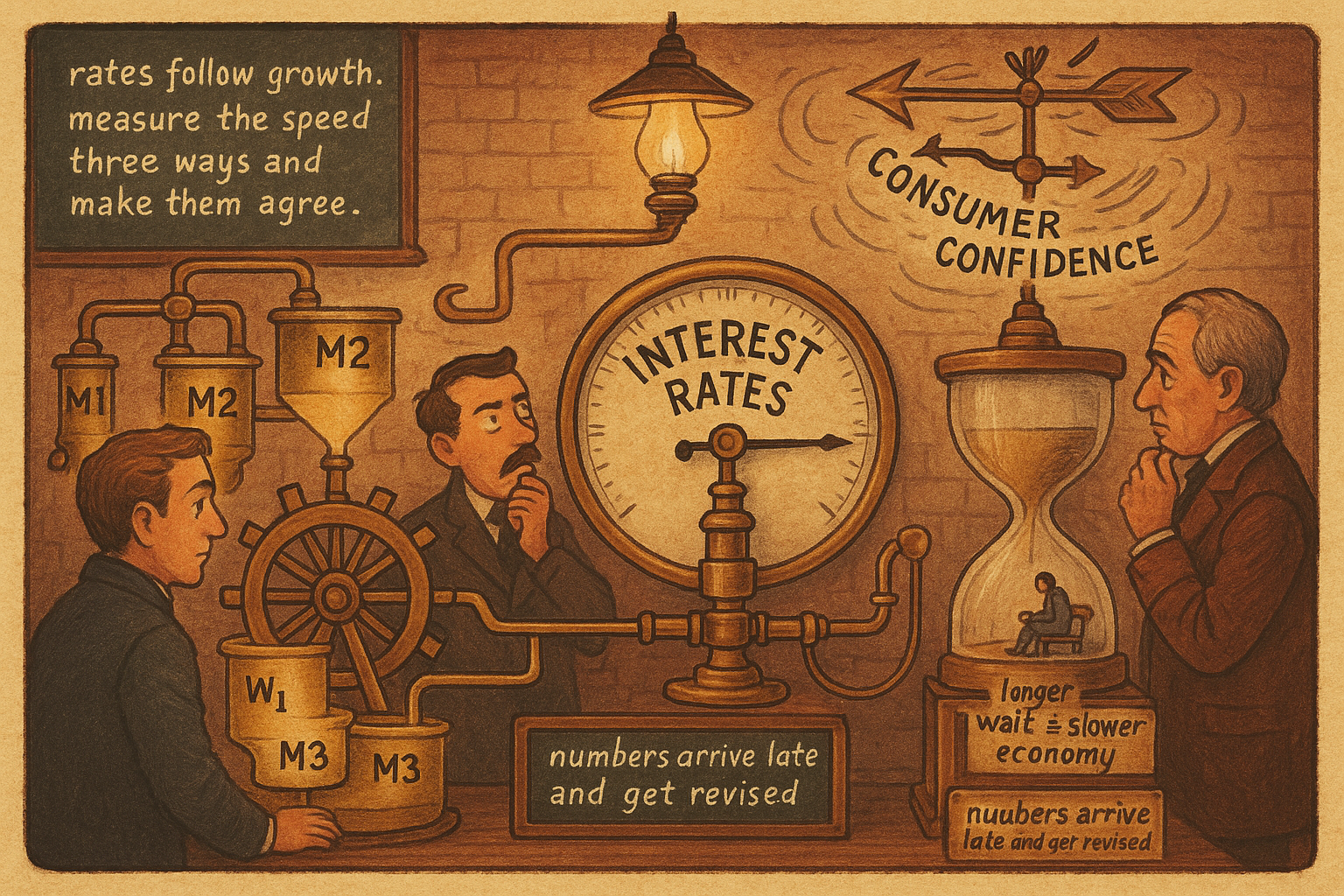

4.42 Money Supply, Confidence, and Unemployment Duration as Rate Predictors

When inflation is quiet, rates still follow growth. Money supply, consumer confidence, and unemployment duration read the economy's speed, strongest on the long end, and only when they agree.

Inflation is the loudest driver of interest rates, but it is not the only one, and in the stretches where inflation sits quiet, rates still move. Three slower fundamentals do the moving: how much money is sloshing through the system, how confident consumers feel, and how long the average jobless person stays jobless. Each one is a window into the speed of the economy, and the speed of the economy sets the demand for money, which sets rates. The "Predicting Interest Rates from Inflation: The Real-Rate Ratio" article handled the inflation spoke; this one adds the activity spokes that fire when inflation is not the story.

The common thread is that rates follow growth. A faster economy wants more credit, bids up the price of money, and pushes rates higher. A slowing economy does the reverse. So any indicator that leads the growth rate is, secondhand, an indicator that leads rates. That is the logic behind treating copper as an activity proxy in "Copper as an Economic Activity Indicator," and these three series are the same idea sourced from monetary and labor data instead of an industrial metal.

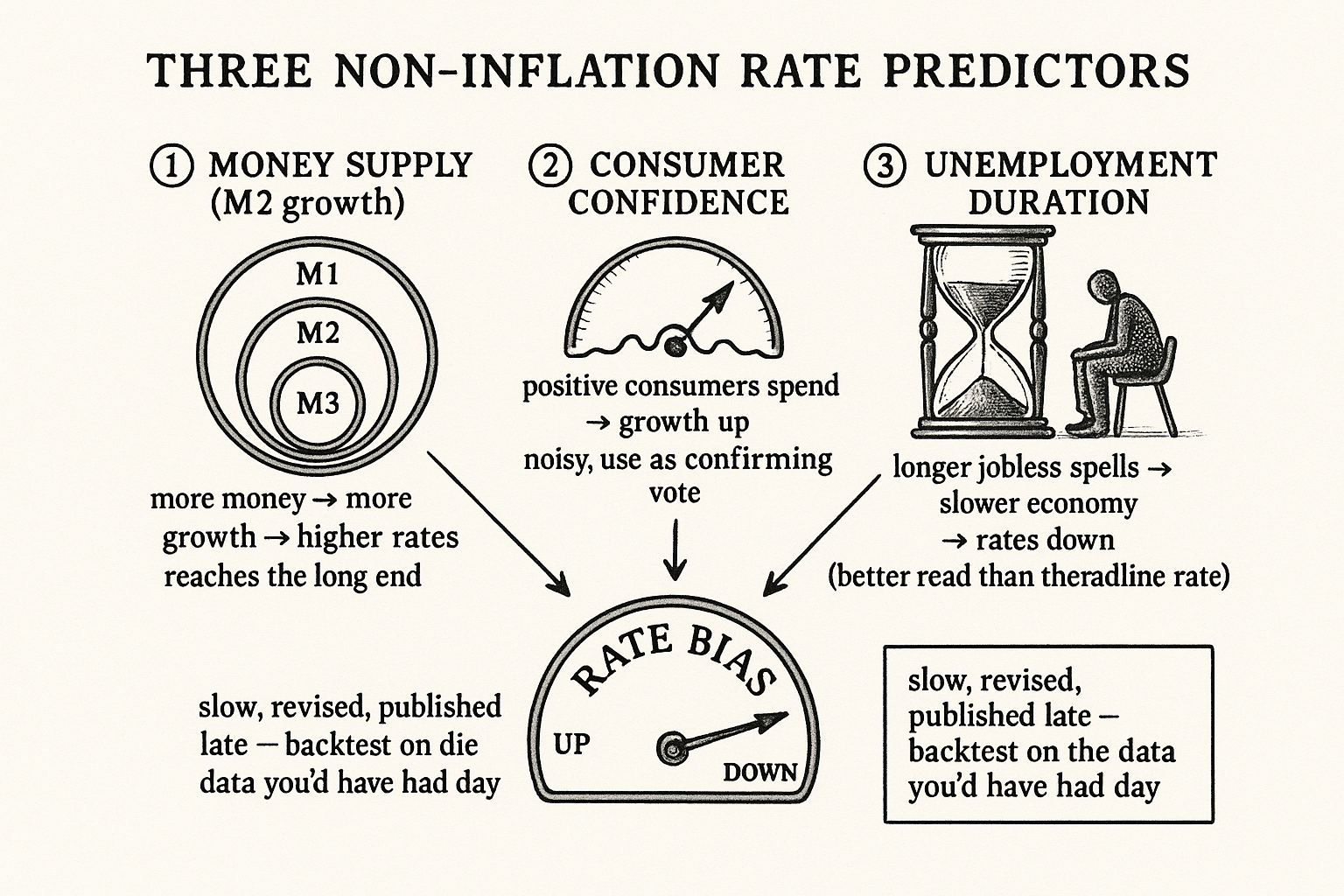

Money supply: M1, M2, M3

Money supply is measured in widening circles, and you should know which circle you are quoting. M1 is the narrow one: money held as cash or in checking accounts, the stuff you can spend right now. M2 adds the next ring out, time deposits and CDs, money that is one small step from spendable. M3 is the widest, M2 plus the assets and liabilities of financial institutions that can be converted into spendable form.

$$ \text{M1} \;=\; \text{cash} + \text{checking} $$ $$ \text{M2} \;=\; \text{M1} + \text{time deposits, CDs} $$ $$ \text{M3} \;=\; \text{M2} + \text{convertible institutional assets/liabilities} $$

Each layer adds money that is a little harder to spend on a moment's notice. The mechanism that connects this to rates is direct: the more money in the system, the more the economy grows, and that growth translates into higher rates. M2 is the workhorse for this. M2 and rates are correlated, and money supply is predictive for rates, with a stronger pull on long-term rates than on short. More money in the system today plants the growth that long rates are trying to price years out, which is why the money-supply signal reaches further down the curve than the inflation signal does.

Use the growth rate of M2, not its level. The absolute dollar amount of M2 climbs forever; what matters is whether it is accelerating or decelerating relative to its own history, the same stationarizing instinct from "How to Build Stationary Indicators from Non-Stationary Prices." A rising M2 growth rate is fuel for future activity and future rates.

Consumer confidence

Confidence is the psychology spoke. If consumers feel positive, they spend and borrow, growth increases, and rates follow growth up. If they turn cautious, they save, growth cools, and rates ease. The series is soft and sentiment-driven, so it is noisier than money supply, but it leads because spending decisions get made on feeling before they show up in hard activity data.

The honest caveat is that confidence is the weakest of the three. Sentiment surveys whip around, get revised, and sometimes diverge from what people actually do with their wallets. Treat confidence as a confirming vote, not a standalone trigger. When confidence agrees with money supply and labor data, you have a coherent growth story; when it fights them, trust the harder series and wait.

Unemployment duration

The labor spoke is the sharpest of the three, and it is not the unemployment rate. It is the average duration that someone stays unemployed. Duration measures the texture of the labor market in a way the headline rate misses. When people who lose jobs find new ones fast, the economy is humming, demand for money is firm, and rates hold up or rise. When the average jobless spell stretches out, the economy is slow, hiring is weak, and rates drift down.

The logic is clean: the longer someone is out of work, the slower the economy is running, and the lower rates will go. Duration is a better read than the raw unemployment rate because the rate can fall for ugly reasons, like discouraged workers leaving the labor force, while rising duration unambiguously says the people who are unemployed are stuck, which only happens when hiring has stalled. Duration lengthening is a slowdown signal, and a slowdown signal is a rates-down signal.

Putting the three together

These are slow, low-frequency series, and the right way to use them is as a composite read on the direction of the economy, which then conditions your rate view.

$$ \text{growth pressure} \;\sim\; \big(\text{M2 growth} \uparrow\big)\;+\;\big(\text{confidence} \uparrow\big)\;+\;\big(\text{unemployment duration} \downarrow\big) \;\Longrightarrow\; \text{rates bias up} $$

Read it as a vote, not an equation to evaluate to a decimal. Rising M2 growth, rising confidence, and shortening unemployment duration all point the same way: the economy is speeding up, and rates have an upward bias. Flip all three and rates have a downward bias. The value of stacking them is that they fail at different times. Money supply can mislead during a credit crunch when money exists but does not circulate; confidence can spike on a headline and fade; duration lags the turn. No single one is trustworthy alone, so you want agreement across the set before leaning on the macro view, and you treat disagreement as a signal to wait rather than to average.

Mind the publication lag and revisions. These series arrive late and get revised, sometimes heavily, so a real-time backtest has to use the vintage of the data you would have actually had on the day, not the polished number in today's database. Backtesting macro signals on revised data is a quiet form of look-ahead, and it flatters every fundamental system that has ever been built. This is the kind of subtle leakage "How to Test Indicator Thresholds Without Fooling Yourself" warned about, transplanted from price indicators to economic releases.

Where this lands: money supply, confidence, and unemployment duration give you the non-inflation read on rates, strongest on the slow end of the curve. They pair with the inflation signal from the Real-Rate Ratio, and they set up the next distinction in this arc, "Short Rates Price the Present, Long Rates Price the Future", which explains why money supply reaches the long end while inflation grips the short end.

Visualizing the three rate predictors

KEY POINTS

- When inflation is quiet, rates still move on the speed of the economy. Three slow fundamentals read that speed: money supply, consumer confidence, and unemployment duration. Rates follow growth.

- Money supply comes in widening circles: M1 (cash and checking), M2 (M1 plus time deposits and CDs), M3 (M2 plus convertible institutional assets). More money means more growth means higher rates.

- M2 is the workhorse: correlated with rates and predictive, with a stronger pull on long-term rates than short. Use M2 growth rate, not its ever-rising level.

- Consumer confidence is the psychology spoke and the weakest of the three. Positive consumers spend and borrow, lifting growth and rates. Noisy and revision-prone; use as a confirming vote, not a standalone trigger.

- Unemployment duration, not the headline rate, is the sharpest labor signal. Longer average jobless spells mean a slower economy and lower rates. Duration avoids the trap of a rate that falls because workers left the labor force.

- Use the three as a composite vote on economic direction. They fail at different times, so require agreement before leaning on the view and treat disagreement as a reason to wait.

- These series are published late and revised. Backtest on the data vintage you would have had that day, or you import look-ahead bias into every fundamental signal.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Interest Rates and Money in the Measurement of Monetary Policy

- Monetary Policy and Short-Term Interest Rates: An Efficient Markets–Rational Expectations Approach

- Money Supply

- Measuring Monetary Policy by Money Supply and Interest Rate

- Money demand accommodation: Impact on macro-dynamics and implications for monetary policy

- The Rise and Fall of M2

- Analysing the impact of money supply on economic growth: A panel regression approach for Western Balkan countries (2000–2023)

- Effects of fiscal deficit and money M2 supply on inflation