4.39 Day-of-Week Effects That Actually Have a Cause

Five days, two directions, endless mining. The S&P Monday bias decayed, coffee's Thursday is a guess, but silver's Thursday survives because it is really an economic-strength signal in disguise.

Day-of-week effects are where seasonal research goes to embarrass itself. Five trading days, two directions, and a long history give you ten obvious buckets to mine, and you will always find a few that look significant. The Monday effect in stocks got published, traded, written into folklore, and then half of it decayed. So the bar for taking a day-of-week pattern seriously has to be high, and the thing that clears the bar is never the backtest. It is a cause. A day-of-week effect is worth a look only when you can name why that day, in that market, and the why has to be a mechanism, not a story you reverse-engineered after seeing the chart.

This is the cleanest possible test of the principle from "The Difference Between Explanation and Prediction in Markets." A day-of-week bias is the kind of pattern that is trivial to explain after the fact and brutal to predict forward. The ones below survive not because their stats are unbeatable but because the mechanism behind each is concrete enough to say when it should hold and when it should break.

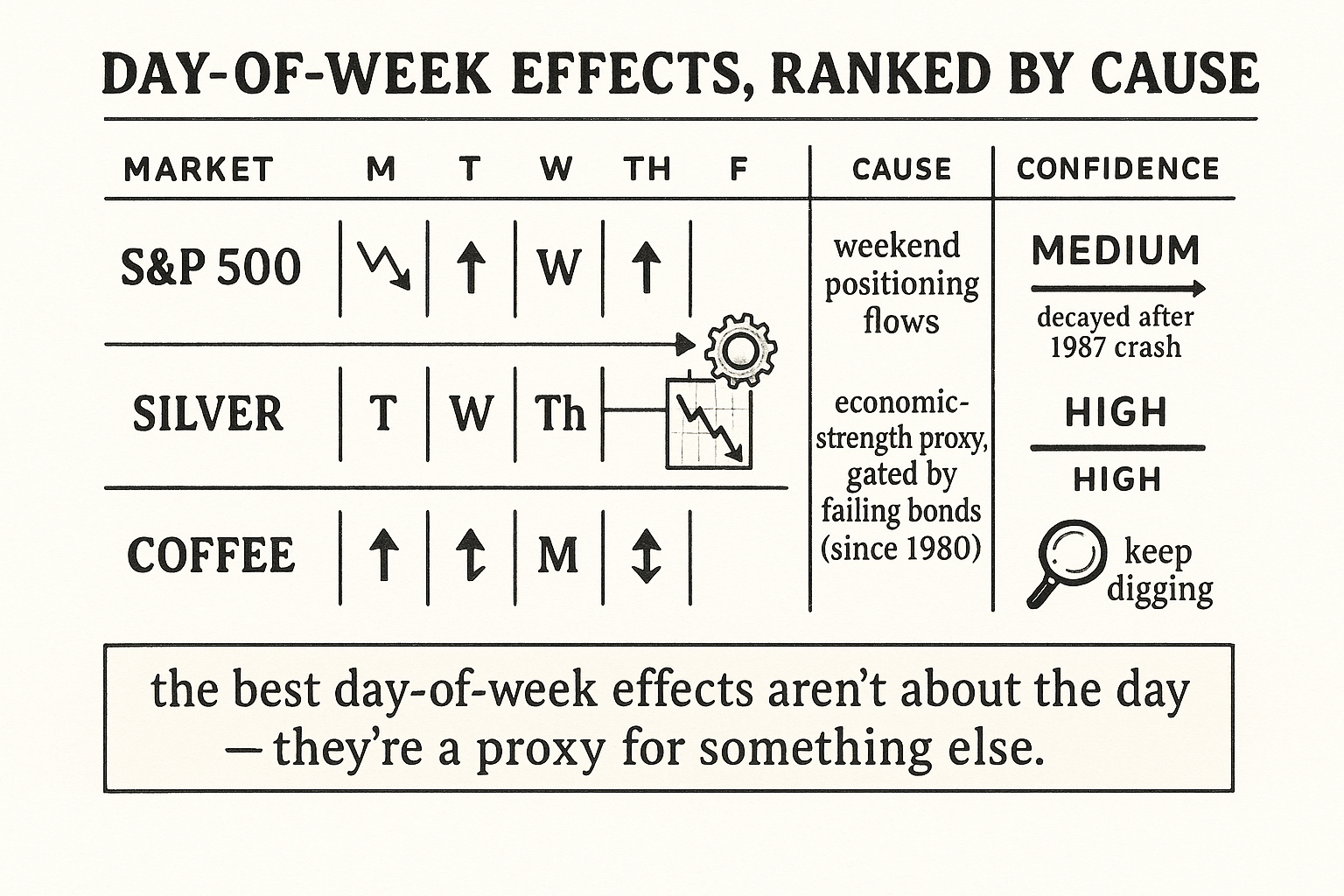

S&P 500: Monday up, Friday down

The flagship behavioral seasonal. Stocks have shown an upward bias on Mondays and a softer tone into Friday, and the standard mechanism is weekend positioning. Traders flatten or lighten risk before the weekend, because two days of headline exposure with no ability to react is a real risk, and they re-establish positions at the start of the week. Selling pressure into Friday, buying pressure on Monday. The flows are the cause; the calendar is just where they land.

The honest part is that this one moved. The Monday effect was magnified after the 1987 crash, "Black Monday," which permanently changed how the market thinks about Monday risk, and the raw edge has weakened since the era when it was first documented. That is the signature of a behavioral seasonal, the fragile engine from "The Three Engines of Seasonality: Fixed-Date, Floating-Date, and Behavioral." A pattern driven by habit gets watched, gets traded against, and shifts. The mechanism is real, which is why some version of the weekend-positioning bias persists in places, but the magnitude is not stable and you cannot trade it as if it were a constant. Treat the S&P day-of-week effect as the cautionary case study, not the moneymaker.

Silver: Thursday up, conditioned on bonds

Silver is the interesting one, because its day-of-week bias is not freestanding. It is conditional, and the condition is what makes it credible. Silver has carried an upward bias on Thursdays, but the better way to read it is through silver's role as an industrial-demand and economic-strength proxy. Silver is half precious metal, half industrial input, so it tends to firm when the economy looks strong. Strong economy also means rising rates and falling bond prices. So the silver bias shows up most on days when T-bonds are falling, and that relationship has held since around 1980.

$$ \text{Silver bias active} \;\Longleftrightarrow\; \big(\text{day} = \text{Thursday}\big)\;\wedge\;\big(\text{T-bonds falling}\big) $$

Read it as a conditional seasonal: the day-of-week tilt is gated by an intermarket state. The Thursday effect alone is a weak, mineable number. The Thursday effect filtered to days when bonds are falling has a mechanism behind it, because falling bonds signal the economic strength that bids silver as an industrial metal. The cause is not "Thursday." The cause is "silver rises with economic strength, and the day-of-week pattern is the visible residue of that." This is the bridge from a behavioral curiosity to an intermarket signal, and it points straight at the approach in "Intermarket Analysis for System Traders": a second market gates the first. A bare day-of-week bias becomes defensible the moment you can attach it to a cross-asset cause.

Coffee: Thursday up, Monday down

Coffee has shown an upward bias on Thursdays and a downward bias on Mondays. The mechanism is murkier than silver's and softer than the S&P's weekend story, which is itself the lesson. Coffee is a thinner, supply-shock-driven market, and weekly patterns there plausibly tie to the rhythm of physical trade, shipping schedules, weekend weather risk in growing regions building into the week, and dealer positioning around it. None of that is as clean as "the earth tilts" or "bonds price economic strength."

So coffee sits in the suspicious tier. The pattern is real in the sample, but the cause is a hand-wave, and a hand-wave fails test four of the reliability checklist in "Is Your Seasonal Real or Curve-Fit? A Reliability Checklist." The right move is not to trade it on faith and not to dismiss it outright. The right move is to keep digging for the actual mechanism, weather risk into the week, a scheduled report, a roll or delivery rhythm, and only graduate it to tradable once the cause is named. Until then it is a flagged candidate, not a signal. Listing it here is the point: most day-of-week effects look like coffee, plausible and unproven, not like silver.

How to handle any day-of-week claim

Three rules, learned from the three cases above.

First, demand the mechanism before the magnitude. The S&P, silver, and coffee differ not in how good their backtests look but in how solid their causes are. Rank by cause strength: silver's intermarket gating is the strongest, the S&P's weekend flows are real but decaying, coffee's is a guess. Trade in that order of confidence, not in order of backtest p-value.

Second, look for the conditioning variable. The silver case shows the upgrade path: a weak standalone day-of-week bias often becomes a real signal once you find the state that gates it. The market does not repeat, it rhymes, the point of "Why the Market Does Not Repeat, But Still Rhymes," and the rhyme in a day-of-week effect is usually some underlying driver that happens to express itself on certain days. Find the driver and you have something more stable than the day.

Third, assume decay on the behavioral ones. Any day-of-week effect that runs on pure trader habit, the S&P Monday bias being the archetype, is competing with everyone else who read the same research. Behavioral edges erode as they spread. Size them small, monitor them, and do not be surprised when they fade or invert, because that is what the engine does.

The deeper takeaway is that the best day-of-week effects stop being about the day. Silver's Thursday bias is really an economic-strength signal that leaks through on Thursdays; the day is the symptom, the intermarket state is the disease. That reframing is exactly what the next article in the arc, "Seasonality as a Filter, Not a Standalone System", is built on: a seasonal earns its keep by combining with the cross-asset signals it is secretly a proxy for, not by standing alone on a calendar.

Visualizing the three cases

KEY POINTS

- Day-of-week effects are trivial to mine: five days, two directions, long history. The bar for taking one seriously is a named mechanism, not a good backtest.

- S&P 500 (Monday up, Friday down): driven by weekend positioning, traders flatten into Friday and re-enter Monday. Real mechanism, but magnified then destabilized by the 1987 crash and decayed since. The cautionary case, not the moneymaker.

- Silver (Thursday up): the strongest case because it is conditional. Silver is an economic-strength proxy, so its bias shows most on days when T-bonds are falling (since ~1980). The cause is economic strength; the day is the residue.

- Coffee (Thursday up, Monday down): real in-sample but the mechanism is a hand-wave. Sits in the suspicious tier; keep digging for the actual cause before trading it.

- Rank day-of-week claims by cause strength, not by p-value: silver (intermarket-gated) over S&P (real but decaying) over coffee (guess).

- Look for the conditioning variable. A weak standalone day-of-week bias often becomes a real signal once you find the state that gates it, as falling bonds gate silver.

- Assume decay on behavioral effects. Pure-habit edges like the Monday bias erode as the research spreads. Size small, monitor, expect fade or inversion.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Behavioral finance impacts on US stock market volatility: an analysis

- Forecast on silver futures linked with structural breaks and day-of

- Foreign Exchange Market Microstructure and the WM/Reuters 4pm Fix

- The effect of the switch to winter time on stock markets - ScienceDirect

- Day-of-the-week effect on stock market returns, volatility, and

- The day-of-the-week-effect on the volatility of commodities

- Order flow composition and trading costs in a dynamic limit order

- Stock market returns and fatal car accidents - ScienceDirect.com