5.38 Lead-Lag Done Right: Predict and Manage, Don't Naively Wait

The naive lead-lag trade enters B after A moves and exits on a timer. That wastes the edge. Use the slope as a forecast of B's move, exit the instant B hits it, and hold to the horizon only as a backstop.

The textbook lead-lag trade goes like this. Asset A jumps. You believe B follows A with a delay, so you buy B and close after a fixed five seconds. Simple, mechanical, and wrong in a way that quietly bleeds you. The old article "Lead-Lag Relationships in Global Markets" established the relationship itself, one market moving first and a related market following with a measurable delay, and warned that the lead is the most fragile object in intermarket analysis. This piece is about what you do once you have a lead worth trading, and the answer is not "wait five seconds."

The fixed-wait version throws away the two things that actually make the trade work: a number for how far B should move, and a rule for getting out when it does.

Why the fixed-wait trade is broken

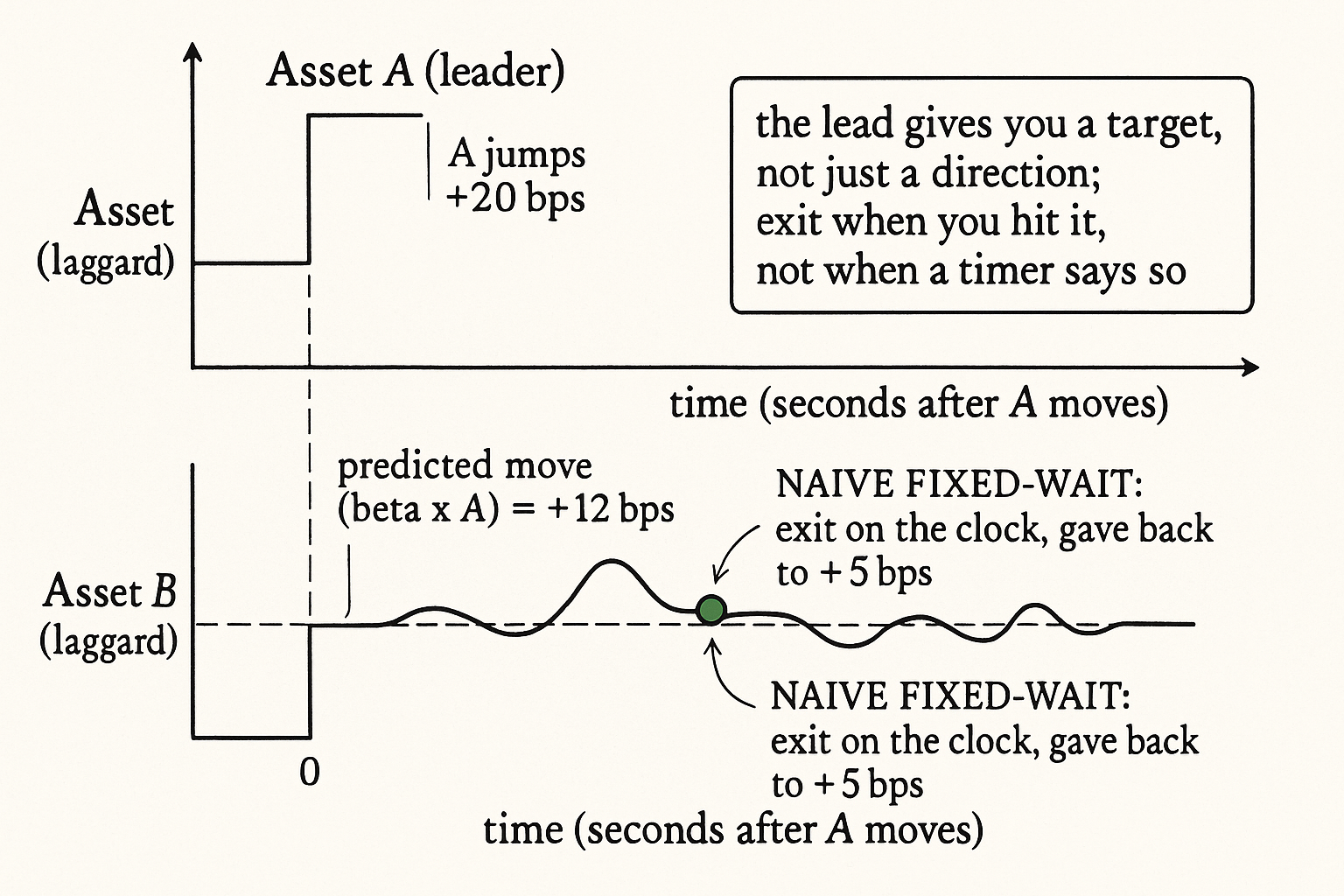

A leads B means the regression of B's future return on A's recent return has a real slope at some lag. The old article "Crypto Cross-Exchange Lead-Lag Study" built exactly this on crypto venues, regressing one exchange's returns against another's at a shifted timeframe to find where the slope peaks. That slope is not just a yes/no signal that B will move. It is a magnitude. It tells you roughly how much B should move given the size of A's jump.

The naive trade ignores the magnitude entirely. It enters B and exits on a clock, which means three bad outcomes get lumped together. B reaches the predicted move in two seconds and then keeps drifting or reverses, and you sit through the give-back until your timer fires. B reaches the move instantly and you hold for three more seconds of pure noise and adverse selection. B never moves at all because this was one of the times the lead failed, and you still hold to the timer hoping. A clock cannot tell these apart. A target can.

Predict the move, then manage the exit

Use the lead the way it was measured: as a forecast of B's move, not a trigger to wait.

$$ \widehat{\Delta B} = \beta \cdot \Delta A_{\text{recent}} $$

Read it plainly: the predicted move in the lagging asset B equals the lead-lag slope beta times A's recent move. Beta is the peak-lag regression coefficient from the old lead-lag study, the number you already estimated to confirm the lead exists. If A jumps 20 basis points and your fitted beta is 0.6, your forecast is a 12 basis point move in B. That 12 bps is the whole trade. It is your target, and it is what turns a vague "B should follow" into a managed position.

Now the management rule, which is the part the naive version skips:

- Enter B in the direction of the forecast as soon as A moves.

- If B reaches the predicted move before your horizon expires, close immediately and take the edge. You got what the lead promised; there is no reason to keep holding into noise.

- If B has not reached the target by the horizon, close anyway, at whatever small profit or loss is there. The lead either misfired or got arbitraged before you, and holding longer is hope, not edge.

The horizon still exists. It is a backstop, not the exit logic. Most of your good exits come from hitting the target early, not from the clock.

Why early exit is the whole point

The edge in a lead-lag trade lives in a narrow time window, the lag you measured, and it decays fast on either side of it. Hold past the moment B catches up to A and you are no longer trading the lead. You are holding naked exposure to B's own noise, paying spread and eating adverse selection with no forecast backing you. The early-exit rule cashes the edge exactly when it exists and refuses to pay for time after it is gone.

A worked sequence makes the asymmetry obvious. Say your measured edge per fired signal is around 12 bps of predicted B-move, your round-trip cost is 4 bps, and B's noise over the holding window is roughly 8 bps one-sigma. Exit the instant B hits 12 bps and you net about 8 bps before the noise has a chance to drag you back. Sit on a fixed timer instead and that 8 bps of noise is now a coin flip layered on top of your realized move, so half your hit-the-target trades give back several basis points before the clock lets you out. Same signal, same entry, worse exit, and the difference is pure management.

The forecast also gates entry size. A big predicted move relative to cost is worth a full clip; a predicted move barely above your round-trip cost is not worth trading at all, no matter how clean the lead looked historically. The fixed-wait trade has no way to express this because it never computes the number.

The traps that still apply

None of this rescues a lead that is not real. The old lead-lag article's three fake-lead mechanisms are all still live here: a shared slow driver hitting both assets with different delays, a real lead that got arbitraged away as venues sped up, and a data-mined lead from scanning too many pairs and lags. A managed exit on a fake lead just loses more efficiently. Re-estimate beta on a rolling window and watch the peak lag migrate toward zero, the same early-decay warning from before, because the day the lag collapses is the day this trade stops paying and starts feeding the faster player on the other side.

The other honest limit is that this is a latency race. The cross-exchange version from the old fair-value work, "Cross-Exchange Fair Value for Crypto Perps," is the same physics: the leader's move is public, and everyone with a colocated box sees it too. Your forecast of B is only tradable in the slice of time between A moving and B catching up, and if that slice is shorter than your reaction time, the predicted move is real and still unreachable. Measure your own latency against the lag before you assume the edge is yours.

Visualizing predict-and-manage vs naive-wait

KEY POINTS

- The naive lead-lag trade (enter B after A moves, exit on a fixed timer) wastes the two things that make the trade work: a magnitude for B's expected move and a rule to exit when it is reached.

- The lead-lag slope you already fit (the old article "Crypto Cross-Exchange Lead-Lag Study") is a forecast, not just a trigger. Predicted B-move equals beta times A's recent move, so a 20 bps A-jump with beta 0.6 forecasts a 12 bps B-move.

- Manage the exit: close as soon as B reaches the predicted move, and close at the horizon otherwise at whatever small profit or loss exists. The horizon is a backstop, not the exit logic.

- Early exit cashes the edge inside the narrow lag window where it exists; holding past B catching up to A is naked exposure to B's noise with no forecast and full costs.

- The forecast also gates size and entry: a predicted move barely above round-trip cost is not worth trading, a fact the fixed-wait version cannot express because it never computes the number.

- The fragility from the old article "Lead-Lag Relationships in Global Markets" is unchanged: shared-driver fakes, arbitraged-away leads, and data-mined leads, plus it is a latency race, so re-estimate beta and check the lag against your own reaction time.

References

- Lead-Lag Relationships and Cross-Correlation in Financial Time Series

- Latency Arbitrage and Lead-Lag Effects Across Exchanges

- Predictive Regression and Exit Rules in High-Frequency Trading

- Information Diffusion and Price Discovery in Fragmented Markets

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Liquidity Provision, Adverse Selection, and Competition

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- The lead–lag relation between the S&P500 spot and futures markets: An intraday-data analysis using a threshold regression model

- A cointegration approach to the lead–lag effect among size-sorted portfolios

- Lead-Lag Relationships in Market Microstructure⋆

- Improving S&P 500 Volatility Forecasting through Regime-Switching

- When AI Trading Agents Compete: Adverse Selection of Meta ... - arXiv

- DeltaLag: Learning Dynamic Lead-Lag Patterns in Financial Markets