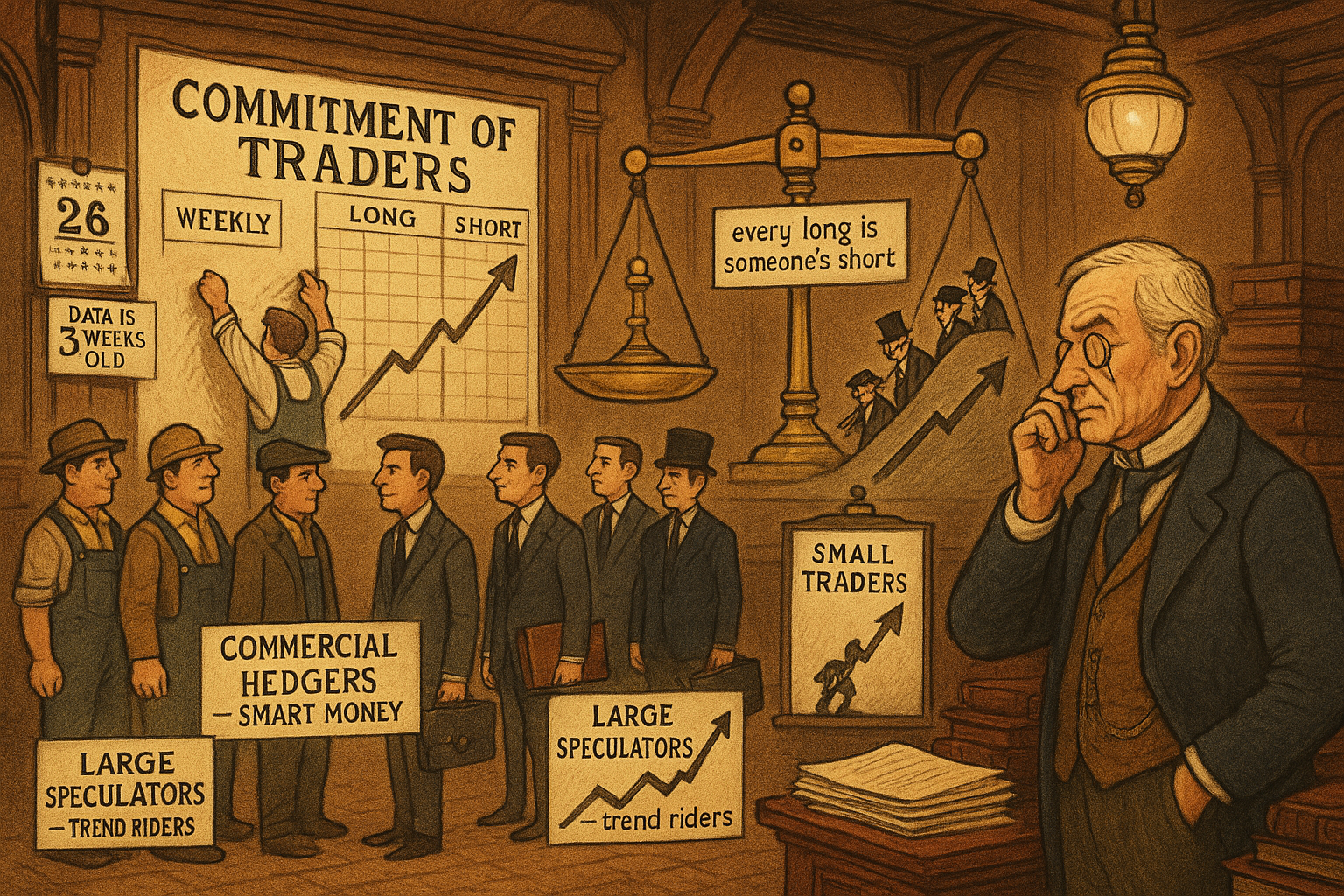

4.45 Reading the COT Report: Three Trader Groups, One Edge

The Commitment of Traders is a weekly census of who owns the futures market. Split it into hedgers, funds, and retail, watch the smart money, and remember the numbers reach you three weeks late.

Every Friday the regulator publishes a census of who owns the futures market. Not price, not volume, but positions: how many contracts each kind of trader is long and short in every major futures market. Most traders never open it. The ones who do are reading the only public dataset that tells you what the people with the deepest pockets and the best information are actually doing with their money, instead of what they say on television. The Commitment of Traders report is that census, and the edge in it comes from splitting the market into three groups that behave in completely different ways.

This is intermarket analysis turned inward. The "Intermarket Analysis for System Traders" article gated one market's signals on the state of another market; COT gates a market's signals on the positioning inside that same market. Instead of asking "what are bonds doing while I trade stocks," you ask "who is long this contract, and are they the smart money or the dumb money." Same discipline, different axis. The data is positional, not price-derived, which is exactly why it adds something a chart cannot.

The three groups

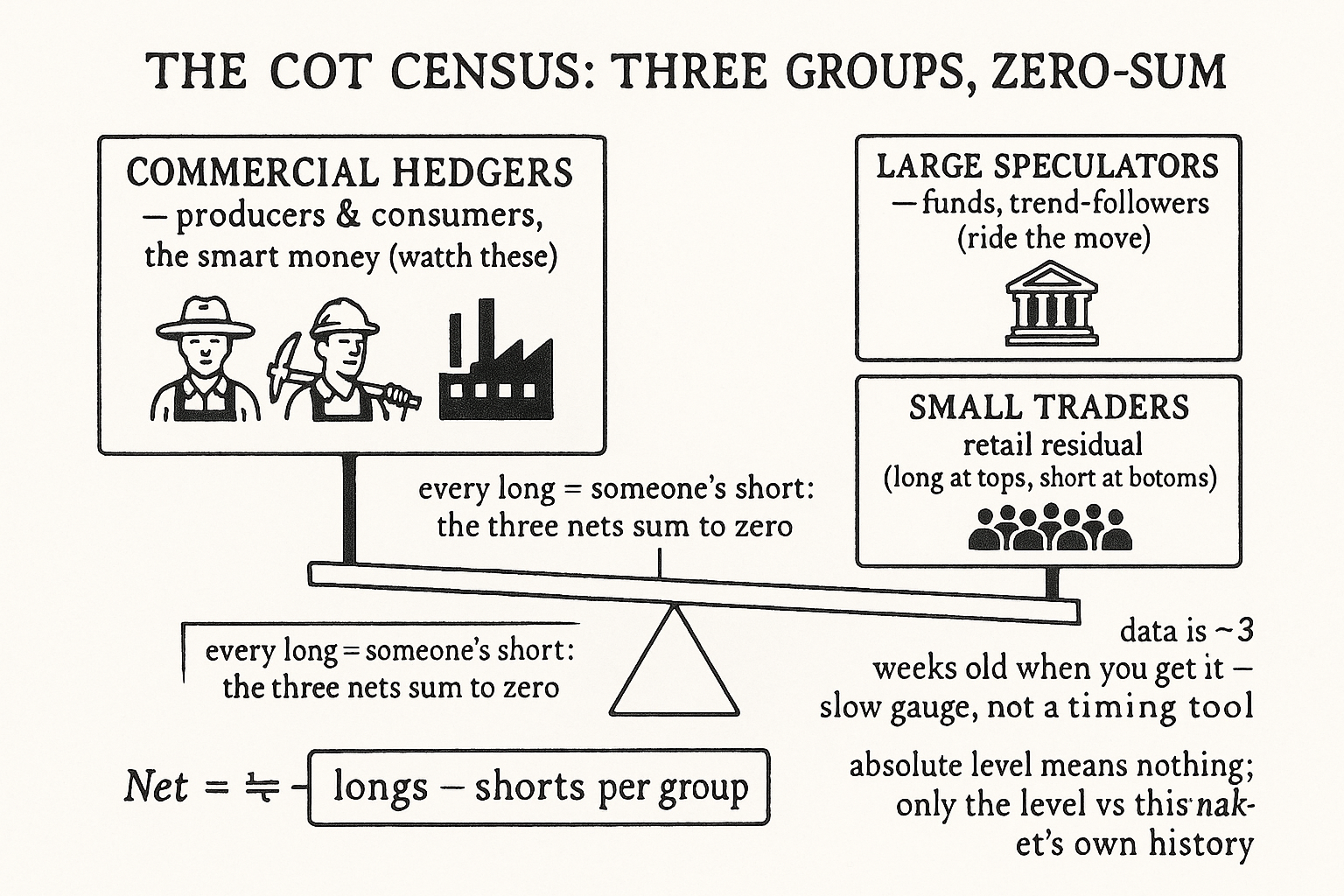

The report sorts every reportable position into three buckets, and the whole value of COT lives in keeping them separate.

Commercial hedgers are the producers and consumers of the physical commodity. The farmer who grows the corn, the cereal company that buys it, the miner who digs the metal, the refiner who processes the crude. They trade futures to hedge a real-world business exposure, not to speculate, and they are the group that knows the physical supply and demand cold because they live in it. This is the smart money, and they are the group you watch.

Large speculators are the non-commercial reportable traders: the funds, the managed-money accounts, the big trend-followers carrying positions large enough to clear the reporting threshold. They are speculating, not hedging, and as a group they tend to be trend-followers, long after a market has risen and short after it has fallen. Useful to track, but they are riding the move, not anticipating it.

Small traders are everyone below the reporting threshold, the non-reportable positions backed out as a residual. This is the retail crowd, and the group's historical reputation is the unflattering one: small traders tend to be heaviest long at tops and heaviest short at bottoms. The connection to the retail-versus-institutional split in "FX Is Not One Market: Retail vs Wholesale Structure" is direct, the small trader here is the futures-market version of the retail flow that gets run over.

$$ \text{Net}_{\text{group}} \;=\; \text{long contracts}_{\text{group}} - \text{short contracts}_{\text{group}} $$ $$ \text{Net}_{\text{commercial}} + \text{Net}_{\text{large spec}} + \text{Net}_{\text{small}} \;=\; 0 $$

For each group, the net position is its long contracts minus its short contracts. The first line is the single number you build everything on. The second line is the constraint that makes COT a closed system: futures are a zero-sum instrument, every long is somebody's short, so the three groups' net positions sum to zero. When commercials are heavily net short, the speculators and small traders must be net long by exactly that amount on the other side. You are never reading one group in isolation; you are reading who is on the opposite side of the smart money.

What the report actually contains

Beyond the headline long and short for each group, the report gives you the number of traders in each group, the number of spread positions, and the net and percent change in the open interest each group holds. The first thing you compute is the net long position per group, longs minus shorts, because the raw long and short totals move with the overall size of the market and the net strips that out.

The catch that traps newcomers: the absolute level of net commercial position is close to meaningless on its own. Commercials in some markets are structurally always net short, because producers always have product to hedge, and in a market like silver the commercials have effectively never been net long in the modern record. So "commercials are net short 40,000 contracts" tells you nothing until you know whether 40,000 is high or low for this market's own history. The signal is the position relative to its own past extremes, not the raw number, which is the differencing-and-normalizing instinct from "How to Build Stationary Indicators from Non-Stationary Prices" and the reason the next article in this arc builds an index instead of trading the level.

The three-week catch

COT is not real-time, and pretending it is will hurt you. Positions are tallied after the market close on Tuesday. Auditing the data takes time, so the report is released later that week, and the practical reality across the publication schedule is that by the time the numbers are in your hands, they can be around three weeks old. You are looking at a photograph of where the big players stood, taken weeks before you got to see it.

That lag is the central design constraint of any COT system, and it cuts two ways. It kills COT as a short-term timing tool outright; you cannot react to a position shift you learn about three weeks late. But it barely dents COT as a slow positioning gauge, because the commercial accumulation it tracks plays out over weeks and months, not days. A signal that itself leads the market by about two weeks, the property "Why Commercials Are Counter-Trend (and Lead by 2 Weeks)" builds on, survives a multi-week reporting lag where a fast signal would be destroyed by it. Match the data's frequency to the strategy's horizon or do not use it.

Why this group of three matters at all comes down to information asymmetry. Commercials have the money and the inside view of physical supply and demand that the public never sees, so their aggregate positioning carries information. The report is valuable because it tells you how the large commercial traders are working, and the rest of this arc turns that into a tradable system: why the commercials lead, how to normalize their position into an index, and the one market family where the whole approach falls apart.

Visualizing the three groups

KEY POINTS

- The Commitment of Traders report is a weekly census of futures positioning: how many contracts each kind of trader is long and short in every major market. It is positional data, not price-derived, so it adds what a chart cannot.

- It sorts positions into three groups that behave differently. Commercial hedgers (producers and consumers) are the smart money with the physical-market view; large speculators are trend-following funds riding the move; small traders are the retail residual, long at tops and short at bottoms.

- Build everything on net position: long contracts minus short contracts per group. Futures are zero-sum, so the three groups' nets sum to zero, you are always reading who sits opposite the smart money.

- The report also gives trader counts, spreads, and changes in open interest, but the net per group is the workhorse number.

- The absolute level of net commercial position is close to meaningless alone. Commercials are structurally net short in many markets (effectively always in silver), so the signal is the position relative to this market's own past extremes, not the raw number.

- COT is roughly three weeks old by publication: tallied Tuesday's close, audited, released later. It is a slow positioning gauge, not a short-term timing tool.

- The lag survives because commercial accumulation plays out over weeks and the signal leads by about two weeks. Match the data frequency to a multi-week horizon or do not use it.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Hedgers, funds, and small speculators in the energy futures markets

- Why Do Hedgers Trade So Much?

- The Role of Hedgers and Speculators in Commodity Futures Markets

- On the predictive role of large futures trades for S&P500 index returns

- Four Commitments of Traders Reports puzzles, revisited

- The effectiveness of position limits: Evidence from the foreign exchange futures markets

- Who Holds Positions in Agricultural Futures Markets?

- The Economic Role of Commodity Futures Markets