1.24 Alpha Decay Is Just Competition (and Papers Lie)

Alpha decay isn't physics, it's a crowd. There are more funds than strategies, your edge gets divided until it dies, and published papers are crowded corpses. Verify everything yourself.

Your strategy stops working and you reach for a physics metaphor. The edge "decayed," like a radioactive isotope obeying some law of nature. The metaphor is comforting and wrong. Nothing about your edge half-lifed on its own. Other people found the same trade and competed the return out of it. Alpha decay is not entropy. It is a crowd.

Once you see decay as competition rather than decay as physics, the defenses change. You stop treating a dying curve as bad luck and start treating it as a signal that the inefficiency you found is no longer yours alone. The old article "Why Systems Work Until They Don't" mapped the lifecycle (discovery, deployment, decay, death) and named crowding as a decay mechanism. This is the mechanism running the whole show.

There are more funds than strategies

Start with the supply-demand picture. Equities is a developed, picked-over market, and there are still opportunities in it. There are also far more hedge funds than there are distinct strategies. Do the arithmetic on that and the conclusion is forced: the same handful of ideas is being run by many teams at once.

Novel ideas are mostly a myth. Whatever you discover, someone else has it or will have it soon. The only real questions are how many people share your idea and how good their version is. You are not racing to find something nobody has seen. You are estimating how crowded a known room already is.

$$ \alpha_{\text{realized}} \approx \frac{\alpha_{\text{raw}}}{1 + N_{\text{competitors}}} $$

This is a heuristic, not a measured law, so treat it as intuition. The raw edge of an inefficiency gets split across everyone trading it. One participant keeps most of it. Ten participants chasing the same signal each get a sliver, and the act of all of them trading it pushes the price to where the signal no longer fires. The edge did not evaporate. It got divided until each slice fell below costs. That is what a decaying equity curve is telling you: the room filled up.

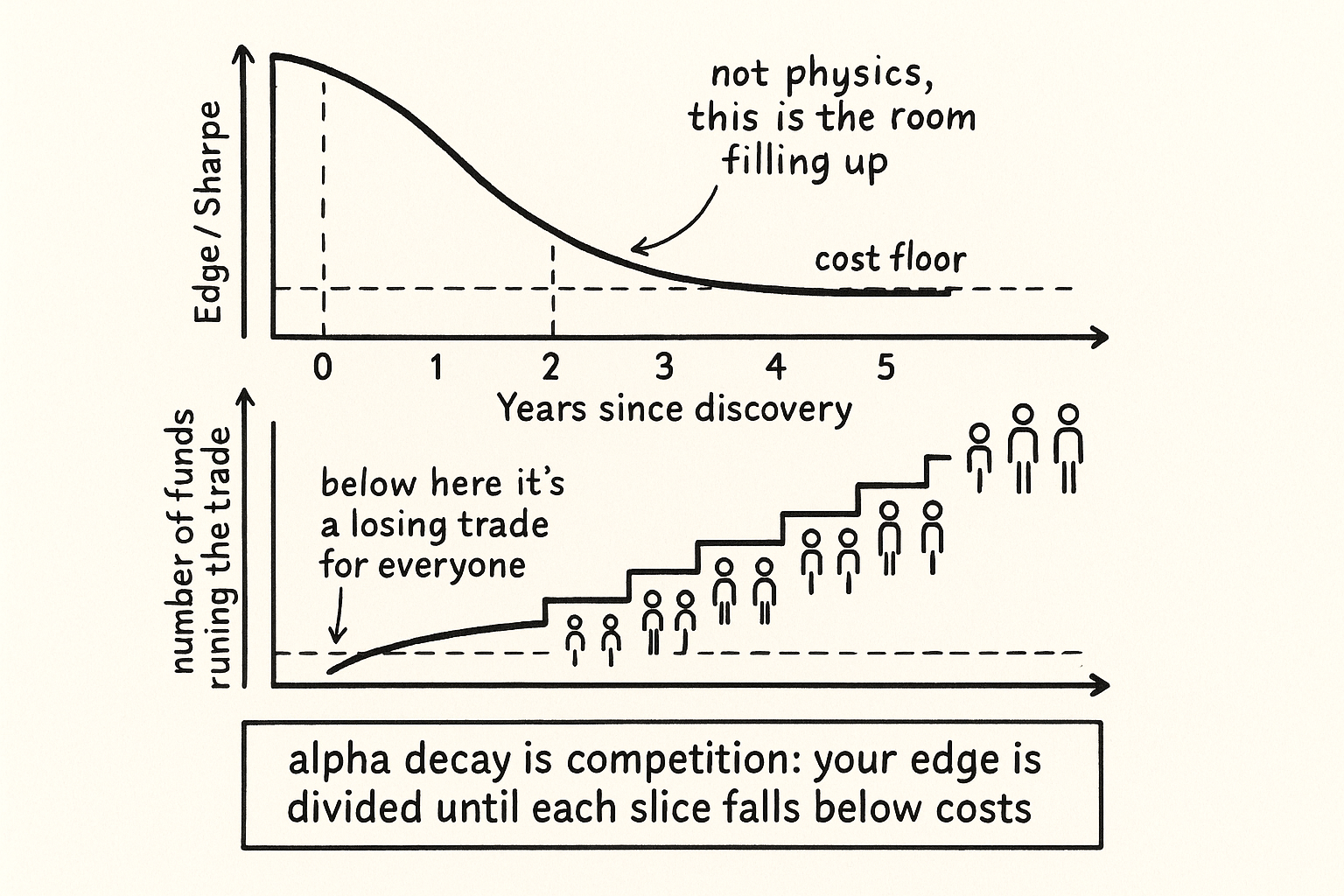

The exponential shape, and why it is competition

Crowded edges fade with a recognizable curve. Model the surviving edge as exponential decay with a half-life.

$$ \alpha(t) = \alpha_0 \cdot \left(\tfrac{1}{2}\right)^{t / h} $$

The half-life h is the time for the edge to fall by half. The old article "Why Systems Work Until They Don't" put rough class-specific values on it: statistical arbitrage at two to three years, factor strategies at five to ten, trend at ten to twenty, market-making at half a year to two. Plug in h of two years and read the schedule: full edge today, half in two years, a quarter in four, an eighth in six. A strategy you deploy at a 2.0 Sharpe is a 1.0 Sharpe strategy in two years if it is the crowded kind, and you should size and plan as if that schedule is real.

The half-life is short precisely when the edge is easy to find and copy. Stat-arb decays fast because it is a known game with low barriers. Trend decays slowly because it is uncomfortable to hold and capacity-hungry, so fewer participants pile in. The decay rate is a competition rate. The barriers from the theory-of-edge framework (operational pain, capacity limits, the discomfort of fat-tailed payoffs) are the things that slow the crowd down and stretch the half-life.

The data edge, and what it costs

One way to stay ahead of the crowd is to see what they cannot. That is the data edge, and it is expensive and real. A firm like QRT spends on the order of $100 million a year on data. The most expensive feeds are not satellite images or credit-card panels. They are traders bought off bank execution desks, human knowledge of flow that does not exist in any dataset you can buy.

For an individual, the data edge is mostly out of reach, and the lesson is to know that, not to pretend otherwise. The number matters because it sets a breakeven you will never meet at that scale.

$$ \text{data edge pays} \iff \big(\alpha_{\text{with data}} - \alpha_{\text{without}}\big) \cdot \text{AUM} \; > \; \text{data cost} $$

To justify $100M of annual data spend you need the incremental alpha from that data, times the capital you run it on, to clear $100M. That math only closes for very large books, which is why the data edge concentrates at the top. Trying to win on data against firms spending nine figures is the same mistake as trying to out-compute them: you picked the one game where your disadvantage is largest. The way around it is not better data. It is a constraint they decline to take.

Papers lie

The cheapest place to source ideas is published research, and it is also the place most likely to hand you a corpse. You cannot read a paper, implement the strategy, and expect alpha to fall out. Papers lie to you, and the lying is structural, not malicious.

The mechanism is survivorship and incentive. A published backtest is the one configuration out of many that cleared the journal's bar, which is the undocumented parameter sweep the old article "Why Quantitative Does Not Automatically Mean Scientific" warned about. By the time an edge is in print, it has been read by thousands of the exact people who would trade it, which crowds it before you finish reading the abstract. And the author has no incentive to publish the version that still works and every incentive to publish the version that gets cited.

The defense is to verify everything yourself and trust nothing on the page. Treat a paper as a hypothesis to be tested on your own data with your own costs, not as a result to be deployed. Expect that the effect is weaker than reported, already crowded, or gone. The same applies to blogs and books and any public idea: exposure to many sources is how you generate candidates, and independent verification is the only thing that separates a live edge from a retold story. People steal alpha constantly in this industry, and the published edge is the most stolen of all.

Reading the death versus the dip

Competition-driven decay needs a different response than a normal drawdown, and confusing them is expensive in both directions. The old article "When to Switch Off a Trading System" drew the line between a statistical breach (recent behavior stops matching history) and a structural breach (the inefficiency provably changed). Crowding is a structural breach. It deserves more weight than a price-based drawdown alone, because it kills the edge before the equity curve has finished confirming the damage.

Practical read. If your edge is the crowded kind and the return is grinding lower while the trade gets more popular, more discussed, more obviously known, that is competition eating the alpha and it is not coming back by waiting. If the edge sits behind a real barrier and the drawdown looks like one of its historical drawdowns, you are inside the normal envelope and switching off is the expensive error. Size the kill decision to the cause. Decay-as-competition does not reverse; decay-as-noise does.

Visualizing the crowd

KEY POINTS

- Alpha decay is competition, not physics. The edge did not half-life on its own. Other people found the same trade and split the return until each slice fell below costs.

- There are more funds than distinct strategies. Novel ideas are mostly a myth; the real questions are how many share your idea and how good their version is.

- Crowded edges fade exponentially. With a two-year half-life, a 2.0 Sharpe is a 1.0 Sharpe in two years. The half-life is short when the edge is easy to copy and long when a real barrier slows the crowd.

- The data edge is real and concentrated. Spending on the order of $100M a year, mostly on humans from bank execution desks, only breaks even on a very large book, so it is out of reach for an individual.

- Papers lie by construction: published results are the surviving configuration of a parameter sweep, they are crowded the moment they print, and authors are not incentivized to publish what still works. Verify on your own data and costs.

- Treat crowding as a structural breach, which kills the edge before the curve confirms it. A crowded edge grinding lower while the trade gets more popular is not coming back by waiting; a barriered edge in a normal-looking drawdown is.

References

- Does Academic Research Destroy Stock Return Predictability? (McLean and Pontiff)

- Replicating Anomalies (Hou, Xue, Zhang)

- ...and the Cross-Section of Expected Returns (Harvey, Liu, Zhu, multiple testing)

- Crowded Trades and Tail Risk in Hedge Fund Strategies

- Alpha Decay and Strategy Capacity in Quantitative Investing