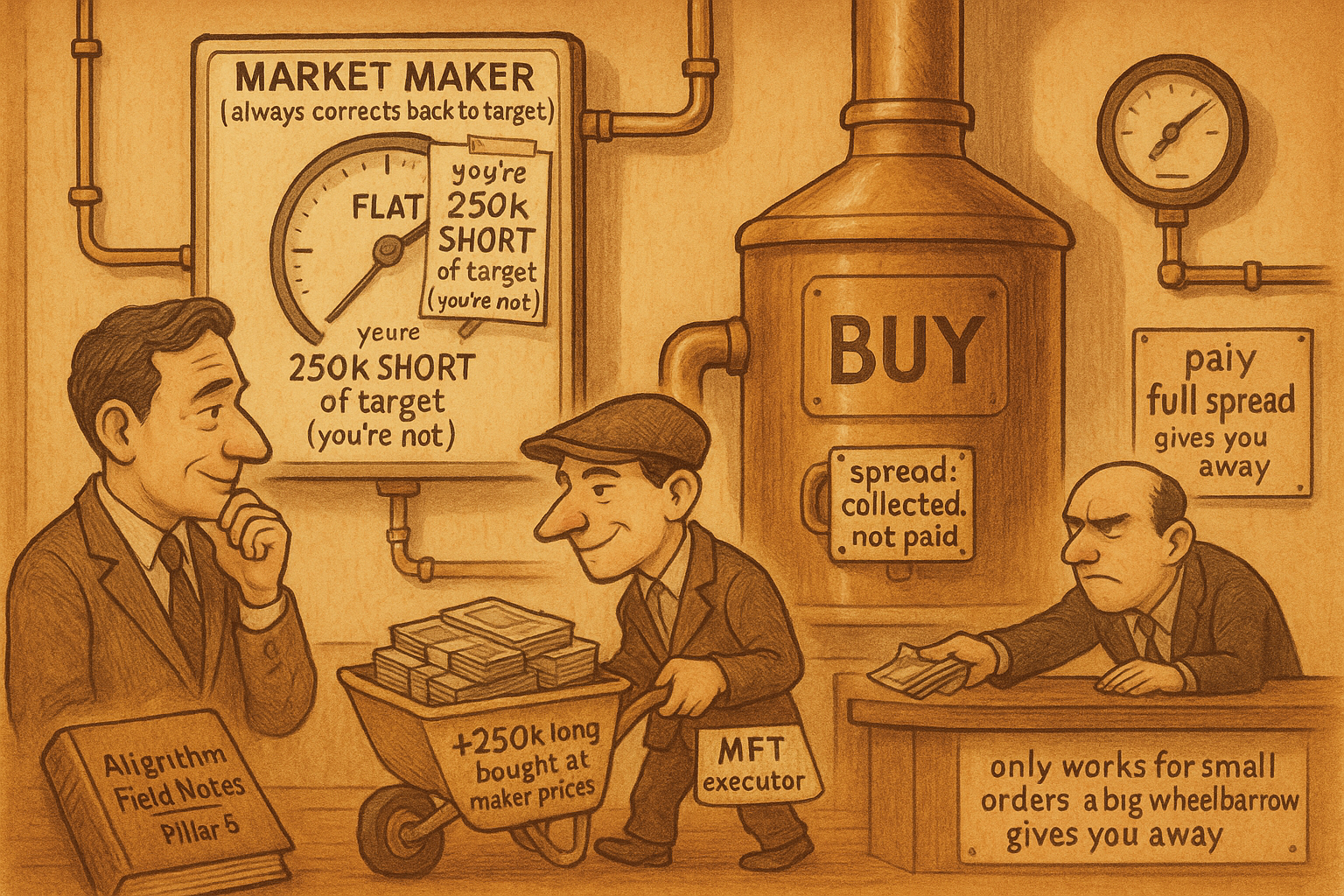

How a maker changes position: skew

To see why this works, recall how a market maker moves its own inventory. A maker quotes both sides. When it wants to shed inventory or pick some up, it skews: one side of the quote sits further from midprice than the other, so the near side fills more often and the far side fills less. The old article "Why Skewing Is Simpler Than People Think" laid out the mechanics, and the old article "Maker vs Taker Edge: Same Signal, Different Economics" laid out why the maker and the taker run opposite businesses off the same view. The maker skews to drag its position back toward zero: the more inventory it holds, the harder it skews to offload it.

Now run that machinery in reverse for execution. You want to put on 250k long. So you tell your market-making engine that it currently holds 250k short. It does not, it holds zero, but the engine does not know that. Believing it is 250k short, it skews hard to its bid side to "get back to zero," resting aggressive passive bids and weak offers. It fills on the buy side, accumulates the long, and as far as it is concerned it is dutifully flattening a short. When it thinks it has reached zero, you are actually long 250k. You have put on the entire position as a maker, collecting spread on every fill instead of paying it.