4.63 PPP and the Big Mac Index: Why Valuation Only Matters Long-Term

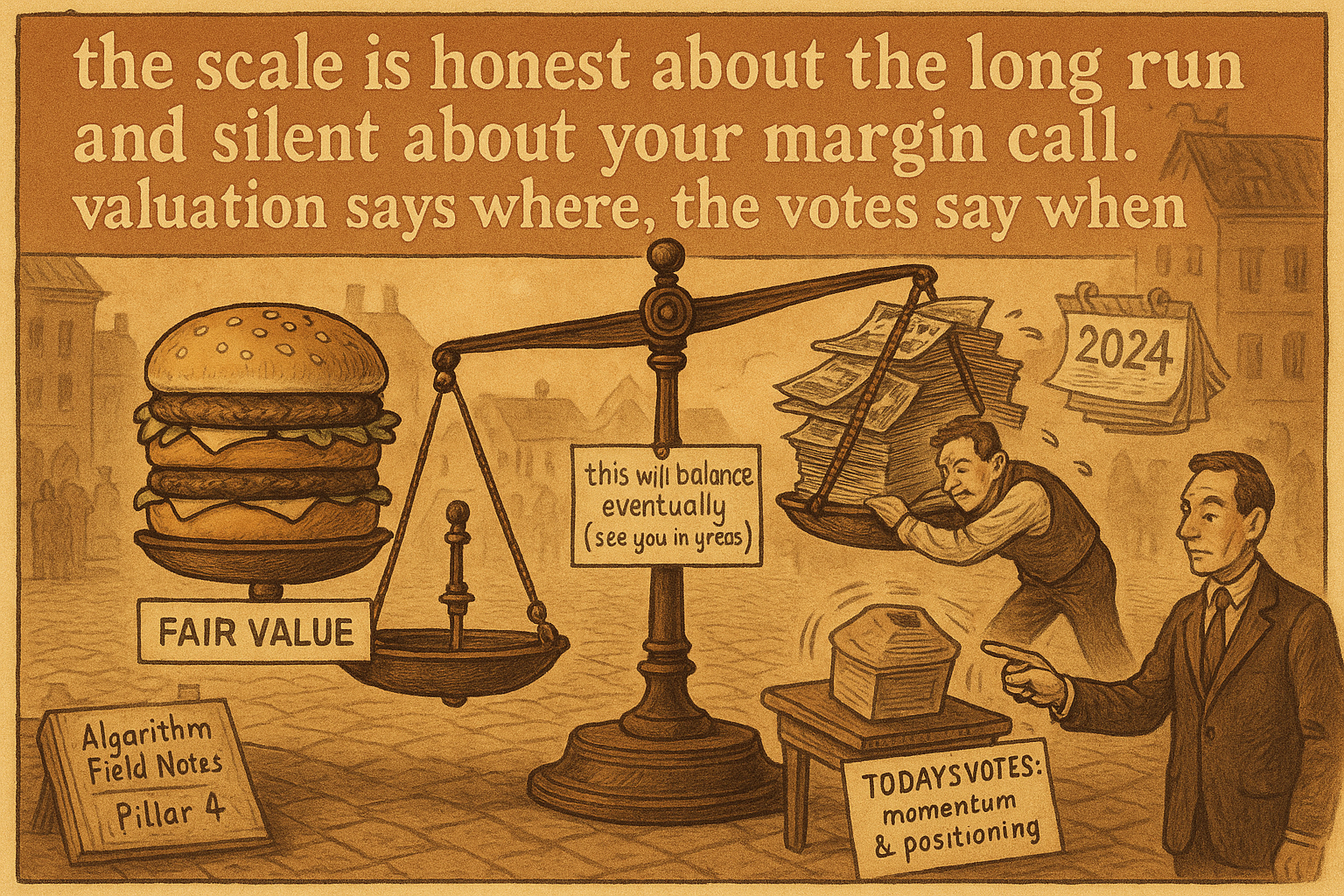

PPP and the Big Mac index value a currency honestly and time it terribly. A currency stays mispriced longer than you can stay short. Valuation says where, momentum and positioning say when.

A Big Mac costs about 30 percent more in dollars when you buy it in Zurich than in New York. Purchasing power parity reads that gap and announces the franc is overvalued. The conclusion is correct and the trade built on it is a grave. You can short the franc against that 30 percent for three years and bleed out long before the gap closes, because the gap closes on a clock that has nothing to do with your margin call. Valuation tells you where the currency should be. It says nothing about when, and in FX the when is the whole problem.

Purchasing power parity is the most common framework for valuing a currency, and the Big Mac index is its cartoon version. Both rest on one idea: a basket of goods should cost the same across countries once you convert through the exchange rate, and relative inflation should be the thing that keeps the prices aligned. If a good is cheaper in one country, buyers shift demand there, the demand pulls on the currency, and over a long enough horizon the prices reconverge. That is the law of one price stretched across borders.

The arithmetic, and why it disappoints

The mechanics are simple enough to write on a napkin.

$$ S_{\text{PPP}} = \frac{P_{\text{domestic}}}{P_{\text{foreign}}} \qquad\qquad \%\Delta S \;\approx\; \pi_{\text{domestic}} - \pi_{\text{foreign}} $$

The left equation is absolute PPP: the fair exchange rate equals the ratio of the two countries' price levels, so if the same basket costs 6.50 in Switzerland and 5.00 in the United States, the franc's fair value against the dollar is 6.50 divided by 5.00, about 1.30. The Big Mac index just uses one burger as the basket. The right equation is relative PPP: the exchange rate should drift by the inflation differential over time, so if Swiss inflation runs two points below US inflation, the franc should appreciate about two percent a year against the dollar to keep the burger prices in line. Both are clean. Both are nearly useless for trading.

The reason is buried in the assumptions. The basket is not actually traded across borders (you cannot arbitrage a haircut or a Zurich rent), goods carry different tax and labor and transport costs in each country, and the convergence force is real but glacial. Orthodox economics piles on enough faulty premises that by the time you try to put PPP on a trade, the edge has leaked out of every joint. PPP gives you a starting point to call a currency cheap or rich. It does not give you a timer, and a valuation signal without a timer is a thesis, not a trade.

Mispricing is not a countdown

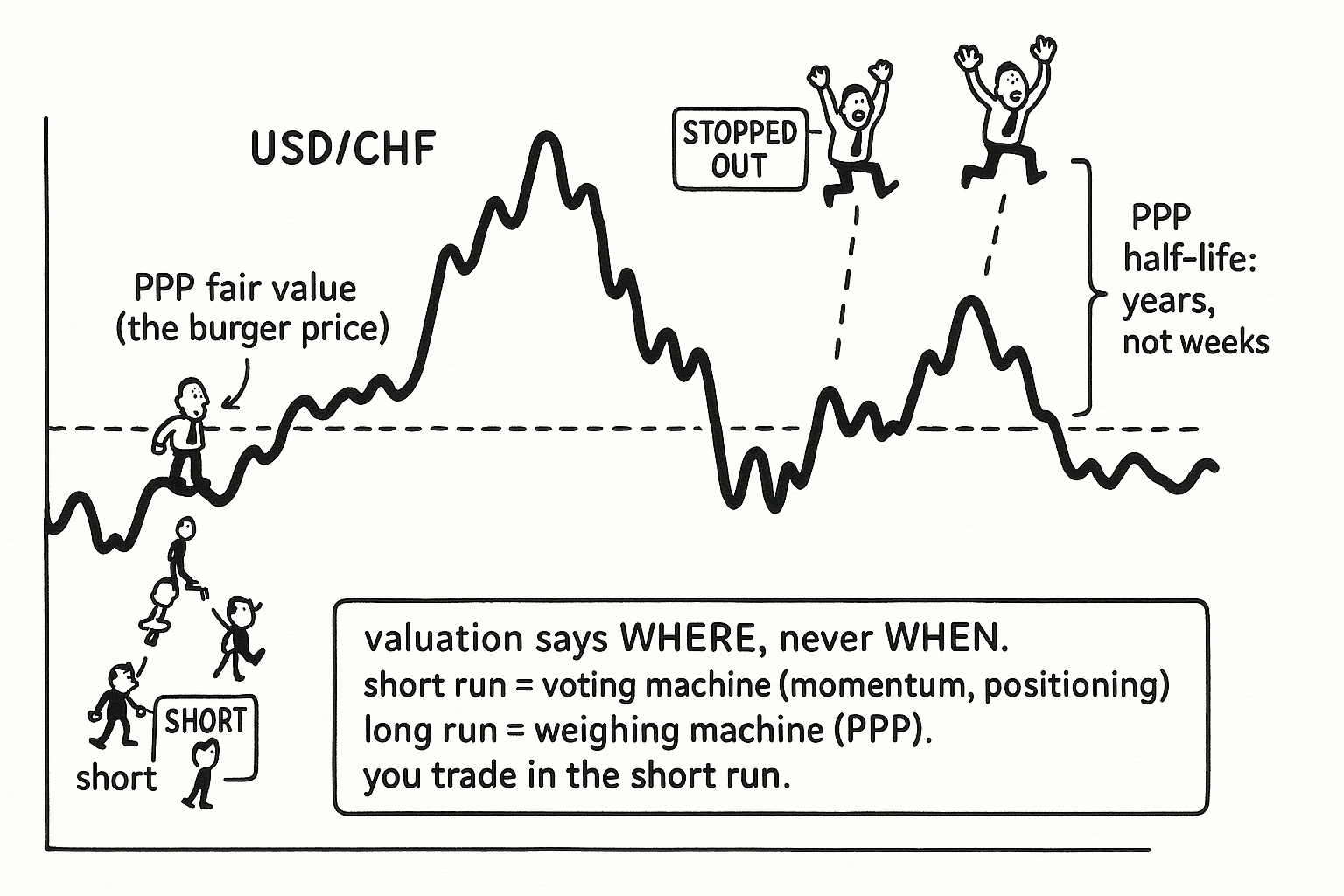

The trap is treating "overvalued" as "about to fall." A currency can stay overvalued or undervalued far longer than you can stay short, and the FX graveyard is full of traders who were right about fair value and wrong about their financing. The mispricing is not a coiled spring. It is a slope that the market climbs and descends on its own schedule, driven by flows and positioning that ignore the burger entirely.

The cleanest way to hold this is the old Graham line: in the short run the market is a voting machine, in the long run a weighing machine. PPP is the scale in the long run. Day to day, week to week, even year to year, the currency is being voted on by speculators whose decisions run on momentum, carry, risk appetite, and emotion, none of which care that the franc is 30 percent rich. The market oscillates above and below fair value because the voting dominates, and only over the super long term does the weighing pull price back toward the equilibrium the napkin math predicts. Estimates of PPP half-lives in floating rates run to several years, which is to say the reconvergence is real and slower than almost any position you would put on.

PPP explains, it does not predict

This is the same distinction the old article "The Difference Between Explanation and Prediction in Markets" drew, applied to valuation. A prediction commits before the outcome and gets dated and scored. An explanation is assembled after, with the answer already visible. PPP is built for explanation. When a currency has spent five years grinding back toward fair value, PPP narrates the move with total confidence and zero risk, because it had the answer the whole time. Run it forward as a dated signal ("the franc is rich, so short it now") and it produces no usable timing and a string of stopped-out shorts.

That is why PPP belongs in the regime layer, not the trigger layer. It is the kind of slow, structural context the old article "Why FX Traders Need Macro but Should Trade Systematically" said macro is for: it tells you which direction the multi-year wind leans, so you do not fight a long-run reconvergence with a structural short forever. It never sets an entry. Valuation chooses the backdrop; positioning and momentum choose the trade. Confuse the two and you have converted a true statement about the next decade into a losing position this quarter.

Where it earns its keep

PPP is not worthless. It is a horizon tool used at the right horizon. For a multi-year allocation, a currency trading 30 percent above its PPP estimate carries a structural headwind that a one-week momentum signal cannot see, and ignoring it means sizing a long-term position against a slow but persistent drag. The honest use is asymmetric: let extreme PPP mispricing veto a structural position in the wrong direction, and let it lean a long-horizon allocation toward the cheap side, but never let it pull a trigger or set a stop. The further price sits from fair value, the more the long-run odds favor reconvergence, and the less that tells you about the next hundred trading days.

The discipline is to keep the timeframes from contaminating each other. A trader who lets a multi-year valuation view leak into a short-term book starts holding losers "because the franc is rich anyway," which is the cognitive defect of the voting-machine world wearing the costume of the weighing-machine truth. Valuation matters in the super long term. Positioning and momentum matter for everything shorter, which is everything you will actually trade.

KEY POINTS

- Purchasing power parity (and its cartoon, the Big Mac index) values a currency by saying the same basket of goods should cost the same across borders, with relative inflation as the equalizer. Absolute PPP sets fair value as the ratio of price levels; relative PPP says the rate should drift by the inflation differential.

- The math is clean and nearly useless for trading. The basket is not arbitrageable across borders, costs and taxes differ by country, and convergence is glacial, with PPP half-lives running to years in floating rates.

- A currency can stay mispriced far longer than you can stay short. Mispricing is a slow slope, not a coiled spring, so "overvalued" does not mean "about to fall."

- Graham's frame: short run the market is a voting machine (momentum, positioning, emotion), long run a weighing machine (fair value). PPP is the long-run scale; the voting dominates every horizon you actually trade.

- PPP explains beautifully after the fact and predicts nothing on a dated basis, the explanation-versus-prediction split from the old article "The Difference Between Explanation and Prediction in Markets." Keep it in the regime layer, never the trigger layer.

- Honest use is asymmetric and slow: let extreme mispricing veto a wrong-way structural position or lean a multi-year allocation toward the cheap side, but never set an entry or stop with it. Valuation chooses the backdrop, positioning and momentum choose the trade.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Purchasing Power Parity (PPP) in the Long Run

- A Panel Project on Purchasing Power Parity: Mean Reversion within and between Countries

- The Big Mac Index (The Economist)

- Purchasing power parity (Wikipedia)

- The Purchasing Power Parity Debate (Journal of Economic Perspectives)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- Burgernomics: the economics of the Big Mac standard

- The Micro-foundations of Big Mac Real Exchange Rates

- What does purchasing power parity mean?

- The PPP Puzzle: Some New Evidence

- The evolution of purchasing power parity

- FX Trading and Exchange Rate Dynamics

- An Approach for Determining Exchange Rates: The Mixture of the