6.14 Expectancy: The Most Important Formula in Trading

Expectancy is the average win or loss per trade, the one number that says if a system makes money. A 36% win rate can print and a 70% win rate can bleed; only expectancy tells the truth.

Strip a trading system down to one number and that number is expectancy: the average amount you expect to win or lose per trade. Not the win rate, not the size of your biggest winner, not how it felt. Expectancy combines how often you win with how much you win and lose into a single figure that tells you whether the system makes money at all. Traders chase every metric except this one, and a system with a negative expectancy is a machine for converting capital into broker fees no matter how clever the entries look.

This is the anchor for the next several articles. "Why Percent Profitable Is Overrated" and "Profit Factor, Expectancy, and the Shape of Returns" both orbit it, so it is worth getting the arithmetic exactly right first.

The formula and what each piece does

$$ E = \big(P_{\text{win}} \times \text{avg win}\big) - \big(P_{\text{loss}} \times \text{avg loss}\big) $$

Expectancy is the probability of a win times the average winning trade, minus the probability of a loss times the average losing trade. The first term is the money you make from winners weighted by how often they happen; the second is the money you give back to losers weighted by how often they happen. Subtract and you get the average result of a single trade, in dollars or in R-multiples. A positive expectancy means the average trade adds to your equity; a negative one means the average trade subtracts from it. Every other performance metric is a way of looking at one slice of this number; expectancy is the whole thing.

A worked example, because the formula hides the trade-off

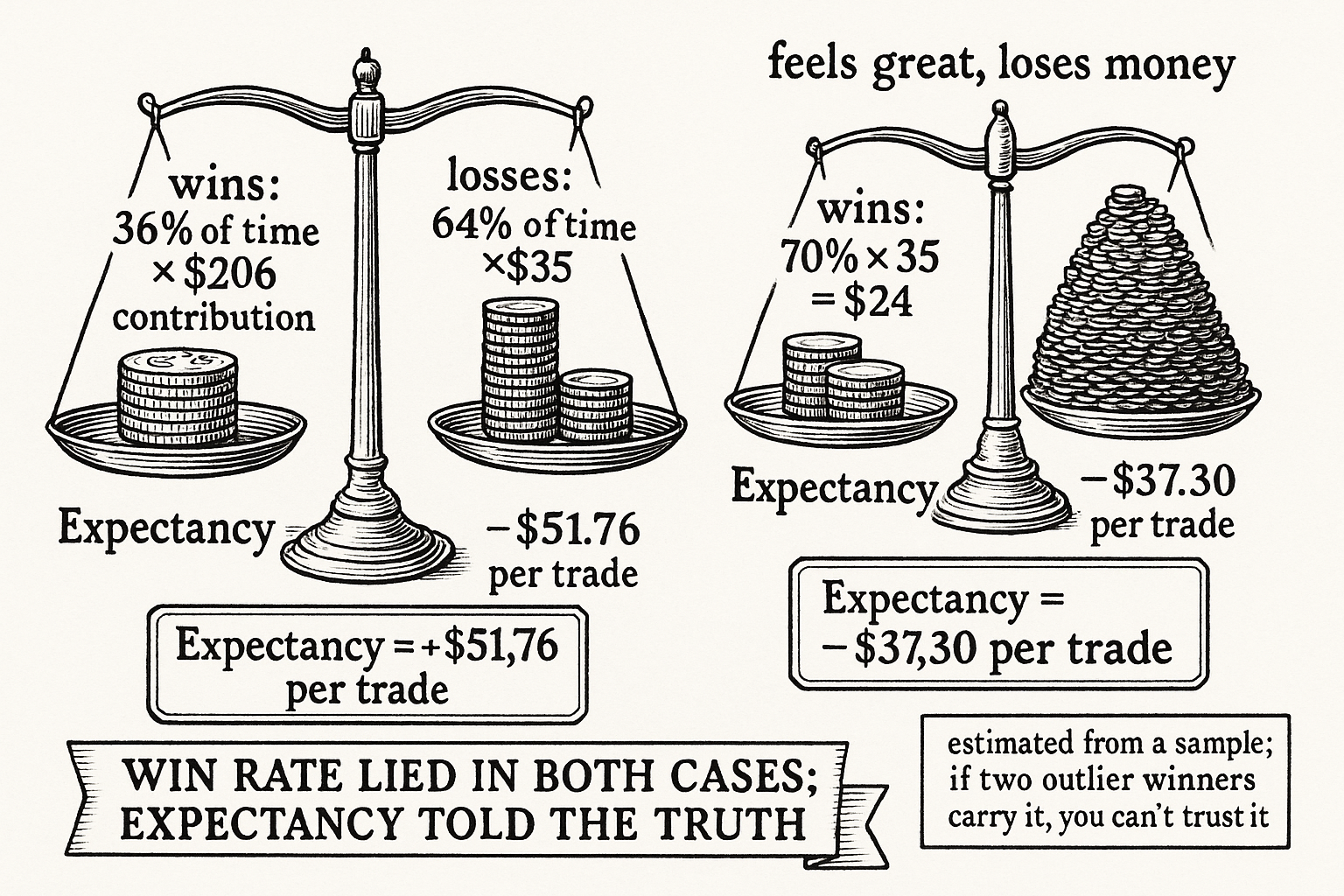

Numbers make the point the formula obscures. Take a trend-following system that wins 36% of the time. That sounds like a losing proposition until you put in the sizes. Suppose the average winner is $206 and the average loser is $35.

The expectancy is 0.36 times $206 minus 0.64 times $35, which is $74.16 minus $22.40, or $51.76 per trade. The system wins barely a third of the time and makes about $52 on every trade it takes, because the winners are roughly six times the size of the losers. Now flip it. Take a system that wins 70% of the time, a number that feels wonderful, with an average winner of $35 and an average loser of $206, the mirror image. Its expectancy is 0.70 times $35 minus 0.30 times $206, which is $24.50 minus $61.80, or negative $37.30 per trade. It wins twice as often and loses money on average, because the rare losses are large enough to swamp the frequent small wins. The win rate told you the opposite of the truth in both cases.

Why this is the number that decides everything

Expectancy is the foundation because it is what you multiply by frequency to get your edge over time. A system's profit per period is roughly its expectancy times the number of trades it takes, so a small positive expectancy traded often can beat a large one traded rarely, and a large negative expectancy traded often is the fastest way to ruin. This is also where position sizing enters: expectancy in R-multiples tells you the edge per unit of risk, and the sizing articles in this pillar turn that edge into how much capital to put behind each trade. Without a positive expectancy there is nothing to size, because betting more on a negative-expectancy system loses faster, not slower.

The caveat that protects you: expectancy is estimated from a sample, so the win probability, average win, and average loss are all noisy, and a backtest expectancy computed from a few dozen trades carries enormous uncertainty. A system whose entire positive expectancy rests on two outlier winners has an expectancy you cannot trust, because remove those two trades and the number flips. Compute expectancy on enough trades to mean something, look at how much of it depends on the tails, and treat a fragile expectancy the same way you treat any other overfit result.

Visualizing expectancy

KEY POINTS

- Expectancy is the average win or loss per trade, the one number that says whether a system makes money. It combines how often you win with how much you win and lose.

- The formula is the probability of a win times the average win, minus the probability of a loss times the average loss. Positive means the average trade adds to equity; negative means it subtracts.

- A 36% win-rate trend system with a $206 average win and $35 average loss has an expectancy of about +$52 per trade, because winners are six times the size of losers.

- The mirror image, a 70% win rate with a $35 average win and $206 average loss, has an expectancy of about -$37 per trade. It wins twice as often and loses money, because rare large losses swamp frequent small wins.

- Profit per period is roughly expectancy times trade frequency, so a small positive expectancy traded often can beat a large one traded rarely, and a negative expectancy traded often is the fastest route to ruin.

- Expectancy is estimated from a noisy sample. If two outlier winners carry the whole number, you cannot trust it, so compute it on enough trades and check how much rests on the tails.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Momentum, Market-Regime and Stocks & Options Trading Strategies

- Psychology-based Models of Asset Prices and Trading Volume

- The Impact of Volatility Targeting

- Investor sentiment in the theoretical field of behavioural finance

- Beating the Wick: A Regime-Filtered Intraday Gold Trading Strategy

- A Risk-Sensitive Trading Framework for Real Financial Markets - arXiv

- NBER WORKING PAPER SERIES VOLATILITY MANAGED

- Behavioral Finance: Theories and Evidence

- Evaluating Trading Strategies

- Trade Sizing Techniques for Drawdown and Tail Risk Control

- On the Performance of Volatility-Managed Portfolios

- Portfolio Management with Targeted Constant Market Volatility

- Cross-Asset Style Premia Asset Allocation Process

- Return Predictability and Market-Timing: A One-Month Model

- Behavioral Finance

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.