4.48 Why COT Fails in Currencies

The COT index dies on currencies for a structural reason: futures are the whole hedging market in commodities but a rounding error in FX. No amount of tuning fixes an unrepresentative sample.

The COT index works beautifully on corn and silver and dies quietly on the euro, and traders who do not understand why keep trying to trade it there anyway. The failure is not a bad parameter or a weak sample. It is structural. COT measures positioning in the futures market, and the entire edge depends on the futures market being where the smart money actually trades. In currencies, it is not, so the data you are reading is a tiny, unrepresentative corner of the real market, and a contrarian signal built on it is noise wearing the costume of a signal.

The previous articles in this arc built the COT system on a single assumption: the commercial position in futures reflects the genuine hedging activity of the people who know the physical market. That assumption holds in commodities. It collapses in FX, and the reason ties directly back to "FX Is Not One Market: Retail vs Wholesale Structure."

Futures are the whole market in commodities, a sliver in FX

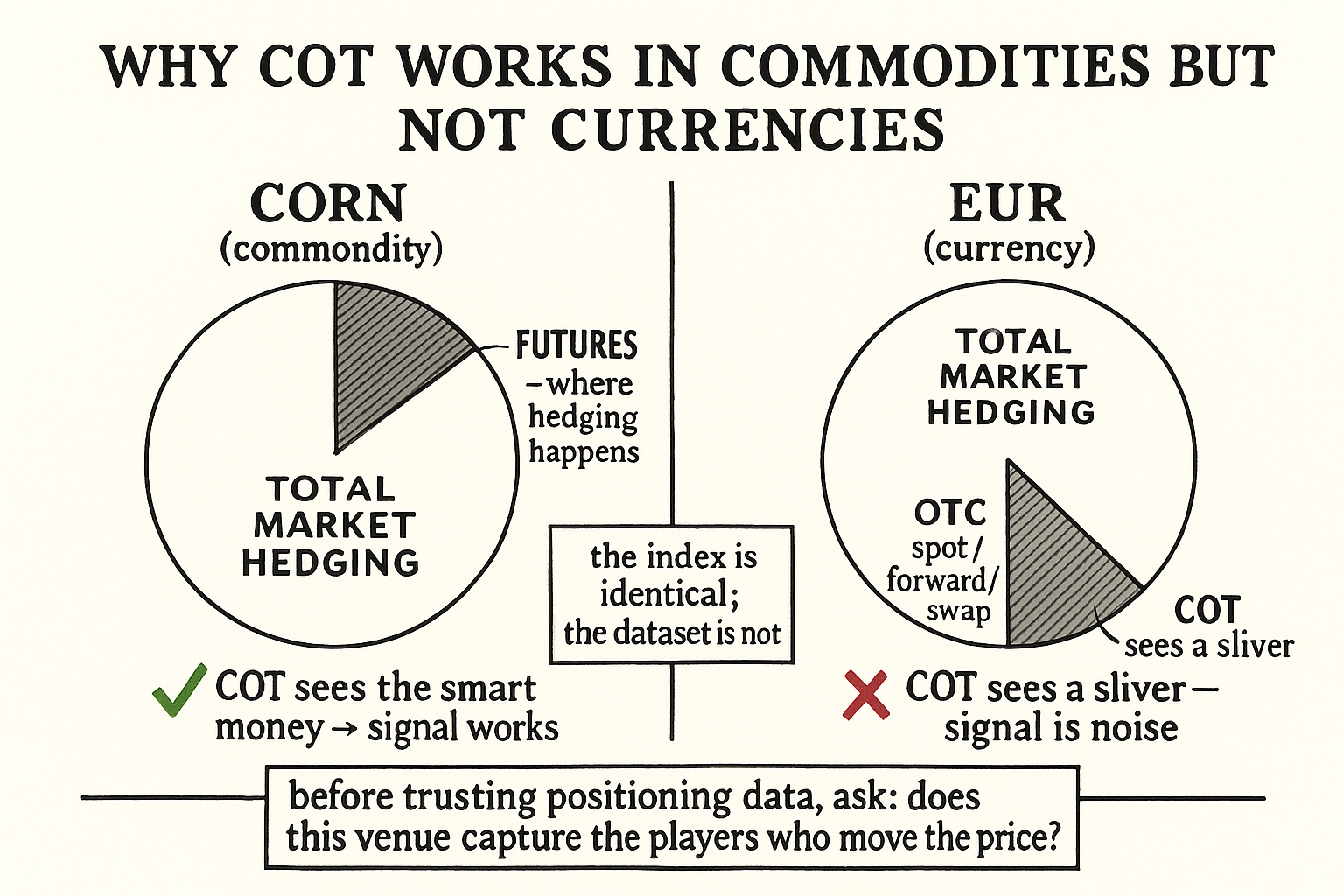

In a physical commodity, the regulated futures exchange is the center of gravity for hedging. A corn producer who wants to lock in a price uses corn futures, because that is where the liquidity and the standardized contracts are. The futures open interest captures a large and representative share of the real hedging, so the commercial net position in the COT report is a faithful read on what the smart money is doing.

Currencies are the opposite. Currency futures exist, but they are a rounding error next to the over-the-counter spot, forward, and swap market where the actual volume lives. The real FX market is the interbank and institutional OTC world described in "The Real Heart of FX Liquidity," and it dwarfs the listed futures by orders of magnitude. The futures represent only a small slice of the total currency market, so the positions reported in COT are not the smart money's book; they are a fraction of it, and not even a random fraction.

$$ \text{COT signal quality} \;\propto\; \frac{\text{hedging captured by futures}}{\text{total hedging in the market}} $$ $$ \text{commodities: ratio} \approx \text{high} \qquad \text{currencies: ratio} \approx \text{tiny} $$

The usefulness of the COT data scales with how much of the market's real hedging actually shows up in futures. In commodities that fraction is high, so the signal is informative. In currencies it is tiny, so the commercial net in FX futures tells you about the positioning of a small, self-selected group of futures users, not about the institutions moving the currency in the OTC market. A clean formula computed on the wrong dataset is still the wrong answer.

Why this is a sample problem, not a tuning problem

The temptation is to assume the FX failure is fixable: try a different lookback, a different threshold, a different currency. It is not, and recognizing why saves you a lot of wasted backtesting. The futures positioning in FX is an unrepresentative sample of the true positioning. No amount of normalizing an unrepresentative sample makes it representative. You can compute a gorgeous COT index on euro futures, and it will have all the statistical polish of the commodity version and none of the predictive content, because the thing it measures is disconnected from the thing that moves the price.

This is the difference between a parameter you can tune and a precondition you cannot. The COT system has one hard precondition: the futures market must capture the smart money. Tune all you want inside markets that meet it. In markets that fail it, tuning is just fitting noise, and a great backtest there is a warning, not a green light, the same "works everywhere is a red flag" instinct that should fire whenever a method posts results in a market where its mechanism cannot hold.

The general rule this teaches

The currency failure generalizes into a check you should run before applying any positioning-based system to a new market: does the dataset you are measuring capture the participants who actually drive the price? COT works in commodities and fails in FX for the same reason a microstructure signal works on a lit exchange and fails when most volume is in dark pools or OTC. If the venue you can see is not where the decisive flow happens, the data from that venue is structurally blind to the thing you care about.

So the practical boundary is clean. Use COT in the physical commodity markets, grains, metals, energy, softs, livestock, where futures are the hedging venue and the commercial position is the real smart-money book. Do not use it in currencies, where the listed futures are a sideshow to the OTC market. The same caution extends to any market where exchange-listed futures are a small fraction of total activity; the commodity-versus-currency split is the clearest case, not the only one.

That closes the Commitment of Traders arc. The report splits the market into hedgers, speculators, and retail; the commercials lead by about two weeks because they trade physical value against the trend; the COT index normalizes their position into a bounded contrarian signal; and the whole apparatus only works where futures are the real market, which means commodities yes, currencies no. A powerful tool with a sharp edge and a clearly marked boundary is worth more than a tool you believe works everywhere, because the second kind is the one that quietly loses your money in the markets where it never could have worked.

Visualizing the structural failure

KEY POINTS

- The COT index works in commodities and fails in currencies for a structural reason, not a tuning reason. COT measures futures positioning, and the edge requires the futures market to be where the smart money actually trades.

- In physical commodities, the regulated futures exchange is the center of gravity for hedging, so the commercial net position is a faithful read on the smart money.

- In currencies, listed futures are a rounding error next to the OTC spot, forward, and swap market. Futures capture only a tiny slice of total FX activity, so the reported positions are an unrepresentative fraction of the real book.

- COT signal quality scales with the fraction of real hedging that shows up in futures: high in commodities, tiny in currencies. A clean formula on the wrong dataset is still the wrong answer.

- This is a sample problem, not a tuning problem. No lookback or threshold fixes an unrepresentative sample, and a polished COT backtest on FX futures is a warning, not a green light.

- The general check before applying any positioning system to a new market: does the dataset capture the participants who actually drive the price? If the visible venue is not where the decisive flow happens, the data is structurally blind.

- Use COT in grains, metals, energy, softs, and livestock; avoid it in currencies and any market where listed futures are a small fraction of total activity.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Flows and Positioning in the Global Currency Market

- Microstructure of Foreign Exchange Markets

- Speculation, Hedging and Intermediation in the Foreign Exchange Market

- Futures trading activity and predictable foreign exchange market returns

- Hedging foreign currency portfolios

- The impact of the listing of options in the foreign exchange market

- What is the impact of introducing a parallel OTC market? Theory and

- FinCoT: Grounding Chain-of-Thought in Expert Financial Reasoning