5.39 Big Moves in Lead-Lag: Liquidations, Impact, and News

Lead-lag edge lives in the big moves, so quantile-regress on the tail, not the mean. Then label the cause from trade size and the liquidation feed: impact follows clean, liquidations snap back, and scheduled news is a cue to widen quotes, not to trade.

A lead-lag regression fit on all the data is mostly fit on noise. Most bars are small, directionless wiggles where A and B drift around their spreads, and the ordinary least-squares slope spends its variance explaining those. The old article "Lead-Lag Relationships in Global Markets" measured the relationship with a lagged regression and treated every observation equally. On the HFT side, that is the wrong weighting. The money in a follow-the-leader trade is in the big moves, and a model that averages them in with a thousand tiny ones is diluting the only part that pays.

Two fixes, one statistical and one structural. Reweight the regression toward the tail, and classify what caused the big move so you know whether to trade it or hide from it.

Fit the tail, not the middle

The plain lead-lag slope answers "on average, how much does B follow A." The question that matters when A prints a large move is "when A moves big, how much does B follow," and those are not the same number. Average and tail behavior diverge because impact is nonlinear: a 5 bps move in A barely perturbs B's book, a 50 bps move sweeps levels and drags B with it. You want the slope conditioned on the large moves.

Two ways to get it. The blunt one is to filter: keep only the observations where A's move exceeds a size threshold, throw away the small bars, and regress on what remains. You lose sample but you stop fitting the noise. The sharper one is quantile regression, which fits the relationship at a chosen quantile of B's move distribution instead of at the mean.

$$ \min_{\beta}\ \sum_{t}\ \rho_{\tau}\!\left(\Delta B_t - \beta\,\Delta A_{t-k}\right), \qquad \rho_{\tau}(u)=u\,\bigl(\tau - \mathbb{1}[u<0]\bigr) $$

Read it as a tilted version of least squares. Ordinary regression squares the error and so chases the mean; quantile regression weights positive and negative errors unequally by the factor tau, the check function rho, so the fitted line lands at the tau-th quantile of B's move rather than its average. Set tau high, near 0.9, and beta describes how B behaves in its large upper-tail moves, k is the lead lag you already measured, and the slope you get is the one that governs the trades worth taking. The middle of the distribution stops dominating the fit.

The practical payoff is a beta that is honest about size. If the all-data slope is 0.4 but the upper-tail slope is 0.7, then when A prints a big move you should forecast B following harder than the average regression would tell you, and sizing off the average leaves edge on the table on exactly the moves where edge is largest.

Volume flags which moves matter

Before you condition on move size, you need to know a move is real and not a one-print artifact. Volume is the cleanest proxy. A large price move on heavy volume is information being absorbed; the same move on a single thin print is a glitch or a spoof clearing, and it will not propagate to B in any reliable way. Weighting or filtering large moves by the volume that accompanied them keeps the lead-lag signal anchored to moves that actually shifted the book, and it is one of the strongest features to fold into the leading statistic.

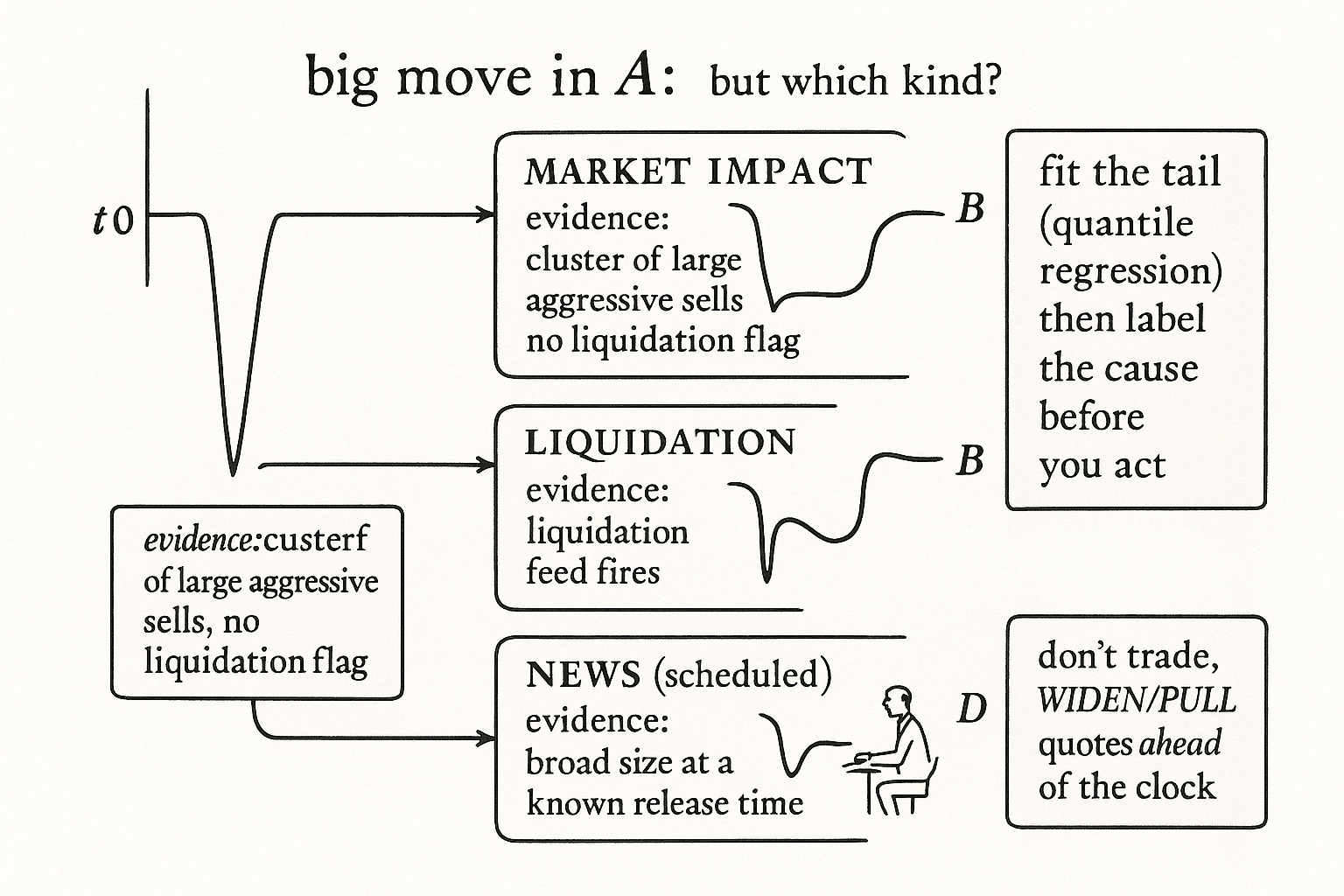

Classify the cause: liquidation, impact, or news

A big move in A is not one thing. It has a cause, and the cause changes whether the lead-lag follow-through is tradable. Three buckets cover most of crypto's large moves, and you can separate them from data you already have.

- Market impact. A large directional trade walks the book. You see it as a cluster of aggressive prints in one direction with large cumulative size and no external trigger. This is the cleanest case for lead-lag: real flow in A, the leader, that genuinely pulls B, the laggard, after it. Trade-size data tells you it happened.

- Liquidations. A forced unwind, visible in the exchange's liquidation feed. These are violent, one-directional, and often mean-revert hard once the cascade exhausts, so the follow-through in B is shorter-lived and the snap-back risk is higher. The liquidation feed is the label; use it to mark these moves and treat their lead-lag signal with a faster exit.

- News. A scheduled or unscheduled headline repriced A on information, not flow. Trade size around a news move looks different, broad participation rather than one whale, and the timing lines up with a known release.

The separator is mechanical. Examine trade size and check the liquidation feed: concentrated aggressive size with no liquidation flag points to impact, a liquidation flag points to forced flow, and a move with broad size at a scheduled time points to news. The old article "Cross-Exchange Fair Value for Crypto Perps" already layered liquidation and flow signals onto fair value across venues; this is the same data feeding a different decision, whether the leader's move is the kind that B will follow cleanly or the kind that will reverse on you.

News is a reason to widen, not to trade

The lead-lag trade is a maker's trade as often as a taker's, and for a maker, scheduled news flips the logic. You do not want to be quoting tight into a release. The old article "Using Trade Flow to Predict Short-Term Price Movement" framed the maker's job as predicting flow; a scheduled news event is the one time you get advance warning that toxic, informed flow is about to arrive on a known timetable.

So the news bucket is not primarily a signal to trade, it is a signal to defend. Ahead of a scheduled release, widen quotes or pull them entirely, because the move that is coming will be fast and informed and your resting orders are the liquidity it picks off. The advantage of news over impact and liquidations is precisely that it is on a clock, so unlike the surprise of a whale or a cascade, you can prepare for it before the first print lands.

The traps, unchanged and sharpened

Conditioning on big moves makes the fragile parts of lead-lag worse, not better. Tail samples are small, so the upper-quantile beta is noisier than the average beta and overfits faster; the old lead-lag article's data-mining warning bites harder when you have already thrown away most of your observations to isolate the tail. Liquidation cascades are the regime where the lead can invert, the laggard leading the snap-back, so a beta fit in calm tails can have the wrong sign in a real cascade. And all of it is still a latency race against players reading the same liquidation feed and the same economic calendar. Re-estimate on a rolling window, keep the size threshold honest, and remember that the cleaner the classification looks in backtest, the more you should suspect you labeled the moves with hindsight.

Visualizing the three causes of a big move

KEY POINTS

- A lead-lag regression on all data fits mostly noise; on the HFT side the edge is in the big moves, so condition the slope on large moves instead of averaging them in.

- Get the tail slope two ways: filter to observations where A's move exceeds a size threshold, or use quantile regression at a high tau to fit B's large-move behavior directly. Average and tail betas differ because impact is nonlinear.

- Volume flags which moves are real. A large move on heavy volume is information absorbed; the same move on a thin print is a glitch, so weight large moves by accompanying volume.

- Classify the cause from data you have: concentrated aggressive trade size means market impact (clean follow-through), a liquidation-feed flag means forced flow (short follow-through, snap-back risk, faster exit), broad size at a scheduled time means news.

- For a maker, scheduled news is a reason to widen or pull quotes, not to trade, because it warns of informed flow on a known clock (the old article "Using Trade Flow to Predict Short-Term Price Movement").

- Tail conditioning sharpens the fragility: small tail samples overfit faster, leads can invert during liquidation cascades, and it remains a latency race, so re-estimate on a rolling window and distrust clean hindsight labels.

References

- Quantile Regression (Koenker and Bassett)

- Liquidation Cascades and Price Impact in Crypto Derivatives

- Market Impact of Large Trades and Order Flow

- Scheduled Macroeconomic News and High-Frequency Liquidity

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Analysis of Limit Order Book and Order Flow

- The Trading Profits of High Frequency Traders

- High-Frequency Trading and Price Informativeness

- Deep order flow imbalance: Extracting alpha at multiple horizons from the limit order book

- The short-term predictability of returns in order book markets: A deep learning perspective

- Measuring Tail Risks at High Frequency

- Measurement of common risks in tails: A panel quantile regression approach for financial institutions

- A high-frequency approach to VaR measures and forecasts based on the HAR-QREG model with jumps