1.23 The Theory of Edge: Why the Market Pays You

Edge is not knowing what others don't, it's doing what others won't. You get paid for constraints: operational pain, capacity-vs-skill, risk premia, thin margins. Name your check or assume you have none.

Most traders look for edge in the wrong place. They hunt for an insight, a pattern, a signal nobody else has found. If that is the game, the opponents are firms with more data, more compute, and more capital than you will ever assemble. You lose that game before you sit down. The reachable edge has nothing to do with knowing something others do not. You get paid for doing something others will not.

The question to carry around is not "what do I know that others don't." It is "what can I do that others won't." That reframing is the whole article. The rest is the taxonomy of the constraints that pay, and how to tell which one is actually cutting you a check.

Getting paid is a transaction, not a reward

Decompose any gross return into the pieces that produced it.

$$ R = R_f + \beta \cdot R_{\text{market}} + \sum_k \lambda_k \, x_k + \alpha $$

Read it left to right. R_f is the risk-free rate you earn for doing nothing. The beta term is the market drift you capture for holding the index, which the old article "Why Quantitative Does Not Automatically Mean Scientific" called out as the free long-bias return that masquerades as skill. The sum is a set of risk premia: each x_k is an exposure (carry, illiquidity, volatility selling, credit) and each lambda_k is the price the market pays you to hold that exposure through the discomfort. Alpha is the leftover, the part you take from another participant who priced something wrong.

Retail content sells the last term and ignores the middle one. The middle one is where most reachable money sits. Risk premia are not edge in the clever sense. They are payment for sitting in a position other people want to get out of. You provide liquidity to the person who wants out, you absorb the volatility they cannot stomach, and you collect the premium for being the buyer at the moment everyone else is a seller. You are not outsmarting that seller. You are out-tolerating them.

The four constraints that pay

The constraints worth building a business on fall into four buckets. Each one is a reason a better-resourced participant declines the trade and leaves it for you.

Operational pain. Some edges require work that is annoying enough that capable firms pass. Reconciling messy data feeds, handling physical delivery, managing a dozen exchange integrations with bad APIs, dealing with tax or settlement plumbing. None of it is intellectually hard. All of it is a grind, and the grind is the moat. The firm that could out-model you decides the operational drag is not worth the capacity, so the trade stays open.

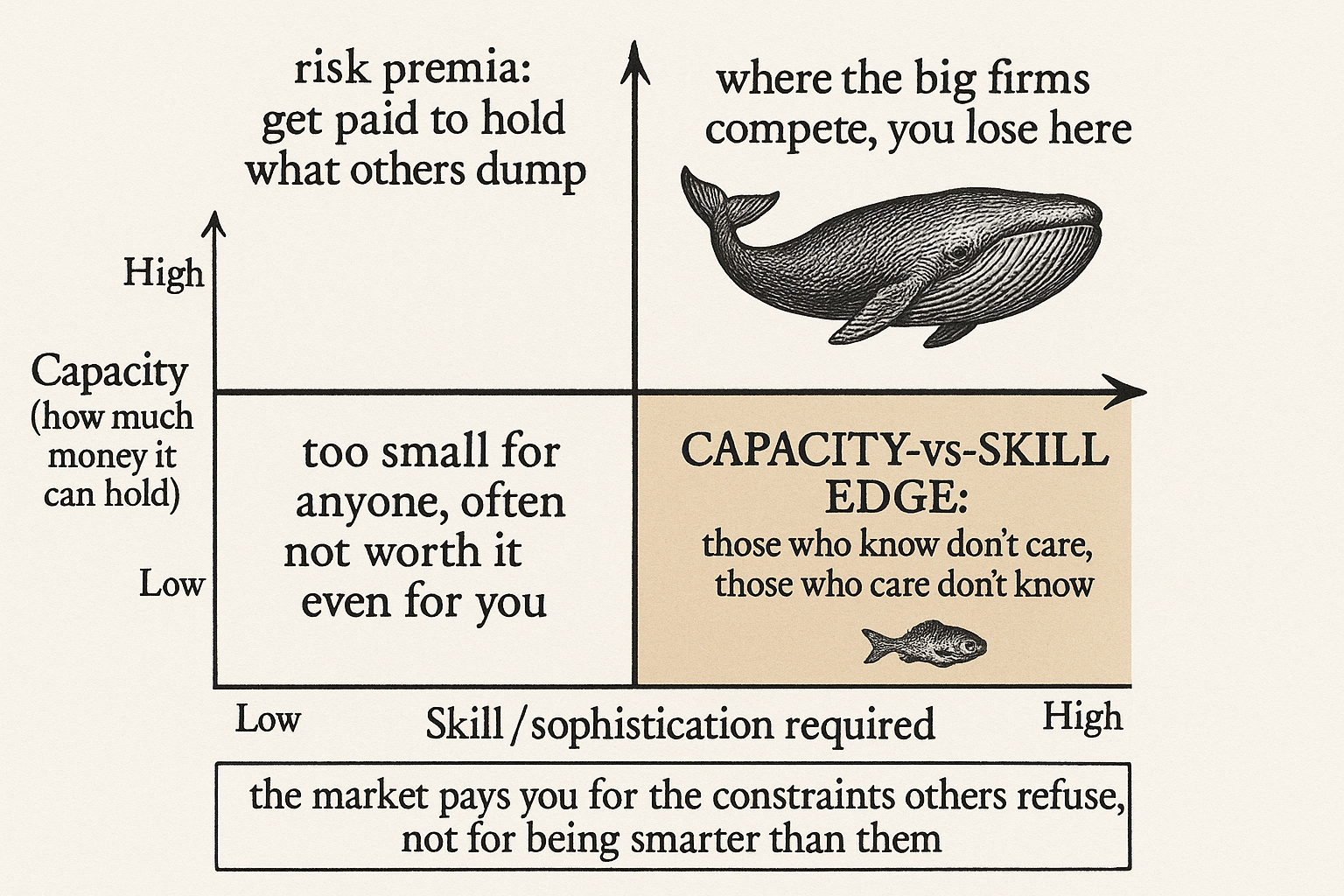

Capacity versus skill. The most valuable of the four. A niche trade has a hard capacity ceiling, and that ceiling makes it invisible to size. The people who know how to run it do not care, because it cannot move the needle on a large book, and the people who would care cannot find or build it. Those who know don't care; those who care don't know. That gap is where a small trader lives.

Risk premia. Covered above. You take a risk off someone's hands and get paid for the transfer. Carry, insurance-like volatility selling, illiquidity. The payment is real and recurring, and the price of it is that the risk occasionally arrives and hurts.

Small margins. Edges too thin for a big cost base to bother with. A trade that nets a few basis points per turn is worthless to a fund carrying large fixed costs and answering to investors who want a headline Sharpe. Run lean, and a few basis points compounded across many turns is a business.

The capacity math, worked

The capacity-versus-skill edge is worth a number, because the number is why it survives.

Take a niche trade with $5 million of capacity that returns 40% a year at the size it can hold. That is $2 million of profit. Real money to an individual. Now hand it to a $20 billion fund.

$$ \text{contribution} = \frac{\text{capacity} \times \text{return}}{\text{AUM}} = \frac{5\text{M} \times 0.40}{20{,}000\text{M}} = 0.01\% $$

The trade adds one basis point to the fund's annual return at full capacity, before the cost of the team, the infrastructure, and the risk committee's attention. The fund passes. Not because they cannot run it, but because it is not worth the seat it would take up. The same trade that is beneath their notice is a third of your year. The ceiling that makes it useless to them is exactly what keeps it uncrowded for you.

This is the structural reason a small operator can survive in a market dominated by larger, smarter teams. You are not competing with them on the trades they want. You are taking the trades they decline.

Know which check you are cashing

Edge that you cannot name is edge you cannot defend. Two questions force the issue.

First, why do you make money? The honest answers are short: you harvest a risk premium, you have a model edge, you have a data or information edge, you have superior access to cost or rebates, or you do not have an edge at all. Most traders cannot pick one. If you cannot, assume the last option until proven otherwise.

Second, why do you keep the money? An edge with no barrier gets competed to zero. The barriers are specific: a fat-tailed payoff that scares competitors out (the kind that kills people who size it wrong), an infrastructure barrier, a knowledge barrier, a psychological barrier, an opportunistic special-situation nature with nothing to fit, or a structural barrier from unfair access. Every one of these is measured against one benchmark: the dollar-volume-weighted participant on the other side of your trades. You do not need to beat everyone. You need to be doing something the average dollar across from you will not do.

$$ \text{edge exists} \iff \big(\text{your willingness} \;-\; \text{marginal participant's willingness}\big) > \text{cost} $$

The marginal participant is the dollar-weighted average of who you trade against. If your only advantage is that you are willing to hold the position they are dumping, that is a real edge as long as the premium clears your costs. If you have no such gap, you are the marginal participant, and the expected value of the game is your cost base running in reverse.

Mixing and stacking

The constraints are not mutually exclusive, and the good operators run several at once and rotate them with conditions. When alts are running, add depth to alts and collect the premium for providing it. When funding is rich on perps, run the funding trade. When one market goes wide and illiquid, the operational-pain and small-margin edges fatten. The mix is the point. Each individual constraint is a thin, decaying source, which is the same lesson the old article "The Death of the Single-System Trader" made about rules: one source of edge is one regime change from zero, and the defense is several uncorrelated ones running in parallel.

There is also a compounding structure. New alpha sources are additive. Better execution is a multiplier on the edge you already have. A firm like Citadel does not win by inventing every edge it runs. It wins from scale, from being the largest participant with the best cost structure, and it multiplies whatever raw edges it touches through superior execution. You will not have that multiplier. You compete on the additive side, by finding constraints the multiplier-firms decline to bother with.

Visualizing the trade-off

KEY POINTS

- The reachable edge is not knowing what others don't. It is doing what others won't: absorbing volatility, providing liquidity to the person who wants out, out-tolerating rather than outsmarting.

- Gross return splits into the risk-free rate, market beta drift, a sum of risk premia, and alpha. Retail content sells the alpha term and ignores the risk premia, which is where most reachable money sits.

- Four constraints pay: operational pain, capacity-versus-skill, risk premia, and small margins. Each is a reason a better-resourced firm declines the trade.

- Capacity-versus-skill is the strongest. A $5M-capacity trade returning 40% adds one basis point to a $20B fund, so they pass, and a third of your year stays uncrowded.

- Name your edge with two questions: why you make money (risk premium, model, data, cost access, or nothing) and why you keep it (a specific barrier measured against the dollar-volume-weighted participant).

- One constraint is one source of edge, and it decays. Run several and rotate them with market conditions, the same diversification logic that keeps a multi-system trader alive.

References

- Risk Premia Harvesting Through Dynamic Allocation (alternative risk premia)

- Liquidity Provision and the Cross-Section of Hedge Fund Returns

- Capacity Constraints and the Decline of Hedge Fund Alpha

- Buffett's Alpha: Leverage, Low-Risk Exposures and Premia (Frazzini, Kabiller, Pedersen)

- Do Hedge Funds Exploit Rare Disaster Concerns? (tail risk premia)