4.65 Monetary Policy and Central-Bank Bias as the #1 FX Driver

Monetary policy is the #1 FX driver, but it moves currencies through expectations, not the rate level. The market forward-discounts the path, so you trade the surprise: a cut smaller than priced rallies the currency.

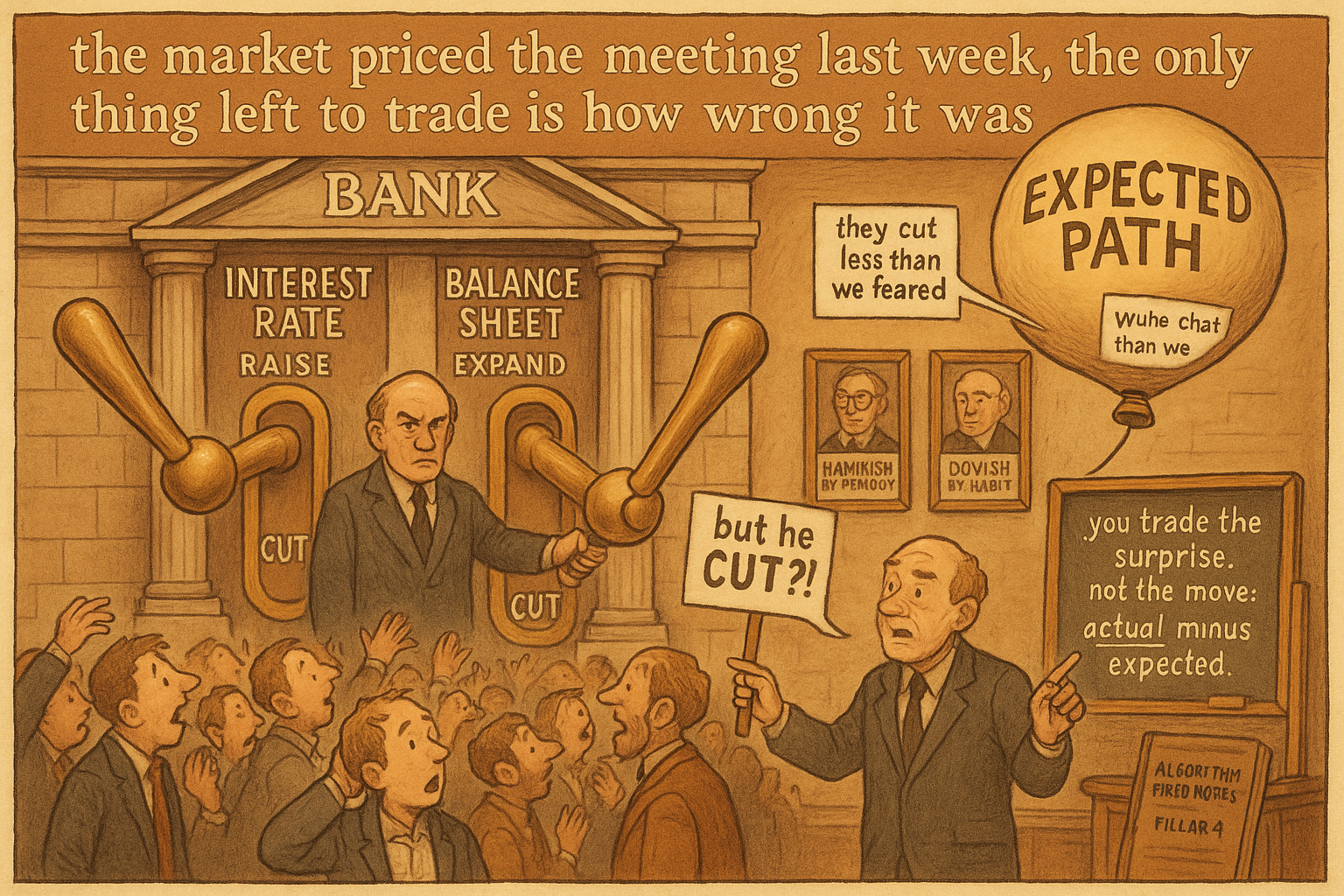

The central bank cuts rates and the currency rallies. New traders stare at the screen and conclude the market is broken. The market is not broken. The cut was 25 basis points and the market had already priced 50, so a "cut" that undershoots expectations is a hawkish surprise, and the currency rallies on the gap between what happened and what was already in the price. Monetary policy is the single most consistent driver of currencies most of the time, and it works through expectations, not through the level. Miss that and you trade every meeting backwards.

Monetary policy tops the domestic-driver list because the relative rate setting is what a floating currency is, at bottom: a claim on a yield differential that the market reprices the instant the expected path of that differential moves. The old article "Global vs Domestic Currency Drivers" put it at the head of the three domestic engines and noted it drives most of the time, when the world is calm enough for domestic factors to be in charge. This is the mechanism underneath that ranking.

Two levers, not one

A central bank has two tools, and the second one used to be invisible to traders.

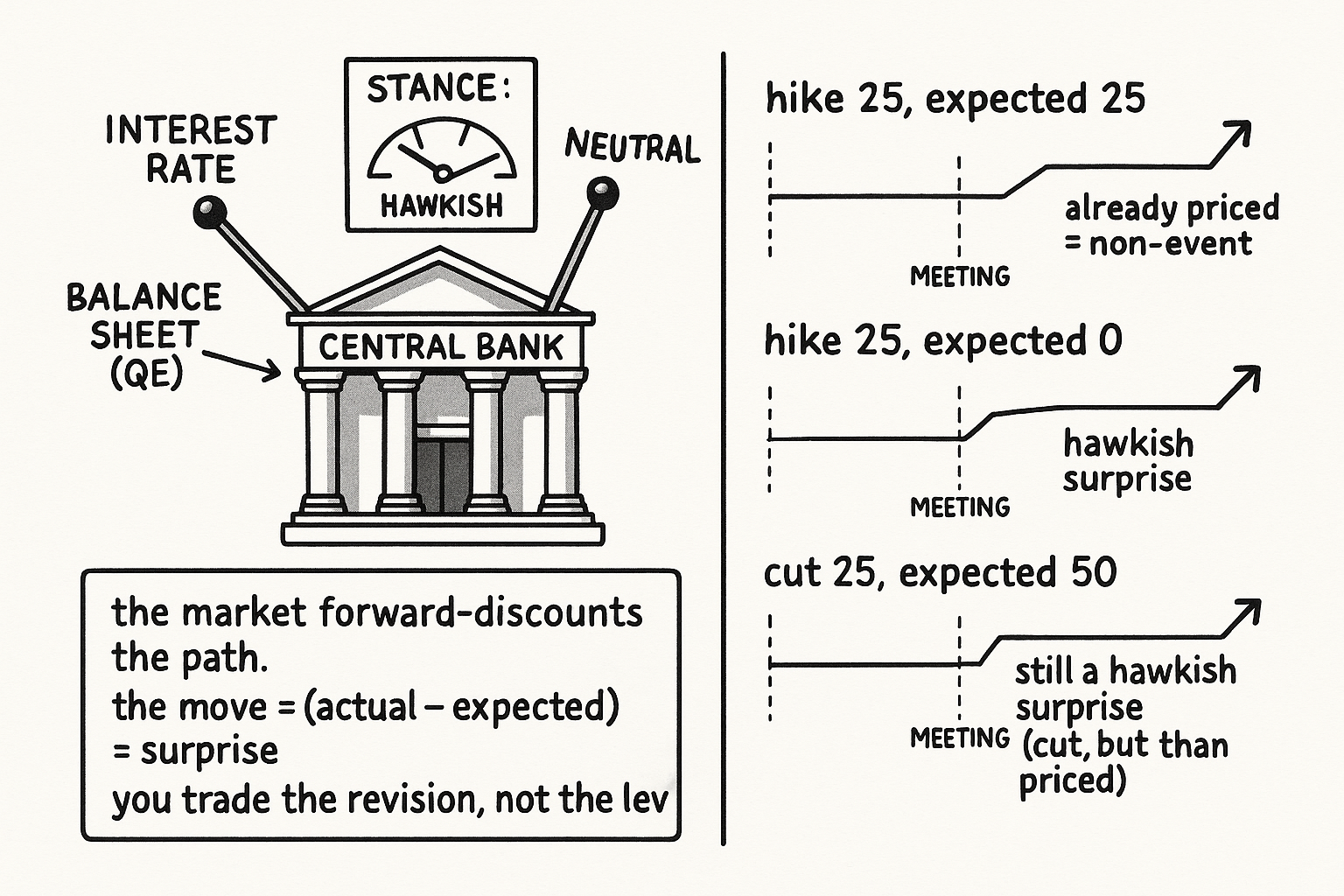

The interest rate is the primary lever and the one everybody watches: raise it and the currency's yield advantage grows, cut it and the advantage shrinks. The balance sheet is the second lever, the quantitative-easing and balance-sheet-management toolkit that central banks leaned on after the rate lever hit zero. Expanding the balance sheet floods the system with the currency and acts like an easing even when the headline rate does not move; shrinking it does the reverse. For most of the modern era rates were the whole story, but a trader who only watches the policy rate now misses half the stance, because a bank holding rates flat while expanding its balance sheet is easing through the back door.

The two levers combine into one thing the market actually trades: the stance, hawkish, dovish, or neutral. Hawkish means leaning toward tighter policy, higher rates or a shrinking balance sheet, which supports the currency. Dovish means leaning toward easier policy, which pressures it. Neutral means on hold. The stance is a direction, and the currency trades the change in direction more than the current setting.

The market forward-discounts the path

The core mechanic, the one that makes "cut equals rally" sane: the market does not wait for the central bank to act. It forward-discounts the anticipated path of rates, pricing expected future moves into the currency today.

$$ \Delta\text{FX} \;\propto\; \big(\text{actual policy} - \text{expected policy}\big) \;=\; \text{surprise} $$

The currency move is driven by the surprise, the gap between what the bank does (or signals) and what the market had already priced, not by the action in isolation. A 25 basis point hike into a market expecting 25 is a non-event; the move already happened when the expectation formed. A 25 hike into a market expecting nothing is a hawkish shock and the currency jumps. A 25 cut into a market braced for 50 is a hawkish surprise and the currency rallies on a cut. The level is old news the moment the market agrees on it. The trade lives in the revision of expectations, which is why currencies react violently to the unexpected and shrug at the expected.

This is also why the stance and the central bank's communication matter as much as the action. A bank can move the currency without touching rates at all, by shifting the expected path: a hawkish tilt in the statement, a dot-plot revision, a press conference that walks back a planned cut. The market reprices the whole forward path off the new information, and the spot currency moves now to reflect rates that have not happened yet and may never.

Banks carry a bias, and the bias is tradeable context

Central banks are not blank reaction functions. Each carries a historical bias baked in by its institutional memory, and the bias tilts how it responds to the same data. The Bundesbank's lineage runs hawkish, a hard preference for tight policy that traces directly to the long German memory of hyperinflation. The Federal Reserve has leaned toward keeping rates low for long stretches, a tilt that reflects the Keynesian center of gravity in US policy thinking. Same inflation print, different institutional reflex, different currency consequence.

The bias is not a signal by itself; it is prior context that shapes how you read the surprise. Knowing a bank runs dovish tells you it will take more inflation to provoke a hike than a hawkish bank would need, so the bar for a hawkish surprise is higher and the bar for a dovish confirmation is lower. It frames the distribution of likely outcomes before the meeting, which is exactly the kind of slow structural read that belongs in the regime layer. It does not tell you what prints tomorrow.

Trading it without trading it by hand

Monetary policy as the number-one driver does not mean trading central-bank meetings discretionarily, which is where the edge gets donated back. The honest structure is the one from the old article "Why FX Traders Need Macro but Should Trade Systematically": the policy read sets the gate, a rule-based system pulls the trigger. The stance and the rate-differential trajectory define the allowed direction, hawkish bank, widening differential, currency-supportive regime, and the systematic layer takes its signals inside that allowance.

The reason to keep hands off the trigger is the forward-discounting itself. By the time a policy shift is obvious enough to trade by gut, it is priced, and the discretionary trader ends up buying the currency at the top of the expectations move and holding through the "buy the rumor, sell the fact" reversal. The measurable inputs make the gate encodeable: the rate differential and its trend, the market-implied path from rate futures, the surprise index against consensus, all of which can be turned into a rule rather than a feeling. Encode the gate and you can backtest the policy overlay instead of trusting your read of a press conference. The residual that resists encoding, a genuine regime shift in a bank's reaction function, a credibility break, stays a slow human regime call, never a fast in-trade override. Policy chooses the direction; rules trade the path.

KEY POINTS

- Monetary policy is the single most consistent domestic driver of currencies most of the time, the mechanism behind its top ranking in the old article "Global vs Domestic Currency Drivers." It works through expectations, not the rate level.

- Two levers: the interest rate (primary, watched by all) and the balance sheet (QE and balance-sheet management). A bank holding rates flat while expanding its balance sheet is easing through the back door, so watching only the policy rate misses half the stance.

- The levers combine into a stance, hawkish, dovish, or neutral, and the currency trades the change in direction more than the current setting.

- The market forward-discounts the anticipated path, so the currency move is driven by the surprise (actual minus expected), not the action. A cut smaller than priced is a hawkish surprise and the currency rallies on a cut. Communication moves the currency without any rate change by shifting the expected path.

- Central banks carry historical biases (the Bundesbank hawkish from hyperinflation memory, the Fed tilted to low rates from Keynesian dominance). The bias is prior context that frames the distribution of outcomes and shapes how you read a surprise, not a signal by itself.

- Do not trade meetings by hand, since by the time a shift is obvious it is priced. Let the policy read set the gate (allowed direction from the stance and rate differential) and a rule-based system pull the trigger, the split from the old article "Why FX Traders Need Macro but Should Trade Systematically." The inputs are measurable, so the gate is encodeable and backtestable.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Monetary Policy and Exchange Rate Dynamics (Dornbusch overshooting)

- The Response of Exchange Rates to Monetary Policy Surprises (NBER)

- Central Bank Communication and Monetary Policy (Journal of Economic Literature)

- Quantitative Easing and Exchange Rates (BIS)

- Forward guidance (Wikipedia)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- Uncovered Interest Parity, Forward Guidance, and the Exchange Rate

- Foreign Safe Asset Demand and the Dollar Exchange Rate

- Monetary Policy and Exchange Rate Returns: Time-Varying Risk Premia in Foreign Currency Returns

- Monetary Policy Surprises and Exchange Rate Behavior

- The Impact of Monetary Surprises on Exchange Rates: Results from Textual and High-Frequency Analysis

- Exchange Rate Dynamics and the Central Bank’s Balance Sheet

- The Relevance or Otherwise of the Central Bank’s Balance Sheet

- Exchange Rates, Yield Curves and Transitory Risk