6.33 Fat Tails: Why Gaussian Thinking Breaks Trading Systems

The bell curve calls crashes impossible, and they keep happening, because real returns have fat power-law tails. Gaussian models fail in the crisis they exist for. Size for the move you can't model.

The normal distribution is the most useful wrong assumption in finance. It makes the math tractable, it underlies most risk models, and it is false about markets in the one way that matters: it radically underestimates how often extreme moves happen. Real returns have fat tails, the rare giant move occurs far more often than a bell curve allows, and a system built on Gaussian assumptions is calibrated for a world where its worst day cannot happen, right up until that day arrives. "Variance Ratio Tests for Traders" already noted that fat tails distort variance; this is the full problem and why it kills systems that ignore it.

The bell curve says the crash is impossible

The normal distribution has thin tails that decay fast, so the probability of a move many standard deviations from the mean drops to essentially zero. Under a Gaussian, a five-standard-deviation daily move should happen roughly once every several thousand years, and a ten-sigma move never in the history of the universe. Markets produce moves of that magnitude every few years. October 1987, the 2008 cascade, the 2010 flash crash, the 2020 March selloff, each was a move the Gaussian model assigns a probability so small it is indistinguishable from impossible, and they keep happening, which means the model is not slightly off, it is wrong about the part of the distribution that determines survival.

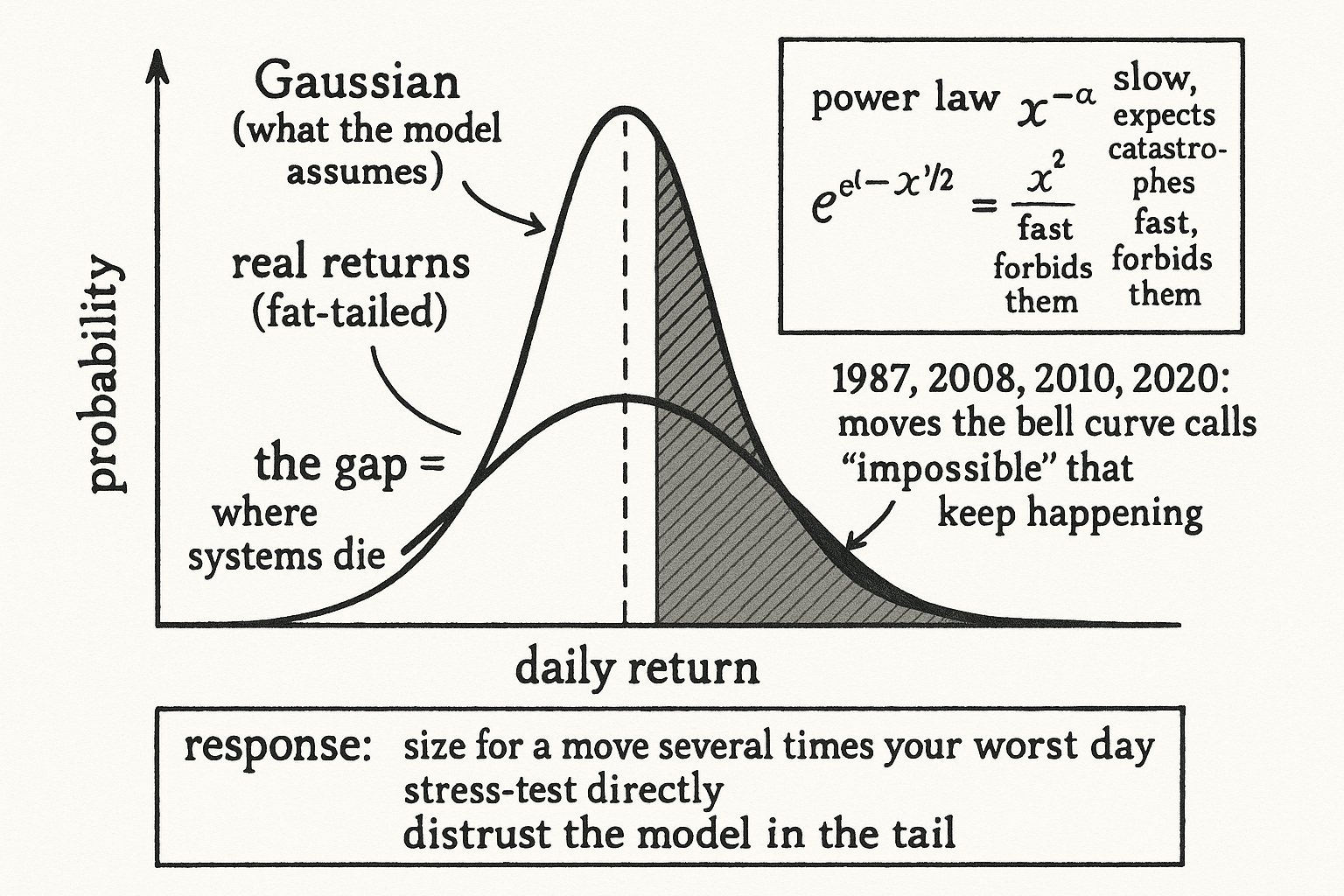

$$ P(|r| > x) \sim x^{-\alpha} \quad \text{(fat tail, power law)} \qquad \text{vs.} \qquad P(|r| > x) \sim e^{-x^2/2} \quad \text{(Gaussian)} $$

The difference is in how the tail decays. A fat-tailed distribution's tail falls off as a power law, a negative power of the move size, which declines slowly, so even far out in the tail there is meaningful probability mass. The Gaussian tail falls off as the exponential of the negative squared move, which declines ferociously fast, crushing the probability of extremes to nothing. The gap between a slow power-law decay and a fast exponential one is the gap between a distribution that expects occasional catastrophes and one that forbids them, and that gap is exactly where trading systems die. Excess kurtosis, the fourth moment running far above the Gaussian value of 3, is the summary statistic that flags this, but the tail behavior is the thing that hurts you.

Why Gaussian risk models fail when it counts

A risk model built on the normal distribution does its job well in calm markets and fails precisely in the crises it exists to protect against. Value-at-risk computed under normality tells you the most you can lose on a normal day, and a normal day is not when you blow up. The model sizes your positions for a world where the worst plausible move is four or five sigma, and then a ten-sigma move arrives and the loss is many times what the model said was possible. The failure is structural, not a calibration error: the model assumed the tail was thin, the tail was fat, and no amount of tuning a thin-tailed model captures a fat tail.

This connects directly to the survival arguments in this pillar. The position sizing from "Why Volatility-Adjusted Position Sizing Matters" scales by volatility, a measure that fat tails make unstable, because a few extreme moves dominate the variance and a calm stretch understates the true risk. The drawdown analysis from "Average Drawdown vs Extreme Drawdown" warned that the worst case lives in the tail the permutation shuffle underweights, and fat tails are why: the real distribution of moves has more extreme events than any thin-tailed model or naive resampling reproduces. Loss control from "Why Loss Control Is the Only Thing You Fully Control" is necessary precisely because the tail can deliver a loss your Gaussian-calibrated stop never contemplated.

Trade as if the tail is real

The practical response is not to find the perfect distribution, because no closed-form distribution captures the tail exactly, and the next article on Lévy distributions shows even the better-fitting ones miss the rarest events. The response is to stop trusting any model in the tail and to build for the move you cannot model. Size positions so that a move several times larger than your worst historical day does not end you, not just so that a normal day is comfortable. Stress-test against extreme scenarios directly, asking what a 20% overnight gap does to the book, rather than reading a probability off a curve that says the gap cannot happen. Treat volatility estimates as understated, because the calm periods that dominate the estimate are exactly when the tail is being underweighted. And accept that the tail is not a rare nuisance to be smoothed away but a permanent feature of markets that determines whether you survive long enough for your edge to matter. The trader who respects the fat tail sizes smaller and lasts; the one who trusts the bell curve sizes for the world the model describes and gets carried out in the world that exists.

Visualizing fat tails

KEY POINTS

- The normal distribution is the most useful wrong assumption in finance. It is tractable and underlies most risk models, and it radically underestimates how often extreme moves happen.

- Real returns have fat tails: the rare giant move occurs far more often than a bell curve allows. Five- and ten-sigma moves that the Gaussian calls essentially impossible happen every few years.

- The difference is tail decay. Fat tails fall off as a slow power law, leaving real probability mass far out, while the Gaussian falls off exponentially, crushing extremes to nothing. Excess kurtosis flags it.

- Gaussian risk models work in calm markets and fail in the crises they exist for. Value-at-risk sizes you for a normal day, and a normal day is not when you blow up. The failure is structural, not a calibration error.

- Fat tails destabilize volatility estimates (a few extremes dominate variance), are why the worst-case drawdown lives in the tail resampling underweights, and are why loss control must cover moves no Gaussian stop contemplated.

- The response is not a perfect distribution but distrusting any model in the tail: size for a move several times your worst day, stress-test extremes directly, treat volatility as understated, and respect the tail as a permanent feature that decides survival.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- AlphaCrafter: A Full-Stack Multi-Agent Framework for Cross ... - arXiv

- Risk Intelligence — Institutional Framework | Page 2

- An Overview of Tail Risk Strategies

- Alpha Decay and Institutional Trading

- FACTOR INVESTING AND ASSET ALLOCATION

- Evaluation of Value-at-Risk (VaR) using the Gaussian Mixture Models

- Tail Risk Dynamics in Price-Limited Stock Market

- Managing Regret Risk: The Role of Asset Allocation

- Central Limits and Financial Risk

- Optimal Portfolio Choice with Fat Tails

- Why does skewness and the fat-tail effect influence value-at-risk estimates?

- Limitations of portfolio diversification through fat tails of the return distributions: Some empirical evidence

- Momentum Has Its Moments

- Assessing Uncertainty in Stock Returns: A Gaussian Mixture ... - arXiv

- [1504.05844] A Study of Correlations in the Stock Market - ar5iv

- Effects of the fat-tail distribution on the relationship between

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.