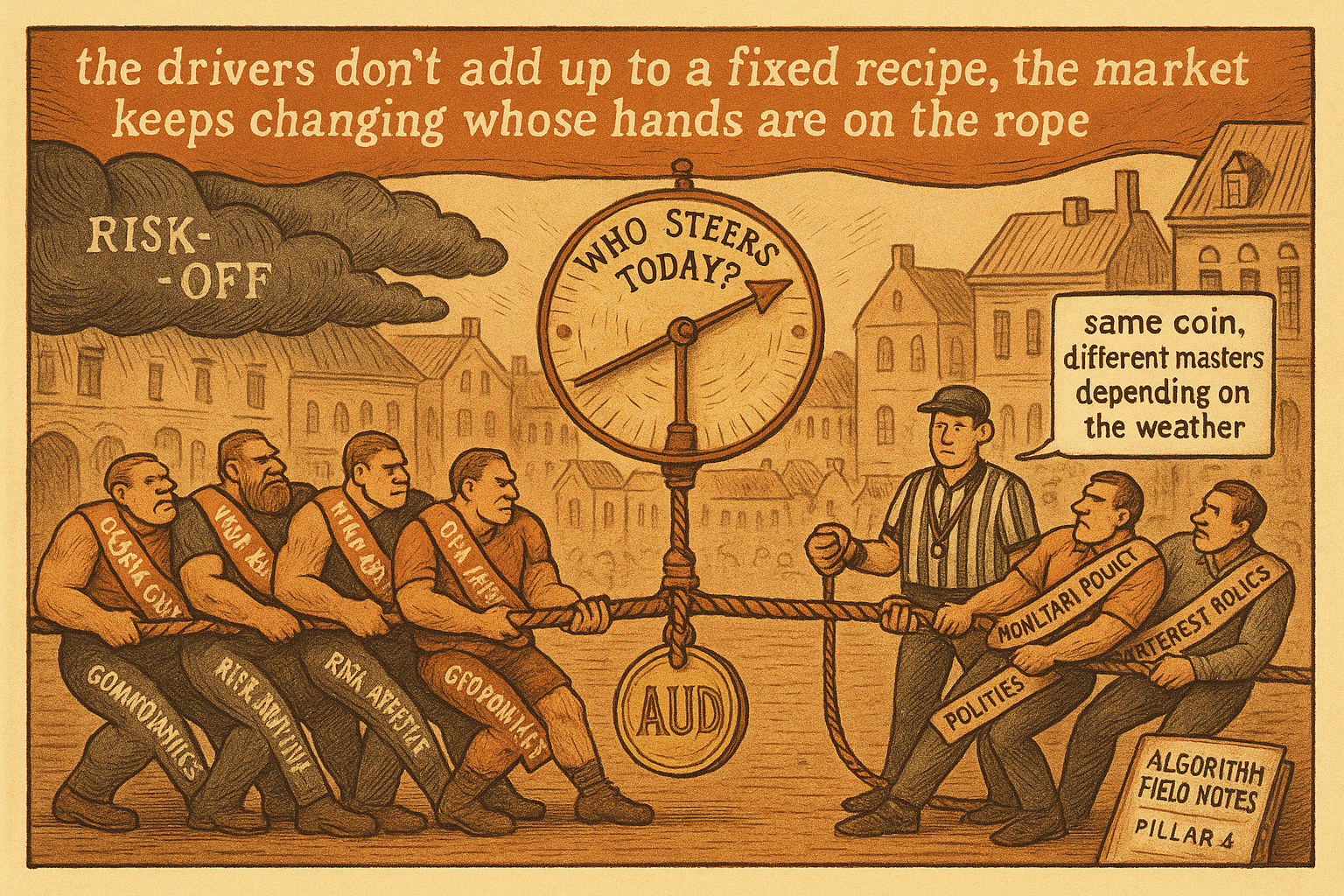

4.64 Global vs Domestic Currency Drivers

A currency is pulled by four global drivers and three domestic ones at once, and the market keeps switching which set steers. Read the regime before the news, or trade the right analysis in the wrong direction.

Same currency, same week, two opposite explanations. On Monday the Australian dollar rallies and the desk says iron ore and a risk-on tape. On Friday it sells off and the desk says soft local jobs data and a dovish RBA. Both are right. What changed is not the currency. What changed is which set of drivers the market decided to price. A currency is pushed by global forces and domestic forces at the same time, and the market oscillates over which set is in charge. Read the wrong set on the wrong day and your correct analysis gets the direction backwards.

The drivers split into two buckets. Four are global, shared across currencies and set by the state of the world. Three are domestic, specific to the country. They are tangled together, but the practical skill is knowing which bucket holds the steering wheel right now, because the answer rotates and the rotation is the part that breaks naive models.

The four global drivers

Global growth comes first because it moves money around the planet. When growth is strong, capital flows toward exporters and the currencies levered to expansion, the Chinas and Koreas and Brazils of the world. When growth weakens, money retreats to safe havens, the Swiss franc and often the dollar, regardless of what those economies are doing domestically. Growth is the tide, and the tide sets the baseline direction for a whole class of currencies at once.

Commodity prices are the second, driven mostly by global growth but kicked around by weather, supply, production, and the fashion of treating a commodity as an asset class. Exporters benefit when prices rise: Brazil, Canada, Australia carry strong terms of trade when their exports get dear. Importers get hurt on the same move: Turkey and India bleed when energy and food climb. One commodity move splits the currency universe into winners and losers along the export-import line.

Risk appetite is the third and the most violent. Global risk-on and risk-off moves the currencies regardless of any domestic fundamental. In a risk-off panic, nobody is pricing the Australian jobs report; they are selling the high-beta currencies and buying havens because the world turned scared, and the local data sheet goes in the bin. Geopolitics is the fourth, often working through risk appetite, sometimes hitting affected countries directly. Instability in Russia sells the ruble, the zloty, and the lira together as the market dumps regional risk, not because three central banks moved but because one map got more dangerous.

The three domestic drivers

Monetary policy is the number-one domestic driver most of the time, the relative interest-rate setting and the central-bank stance. It gets its own treatment in the old article "Monetary Policy and Central-Bank Bias as the #1 FX Driver," so the short version here: rate differentials and the expected path of policy are the most consistent domestic engine, and currencies react hard to surprises in them.

Interest rates are the second, closely tied to policy but worth separating because the market trades the relative differential and its changes, not the level. The third is politics, the elections, fiscal fights, and institutional shocks that move a currency through its own internal story. Domestic drivers are the engine when the world is calm. Stable global backdrop, no panic, no commodity shock, and the market goes back to pricing local rates and local data, which is when fundamental analysis of a single economy actually pays.

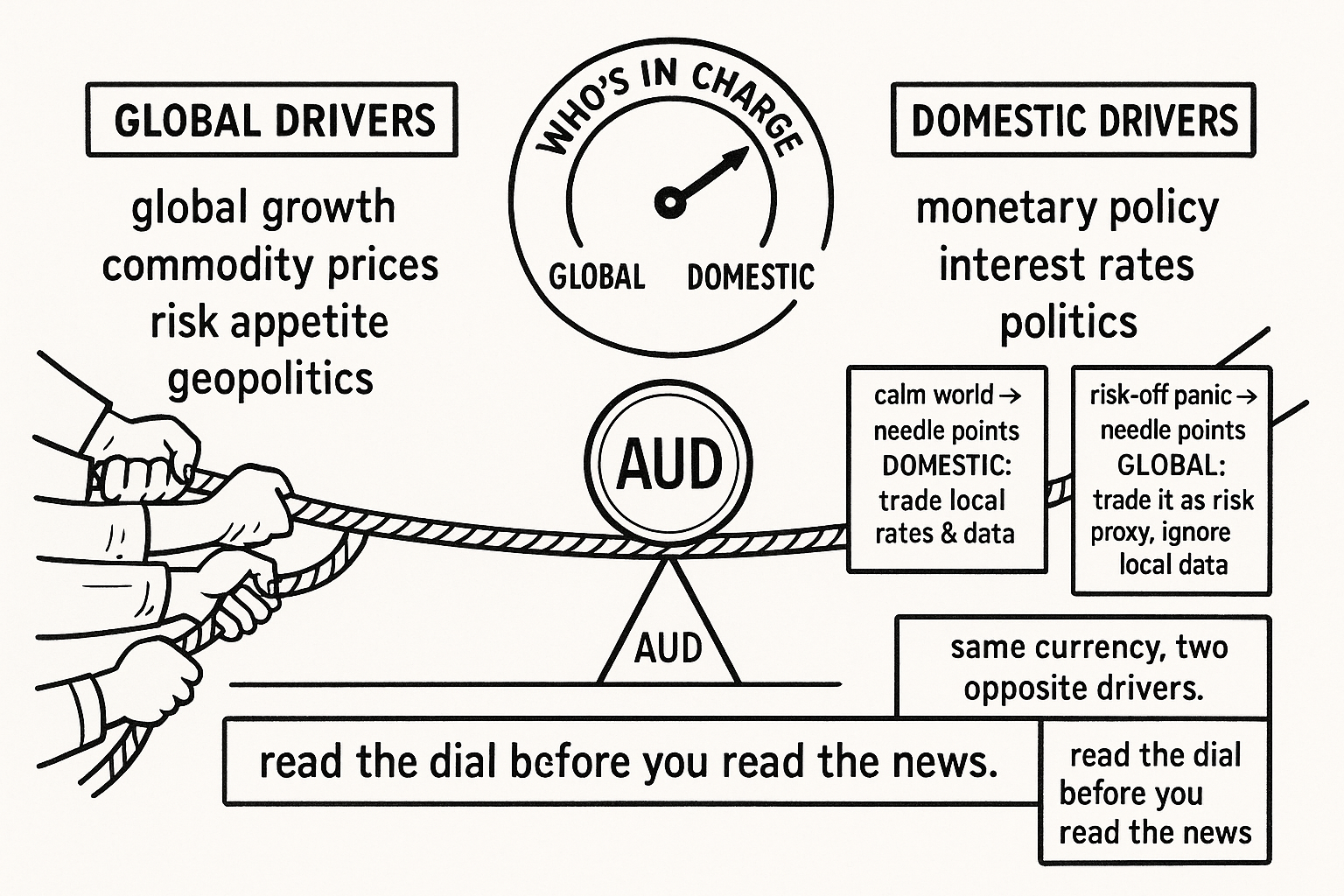

The oscillation is the whole game

The drivers do not add up to a fixed weighting. The market swings between regimes where global factors dominate and regimes where domestic factors dominate, and the swing is what wrecks a model built on one bucket.

$$ \Delta\text{FX}_t \;=\; w_t \cdot (\text{global drivers}) \;+\; (1 - w_t)\cdot(\text{domestic drivers}), \qquad w_t \in [0,1] $$

Read the weight, not the symbols: a currency's move on any day is a blend of the global bucket and the domestic bucket, and the blend weight shifts over time. In a calm world the weight on global sits low and local rates and data drive the currency, so a hawkish surprise from the local central bank sends it up cleanly. In a risk-off episode the weight on global swings toward one and domestic drivers go to irrelevant, so that same hawkish surprise gets steamrolled by a flight to havens and the currency falls anyway. The weight is not constant and it is not observable on a fixed schedule, which is why a regression with static coefficients keeps getting the regime wrong precisely when the regime matters most.

This is the same non-stationarity that runs through the old article "Why FX Traders Must Watch Gold, Rates, and Equities." That article said to watch gold, rates, and equities together and count confirmations; the driver framework here says why the count rotates. Gold and the risk tape carry weight when the global bucket is in charge; the rate differential carries weight when the domestic bucket is in charge. The confirmation that mattered last month can be noise this month because the weight moved underneath it.

Trading the regime, not the average

The usable discipline is to first identify which bucket is driving, then read the matching signals, and to treat that identification as the slow regime call it is. In a risk-off or China-obsessed tape, stop pricing local data and trade the currency as a risk proxy: where does it sit in the high-beta-to-haven spectrum, and which way is global risk leaning. In a calm tape, switch back to the domestic engine and trade the rate differential and the local data flow. The error is running one playbook through both regimes, which guarantees you fight the tape on every transition.

Detecting the switch is the hard part, and it is mostly a context read rather than a clean indicator: a spike in cross-asset correlation, equities and FX and credit all moving as one bloc, is the tell that the global bucket has taken over, a pattern the intermarket articles return to. The honest limit is that the weight is latent and you infer it after it has already started moving, so this framework sets the regime gate and never the trigger. It tells you which set of inputs deserves your attention this week. Pair it with the systematic execution from the old article "Why FX Traders Need Macro but Should Trade Systematically," where the driver read sets the allowed direction and a rule-based system pulls the trigger inside it. Macro picks the bucket; rules trade it.

KEY POINTS

- A currency is pushed by four global drivers and three domestic drivers at once, and the market oscillates over which bucket is in charge. Reading the wrong bucket on the wrong day gets your direction backwards.

- Global drivers: global growth (the tide that moves capital toward exporters or havens), commodity prices (splits the universe into exporter winners and importer losers), risk appetite (moves currencies regardless of domestic fundamentals), and geopolitics (often via risk appetite, sometimes direct).

- Domestic drivers: monetary policy (number one most of the time), interest rates (the traded relative differential), and politics. These drive when the world is calm.

- The blend weight between buckets is not fixed and not observable on schedule, which is why static-coefficient models get the regime wrong exactly when it matters. In risk-off, domestic drivers go to irrelevant and the currency trades as a risk proxy.

- This is the non-stationarity behind the old article "Why FX Traders Must Watch Gold, Rates, and Equities": gold and the risk tape carry weight in the global regime, the rate differential in the domestic regime, and the confirmation that mattered last month can be noise now.

- Trade the regime, not the average: identify the bucket first, then read the matching signals. A cross-asset correlation spike (equities, FX, credit moving as one) signals the global bucket has taken over. The weight is latent, so use this as a regime gate and pair it with systematic execution, the way the old article "Why FX Traders Need Macro but Should Trade Systematically" splits the gate from the trigger.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Exchange Rate Fundamentals and Order Flow (NBER)

- Carry Trades and Global Foreign Exchange Volatility (Journal of Finance)

- Risk Appetite and Exchange Rates (NY Fed)

- Commodity Currencies (Chen and Rogoff)

- The Dollar and Global Risk (BIS)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- Commodity prices, commodity currencies, and global economic activity

- Commodity Currencies and Monetary Policy

- The Relationship between Commodity Prices and Currency Returns

- Can commodity prices forecast exchange rates?

- International capital flow pressures and global factors

- A global perspective on exchange rate dynamics via currency factors

- Liquidity in the global currency market

- Order flow and exchange rate comovement