5.37 Continuous, Event-Driven Trading vs Bar-Based Research

Bar research assumes the clock drives the market. It doesn't, events do. Fixed rebalance times are front-runnable and bars hide execution seasonality. Screen on bars, validate on event-driven sims, trade on events.

Most research runs on bars. You resample the tape to one-minute or one-hour candles, compute features on the close, decide a position, and assume you execute at that close. It is fast, it vectorizes, and the old article "Backtest Integrity Checklist as Code" showed how to keep it honest with shift discipline so you never trade on a bar you could not have seen. Bars are the right tool for screening ideas. But they encode an assumption about time that breaks at the microstructure scale, and a maker who carries the bar habit into live quoting leaves money on the table and hands an edge to anyone watching.

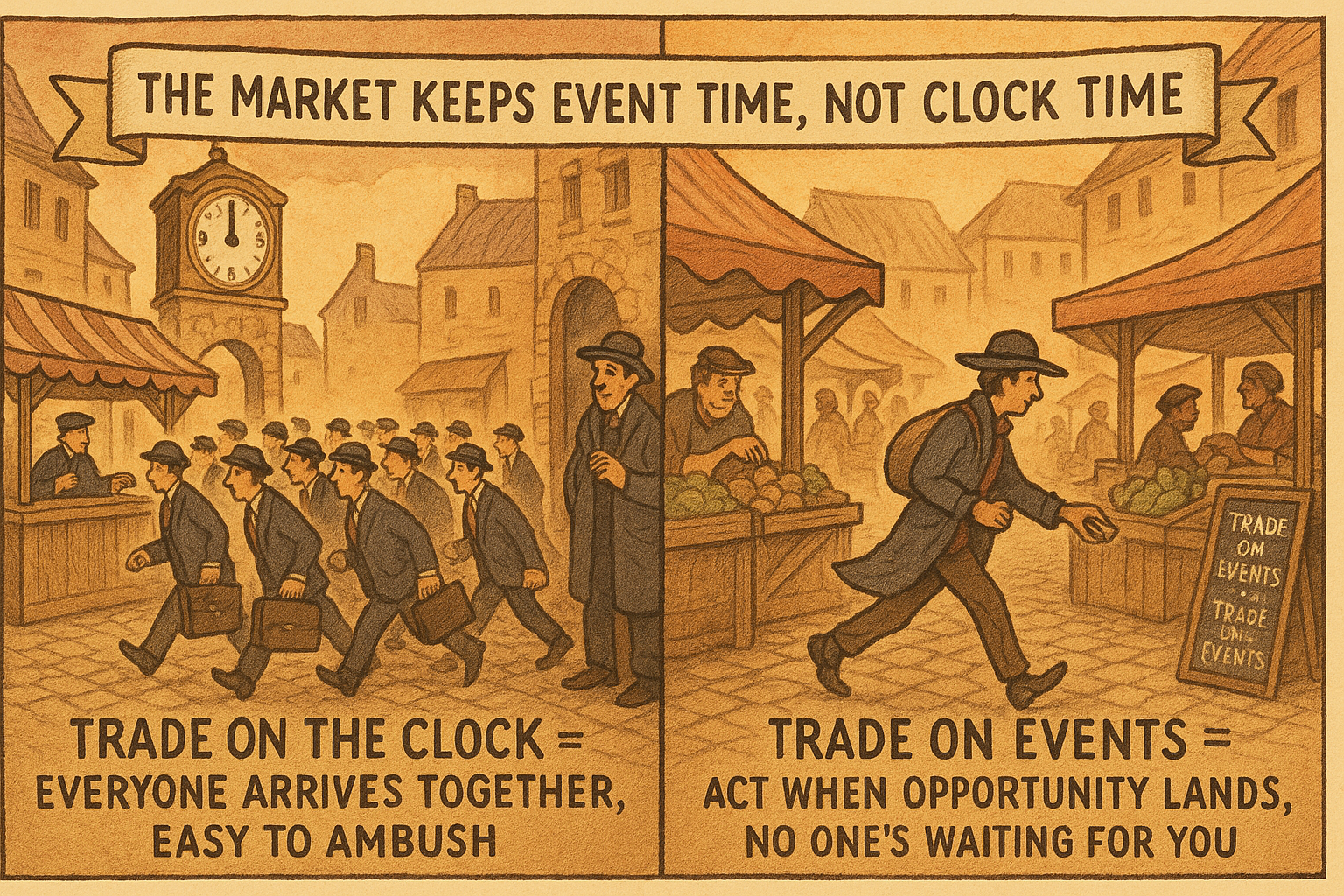

The assumption is that the clock drives the market. Sample every minute, act every minute, as if the interesting moments arrive on a fixed schedule. They do not. Markets move through events, a quote changes, a large order prints, liquidity vanishes, and those events do not wait for your bar to close. This is the intrinsic-time idea: the meaningful clock is the sequence of events, not the wall clock. Bar research forces event-driven reality onto a clock-time grid, and two specific things go wrong.

Problem one: fixed rebalance times are front-runnable

A bar strategy acts at bar boundaries. If you rebalance on the one-hour candle, you trade at the top of every hour. So does a large slice of the market running the same convention. Your order timing is public knowledge before you place it, because everyone knows the hour is about to turn and a wave of mechanical rebalancing is coming.