1.20 The Difference Between Explanation and Prediction in Markets

A market prediction commits before the outcome. A market explanation chooses after the outcome. The first is hard and economically useful. The second is cheap and psychologically comforting. Most commentary is explanation dressed in the grammar of prediction.

A market prediction is a statement made before an outcome about what the outcome will be. A market explanation is a statement made after an outcome about why the outcome occurred. The two look similar on the page and behave differently when capital is at stake.

Prediction is economically useful and statistically demanding. Explanation is psychologically comforting and statistically cheap. Mistaking one for the other is the most common cognitive failure in market commentary and one of the most expensive errors in trading. The fix is to be precise about which side of the outcome the claim was constructed on.

The temporal definition

The cleanest version of the distinction is temporal.

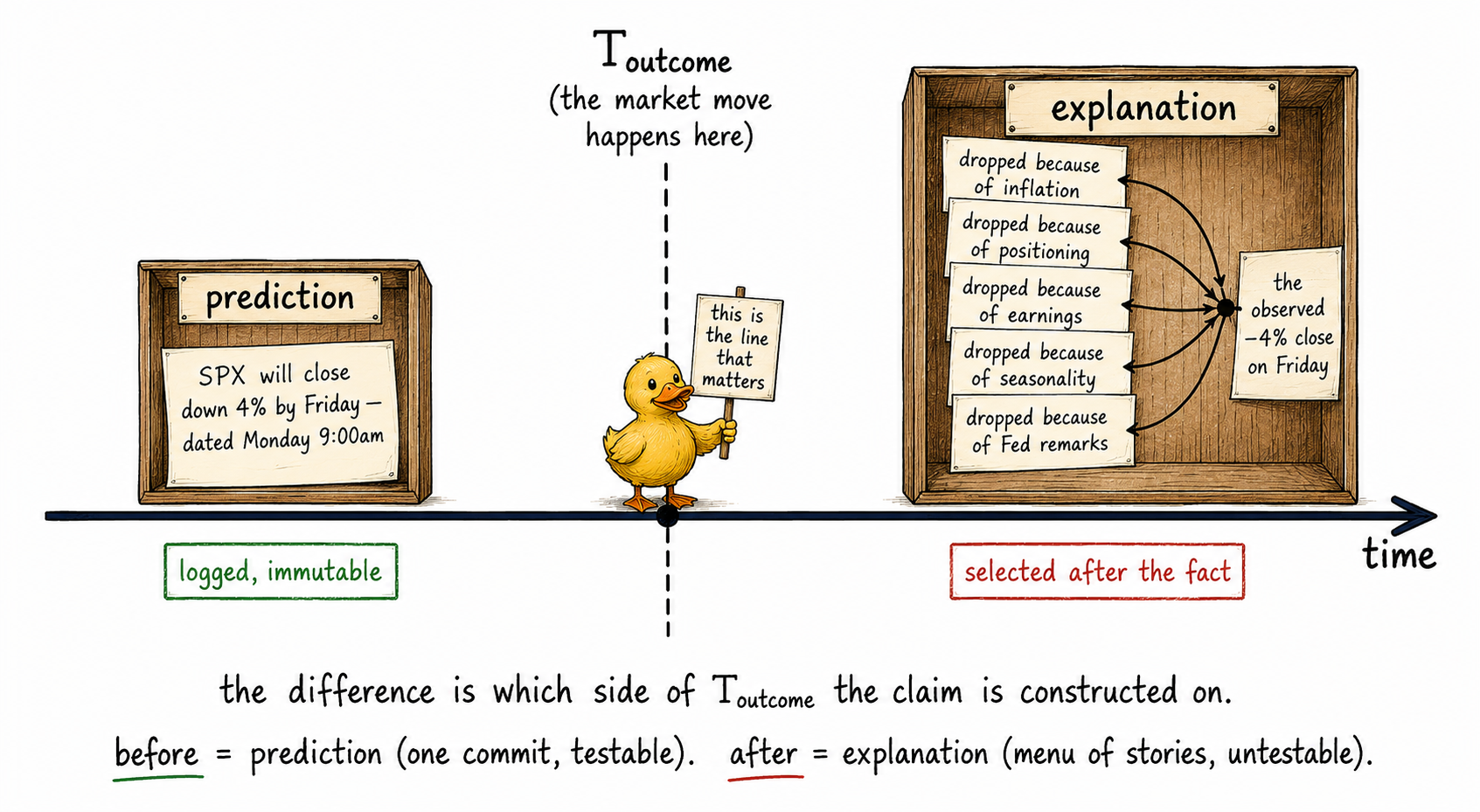

Where Y is the outcome variable (next-week return, year-end index level, recession indicator), X is the available information, and f and g are functions that map information to claims about Y. The function f is computed before knowing the outcome. The function g is constructed after knowing the outcome.

The mathematical difference is which side of T_outcome the inference happens on. The practical difference is which functions are available. After T_outcome, g has access to Y itself when picking which variables in X matter. Before T_outcome, f does not.

The information asymmetry is the entire distinction. Prediction commits without knowing the answer. Explanation chooses with the answer in hand.

Why explanation is cheap

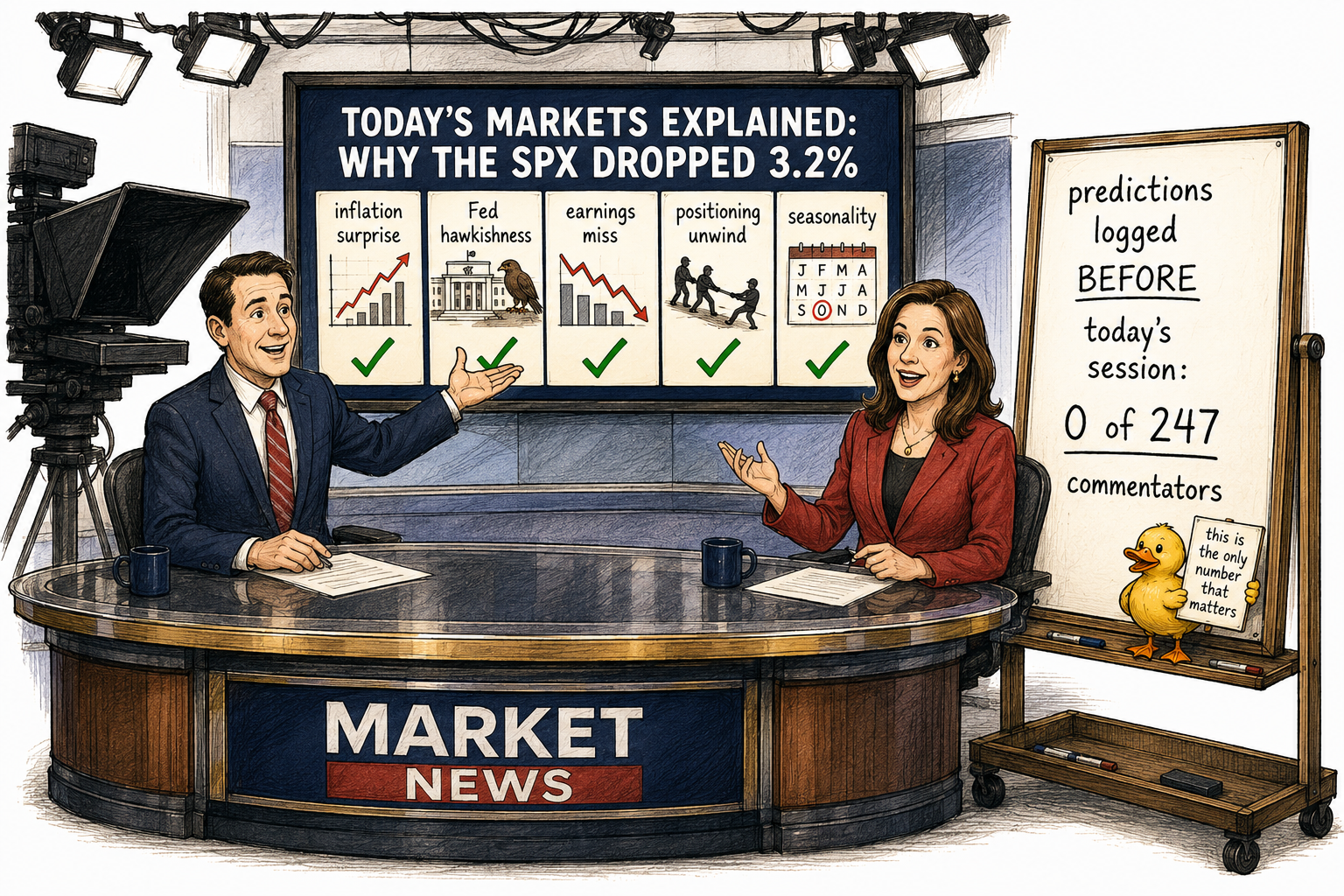

Any market event has many possible explanations. Markets rose because inflation cooled. Markets rose because earnings surprised. Markets rose because liquidity expanded. Markets rose because positioning was short. Markets rose because seasonality was favorable. Markets rose because the calendar flipped. Each of these claims can be supported by selectively cited data. None of them is uniquely correct in any rigorous sense.

After the outcome is known, the explainer picks the explanation that fits. The fit is engineered, not discovered. The explanation feels correct because the explainer used the outcome to select among a menu of post-hoc stories.

The cost of generating an explanation is approximately zero. The market dropped. Six explanations are available within an hour. Most newsroom commentary is the production of these explanations at industrial scale. The activity is sometimes useful for entertainment. It is not useful for trading.

Why prediction is hard

A prediction commits in advance. Once committed, the prediction is right or wrong when the outcome arrives. There is no menu to choose from after the fact.

A real prediction has three properties.

- Dated. The prediction was made at a known time before the outcome was known.

- Specific. The prediction names a variable, a direction, a magnitude, and a horizon.

- Preserved. The prediction is logged in a way that cannot be edited after the outcome arrives.

Almost no published market commentary meets these three criteria. The few participants who do (registered investment advisors making numerical forecasts, hedge funds with publicly tracked performance, prediction market participants) are the only ones whose claims can be evaluated as predictions. Everyone else is making explanations dressed in the grammar of predictions.

The four scenarios

Models in markets fall into four categories based on whether they predict and whether they explain.

Predicts and explains. The ideal scientific model. It produces accurate forward forecasts and provides a mechanism by which the forecasts work. This category is rare in markets and common in physics.

Predicts but does not explain. Pure statistical edge. A black-box model that produces accurate forecasts without anyone understanding why. Plenty of profitable strategies fall into this category. The trader does not know the mechanism but can verify the prediction.

Explains but does not predict. Economic theory that produces compelling causal stories but no measurable forward edge. Much of behavioral finance falls into this category. The story is satisfying. The trading P&L is flat or negative.

Does neither. Most market commentary. The commentator produces a satisfying narrative after the event with no demonstrable forecasting record. The narrative is consumed for the comfort of feeling that something is understood, not for any operational use.

The trader who confuses categories 2 and 3 is dangerous to themselves. A predictive model with no explanation is profitable and uncomfortable. An explanatory model with no prediction is unprofitable and comfortable. Choosing the latter for psychological reasons is one of the more common ways to lose money in markets.

The retail trap

The retail trap is reading post-event explanations as if they were pre-event predictions. The cognitive process looks like this:

The market dropped 4% yesterday. A commentator explains that the drop was caused by hawkish Fed remarks. The commentator's tone is confident. The story is internally coherent. The reader concludes, implicitly, that the same commentator could have predicted the drop in advance. Therefore the reader believes the commentator has predictive insight.

Each step in this chain is wrong. The commentator did not commit to this explanation in advance. The commentator had hundreds of possible explanations available and picked the one that fit. The internal coherence of the story is a feature of human storytelling, not evidence of predictive accuracy. The implicit transfer from "explains well" to "predicts well" is unjustified.

The fix is to track. Anyone who claims predictive insight should be willing to log forecasts before outcomes. The forecast log is the only evidence that the claimed insight exists. In the absence of a log, every confident explanation should be read as an explanation, not a prediction.

The hindsight engine

Hindsight bias is the cognitive tendency to view past events as more predictable than they were before they occurred. The mechanism is selective recall: the explainer remembers the cues that pointed toward the outcome and forgets the cues that pointed the other way. The result is a sincere belief that the outcome was foreseeable, even when no one foresaw it.

Markets are an unusually fertile environment for hindsight bias because the available information at any moment supports many possible narratives, and the outcome eliminates all but one. After the dust settles, the surviving narrative looks inevitable. The trader who internalizes the surviving narrative as evidence of foresight is feeding their hindsight bias and learning nothing about the future.

The corrective is to write forecasts down before the outcome. The written forecast is immune to selective recall. Six months later, the reader can compare what was actually predicted to what actually happened, with no opportunity to retroactively edit the prediction to match the outcome.

Visualizing the temporal asymmetry

The picture is the entire distinction in one image. Everything on the left side commits before knowing. Everything on the right side selects after knowing. The geometry of the time axis is the structure of the difference.

When each is useful

Prediction and explanation each have legitimate uses. The error is using one in place of the other.

Prediction is the basis of alpha. Every trading strategy is a prediction generator. The strategy says: at this point in time, given this information, the expected return of this position is X. The position is taken. The outcome arrives. The prediction is right or wrong. Aggregated over many predictions, the strategy has a measurable edge or it does not.

Explanation is the basis of risk decomposition and post-mortem learning. When a strategy loses money, explanation answers the question of which exposure failed. When a portfolio's drawdown is larger than expected, explanation answers the question of which tail risk realized. This kind of explanation is bounded and useful because it operates on data that already exists and helps the next prediction be better calibrated.

The error is using explanation as a substitute for prediction. "The strategy lost because of X" is a partial answer if the next version of the strategy will use X as a forward predictor and avoid the same exposure going forward. It is not a complete answer if no such forward use is planned and the explanation is consumed for its narrative coherence alone.

What this changes operationally

Three concrete consequences.

Treat every piece of market commentary you read as explanation by default. Until proven otherwise with a dated forecast log, the commentator is producing post-hoc stories. Read for curiosity, not for operational decisions.

Build prediction systems that log forecasts before outcomes arrive. The log is the asset. Without it, the system cannot be evaluated as a predictor, only as an explainer. A trader who runs a strategy without logging forecasts is doing prediction and explanation simultaneously and cannot tell which one is responsible for the results.

Separate post-mortems from forecast generation. After a loss, write down the explanation. Use the explanation to refine the prediction system for the next period. Do not promote an explanation to the status of prediction without an explicit forward test against new data.

KEY POINTS

- A prediction is a statement about an outcome made before the outcome is known. An explanation is a statement about an outcome made after the outcome is known. The difference is which side of T_outcome the inference happens on.

- Explanation is cheap because the explainer has access to the outcome and can select from many possible stories. Prediction is hard because it commits to one claim before any selection is possible.

- A real prediction has three properties: dated, specific, and preserved in a way that cannot be edited after the outcome arrives.

- Models fall into four categories: predicts and explains (ideal), predicts but does not explain (statistical edge, often profitable), explains but does not predict (most behavioral finance, comfortable but unprofitable), does neither (most market commentary).

- The retail trap is reading post-event explanations as evidence of predictive insight. The explainer's confident narrative is a feature of storytelling, not evidence of forecasting accuracy.

- Hindsight bias makes outcomes look more predictable than they were because the surviving narrative is remembered and the discarded ones are not. The corrective is written forecasts that cannot be edited after the fact.

- Prediction is the basis of alpha. Explanation is the basis of risk decomposition and post-mortem learning. Each has legitimate uses; substituting one for the other is the standard error.

- The only evidence that a commentator has predictive insight is a dated forecast log. In the absence of a log, every confident explanation should be read as explanation, not prediction.

- Operational fix: treat market commentary as explanation by default, log forecasts before outcomes arrive, separate post-mortem explanation from prediction generation, and refuse to promote an explanation to a prediction without an explicit forward test.

References

- Evidence-Based Technical Analysis - David Aronson (Amazon)

- Systematic Trading - Robert Carver (Amazon)

- Evidence-Based Technical Analysis: Applying the Scientific Method and Statistical Inference to Trading Signals

- A Comprehensive Review of Statistical Methods in Quantitative

- The Rise of Algorithmic Retail Option Traders

- 1 Hypothesis Testing Ordinary Meaning Daniel Keller – Northern

- Structural Market Modeling vs Heuristic Trading Concepts A

- Research Methodology

- Policy Experiments - Cambridge University Press & Assessment

- Increase Alpha: Performance and Risk of an AI-Driven Trading