4.4 High Noise Markets Are Mean-Reversion Markets

High noise is mean-reversion fuel: motion that cancels out keeps returning to center. The danger is a flip to trend, so gate fades on the efficiency ratio and stop at the MAE edge.

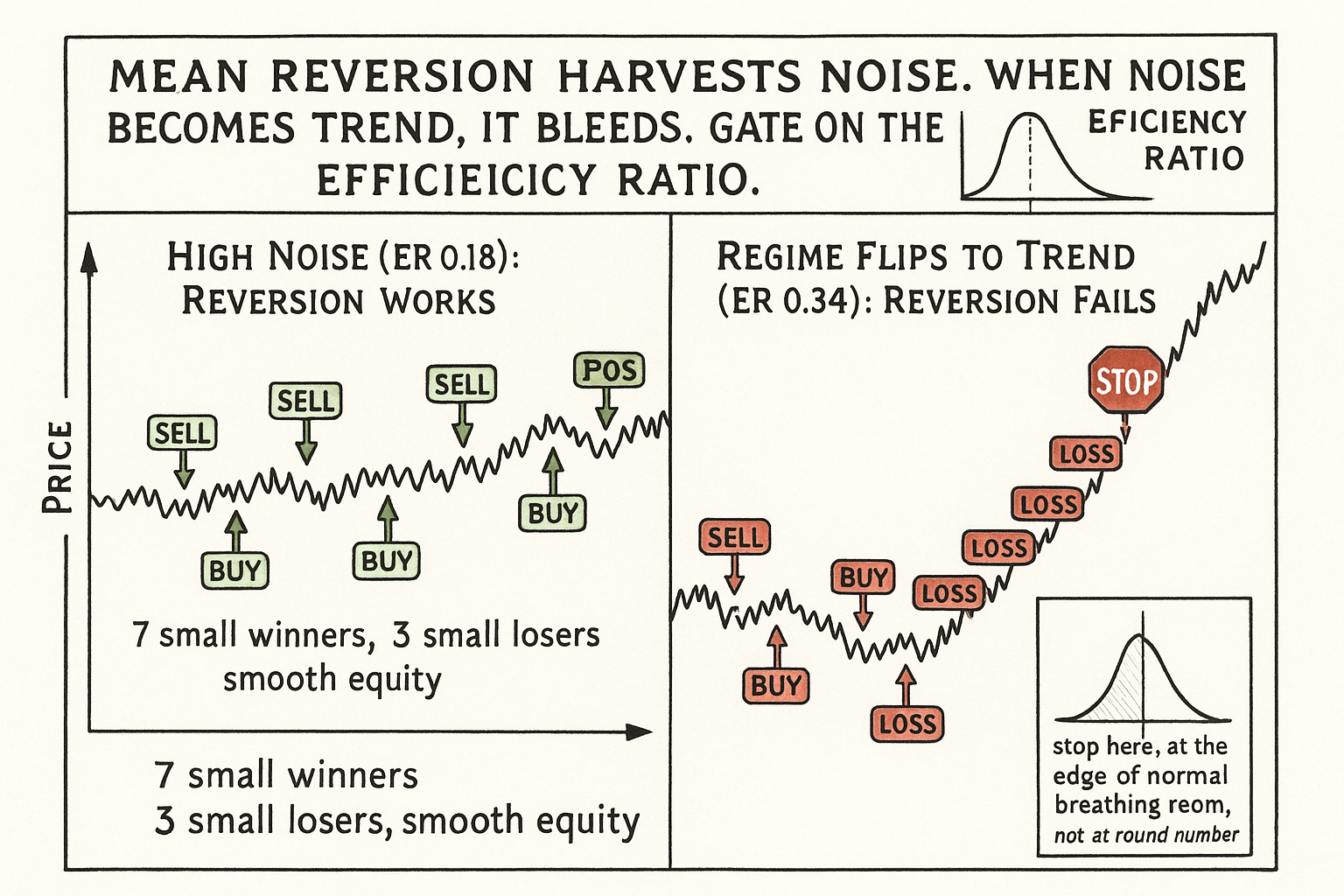

Run a simple fade system on EURUSD: when the 2-day return pushes more than one standard deviation above its recent mean, sell; when it pushes more than one standard deviation below, buy; exit at the mean. On EURUSD intraday and short-horizon daily data, where the efficiency ratio sits around 0.18, this system produces a high hit rate, many small winners, and a smooth equity curve, because the price keeps returning to its slowly moving center. Run the identical system on a trending crude-oil run where the efficiency ratio is 0.34, and it bleeds: every fade sells into a one-way move that does not come back, and the few winners cannot pay for the line of losers. Same logic, opposite result, and the only thing that changed was the noise level of the market.

This is the constructive half of the noise framework. The article "Noise Is Not Volatility" established that high noise means motion that cancels out; this article explains why that cancellation is precisely the raw material a mean-reversion system converts into profit, and why deploying reversion logic anywhere else is a structural mistake rather than a parameter problem. The instruments at the bottom of the trend-quality ranking from "How to Rank Markets by Trend Quality" are not bad markets. They are mean-reversion markets, and they are good at it for reasons rooted in who trades them and how.

Why high noise mechanically favors reversion

A mean-reversion system makes one bet: a move away from a center is more likely to reverse than to continue. That bet pays exactly when the market's motion cancels out, which is the definition of high noise. The link is not a coincidence; it is the same property measured two ways. A low efficiency ratio says net change is small relative to total path. Small net change relative to path means the price keeps coming back. Keeps coming back means reversion. The efficiency ratio and the reversion edge are reading the same underlying structure.

The microstructure mechanism is concrete. In a market dominated by two-sided market-making, every aggressive order is absorbed by a liquidity provider who then wants to offload the inventory, pushing price back toward where it was. The article "Noise Is Not Volatility" named this: dealer inventory management generates mean-reverting micro-structure, which shows up as high noise at short horizons. G10 FX is the cleanest example because interbank liquidity is deep and two-sided and there is no structural drift; the price oscillates around a fair value that moves slowly, and a fade system harvests the oscillation.

The autocorrelation signature confirms it. Mean-reverting markets show negative first-lag return autocorrelation at the reversion horizon: an up move is more likely to be followed by a down move. Trending markets show positive autocorrelation: an up move is more likely to be followed by another up move. The article "Market Personality" listed autocorrelation as a personality dimension; for a reversion system you want it negative at your horizon, and high noise and negative autocorrelation tend to travel together.

What the reversion edge actually looks like

The payoff profile of a reversion system in a high-noise market is the mirror image of a trend system's. Many small winners, occasional larger losers, high win rate, profit factor that depends on keeping the losers from running. The article "Why Profit Factor Can Lie" warned that a high win rate can mask a fat left tail; in mean reversion that tail is the move that does not revert, and it is the entire risk of the strategy.

Here is the asymmetry written out. Suppose the fade wins 70% of the time for an average of 0.4 volatility units and loses 30% of the time for an average of 0.9 volatility units when the reversion fails.

$$ E = p_{\text{win}} \cdot g - (1 - p_{\text{win}}) \cdot l = 0.70 \times 0.4 - 0.30 \times 0.9 = 0.28 - 0.27 = 0.01 $$

The expectancy E is win probability times average gain minus loss probability times average loss. With these numbers it is 0.28 minus 0.27, equal to 0.01 volatility units per trade, barely positive. The high win rate hides how thin the edge is, because the losers are more than twice the size of the winners. Push the loss size from 0.9 to 1.1 (one bad regime where reversions fail more often and run further) and the expectancy goes negative. This is why mean-reversion in high-noise markets lives or dies on the loss tail, not the win rate, and why the article "MAE/MFE Analysis: Seeing What Net Profit Hides" matters more here than almost anywhere: you have to see the maximum adverse excursion distribution to know whether your stop sits inside or outside the reversion's normal breathing room.

The failure mode: noise that turns into trend

A high-noise market is not permanently high-noise. The efficiency ratio drifts, and the worst thing that can happen to a fade system is a market that was choppy becoming trendy. Every reversion strategy has a hidden short position against trend: it is implicitly betting the move reverses, so a sustained move is its maximum-loss scenario. The article "When a Stop Loss Improves Risk but Destroys Edge" framed the trade-off; in mean reversion the stop is not optional, because without it a single regime transition from chop to trend can erase months of small winners.

The defense is a regime gate built on the efficiency ratio. Compute the rolling efficiency ratio at the reversion horizon and disable new fades when it rises above the chop threshold (say, above 0.25 to 0.30, climbing toward trend territory). This is the same gating logic the article "Efficiency Ratio Explained for Traders" described, applied defensively: the fade system runs while the market is noisy and steps aside when the market starts converting motion into direction. A reversion system without this gate is a reversion system that will eventually meet a trend and give back everything.

A second defense is the loss-tail stop sized off the maximum adverse excursion, not off a round number. If the reversion normally breathes 0.6 volatility units against you before reverting, a stop at 0.5 cuts winners; a stop at 2.0 lets the failed-reversion tail run. The MAE distribution tells you where the reversion's normal range ends and the regime-change tail begins, and the stop belongs at that boundary.

Which markets, and at which horizons

High noise is horizon-dependent, so a market can be a reversion market at one horizon and a trend market at another. EURUSD is strongly mean-reverting intraday and at the daily scale (efficiency ratio around 0.18), but at the multi-month horizon a carry or macro lean produces some persistence. Equity indices are the reverse: trend-friendly at multi-week horizons but mean-reverting at the 1-to-5-day scale, which is why short-horizon equity reversion (buy the dip in an uptrend) is a real strategy even though the index is a trend market at longer horizons. The article "Market Personality" listed short-horizon mean reversion as a fit for both FX and equity indices for exactly this reason.

The instruments that are mean-reversion markets across most horizons are the structurally two-sided, no-drift ones: G10 FX crosses, and to a degree the front end of deeply liquid government-bond futures. The instruments that are reversion markets only at short horizons are the trending ones (equity indices, trending commodities) where the long-horizon drift dominates but the short-horizon flow still mean-reverts. The discipline: measure the efficiency ratio at the horizon you intend to fade, not at some other horizon, the same horizon-matching point the article "How to Choose the Right Timeframe for a Strategy" develops.

Decision summary

| Efficiency ratio at fade horizon | Market type | Action |

|---|---|---|

| Below 0.20 | Strong reversion (G10 FX, choppy commodities) | Deploy fade or grid, gate on rising ER, stop at MAE boundary |

| 0.20 to 0.25 | Weak reversion / mixed | Fade with tighter gate, smaller size |

| Above 0.30 | Trend regime | Disable fades, the move will not revert |

The reversion system belongs in the bottom rows of noise and the top rows nowhere. The gate and the MAE-sized stop are not refinements; they are what keep a chop-to-trend transition from ending the strategy.

Visualizing the reversion edge and its failure

KEY POINTS

- High noise means motion that cancels out, which is exactly the raw material a mean-reversion system converts to profit. A low efficiency ratio and a reversion edge are the same structural property measured two ways.

- The microstructure mechanism: two-sided market-making absorbs aggressive orders and offloads inventory, pushing price back toward fair value. This generates mean-reverting micro-structure and high short-horizon noise. G10 FX is the cleanest example.

- The autocorrelation signature: reversion markets show negative first-lag return autocorrelation at the reversion horizon. High noise and negative autocorrelation travel together.

- The payoff profile is many small winners, occasional larger losers, high win rate. The edge can be thin: a 70% win rate at 0.4 units against 0.9-unit losers nets only 0.01 units expectancy, and a slightly worse loss size turns it negative.

- Mean reversion lives or dies on the loss tail, not the win rate. The maximum adverse excursion distribution tells you whether your stop sits inside or outside the reversion's normal breathing room.

- The defining failure mode is a high-noise market turning trendy. Every reversion system is implicitly short trend; a sustained move is its maximum-loss scenario.

- Two defenses: a regime gate that disables new fades when the rolling efficiency ratio climbs toward trend territory, and a stop sized off the MAE boundary rather than a round number.

- High noise is horizon-dependent. EURUSD reverts intraday and daily but leans at multi-month horizons; equity indices trend at multi-week horizons but revert at the 1-to-5-day scale. Measure the efficiency ratio at the horizon you intend to fade.

- The next article, "Low Noise Markets Are Trend-Following Markets", develops the mirror image: why the top of the trend-quality ranking is where trend systems earn their structural edge.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Liquidity in the Foreign Exchange Market: Measurement, Commonality, and Risk Premiums

- Interpreting Deviations from Covered Interest Parity During the Financial Crisis of 2007–08

- An ADX-Conditioned VWAP Strategy in FX Markets

- Short-term Trading Strategy on G10 Currencies

- Order Flows and Stock Returns: Compensation for Market Makers or Compensation for Liquidity Providers?

- How Do UK-Based Foreign Exchange Dealers Think Their Market Operates?

- The Microstructure of Financial Markets

- Charts, Noise and Fundamentals in the London Foreign Exchange Market

- A Regime-Conditioned Statistical Mean Reversion Framework for Intraday Foreign Exchange (FX) Markets

- Simple Measures of Market Efficiency: A Study in Foreign Exchange Markets

- Dealer Behavior and Trading Systems in Foreign Exchange Markets

- Do Inventories Matter in Dealership Markets? Evidence from the U.S. Government Bond Market

- Life in the Pits: Competitive Market Making and Inventory Control

- The Cross-Sectional Determinants of Inventory Control and the Subtle Role of Inventory Risk

- Trends and Reversion in Financial Markets on Time Scales from Minutes to Decades

- Testing the White Noise Hypothesis of Stock Returns

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.