6.28 Why Discretionary Traders Need Rules Even If They Hate Systems

A discretionary trader without rules expresses skill laced with bias, and the two feel identical inside. Rule-bind sizing, exits, and re-entry, keep discretion for real reads, and test which is which.

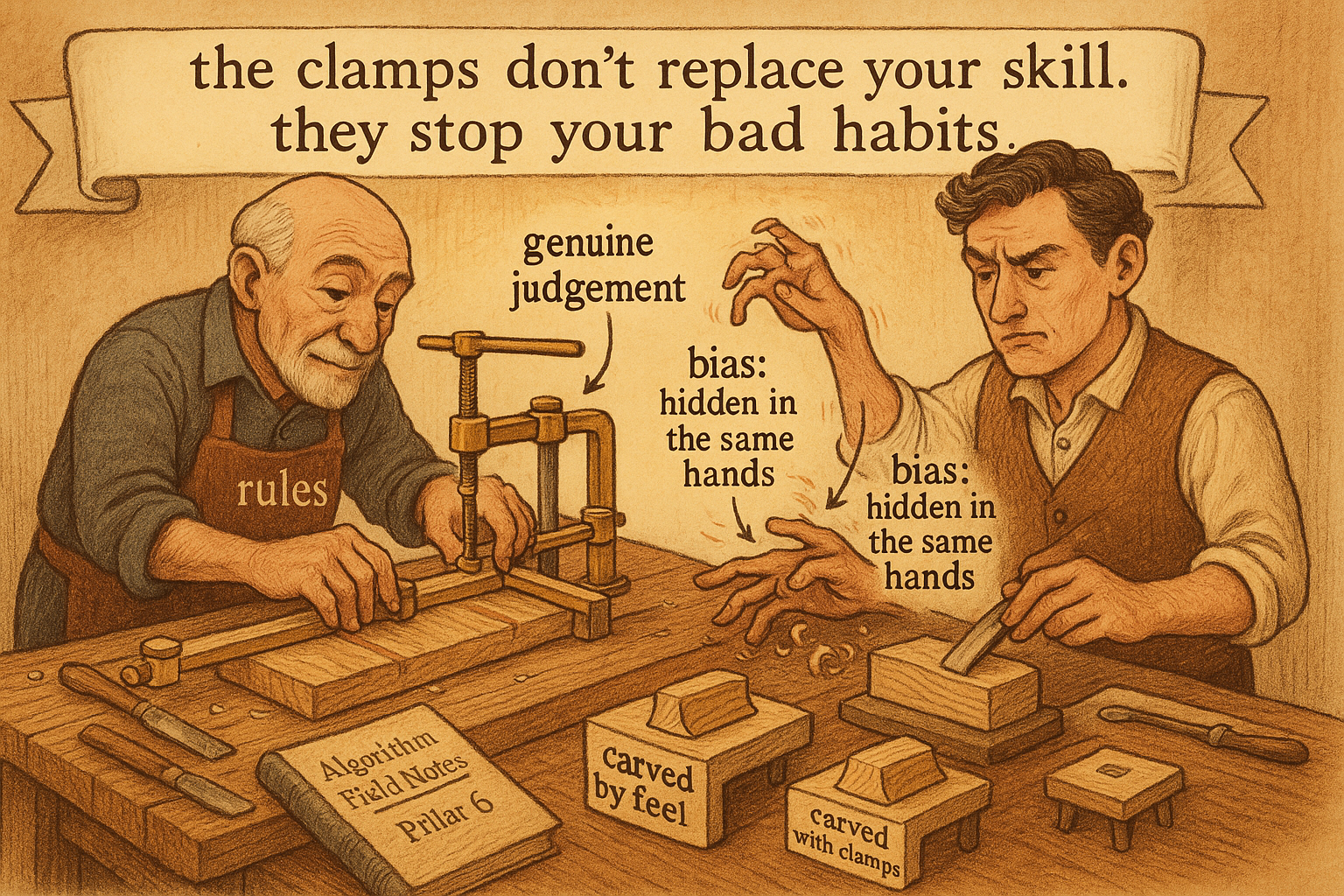

Plenty of skilled discretionary traders recoil at the word systematic. They believe their edge lives in judgment, in reading the market in ways no rule can capture, and handing the decision to an algorithm would throw that edge away. Some of them are right that they have judgment worth keeping. All of them are wrong that judgment means no rules, because the same biases that wreck a novice wreck an expert too, and a discretionary trader without rules is not expressing pure skill, he is expressing skill contaminated by get-even-itis, the disposition effect, and revenge trading. Rules do not replace the discretionary trader's judgment; they fence off the parts of the decision where judgment is known to fail. This article is for the trader who will never fully systematize and still needs the structure.

Judgment and bias arrive together

The discretionary trader's mistake is to treat his judgment as a single thing, all of it valuable, when it is actually a mix of genuine skill and the cognitive flaws from "The Flawed Human Brain in Trading", and the two are tangled together in the moment. His read on which markets are setting up, where the risk is, what the flow is telling him, may be real and hard to replicate. His decision to hold a loser past his plan because he cannot stand crystallizing it is not skill, it is loss aversion, and it feels identical from the inside. Both are his judgment; only one is worth keeping. Without rules, he expresses both, and the bias half quietly drains the edge the skill half generates.

This is why a discretionary trader can have genuine alpha and still lose money. The skill produces good entries and good reads; the unconstrained biases produce bad exits, oversized revenge trades, and held losers, and the second set eats the first. He blames variance or a bad market, when the actual problem is that his process let the biases into the decisions where they do the most damage, the exits and the sizing, while his real skill, the reads, went underexploited.

Rules where bias is worst, freedom where skill is real

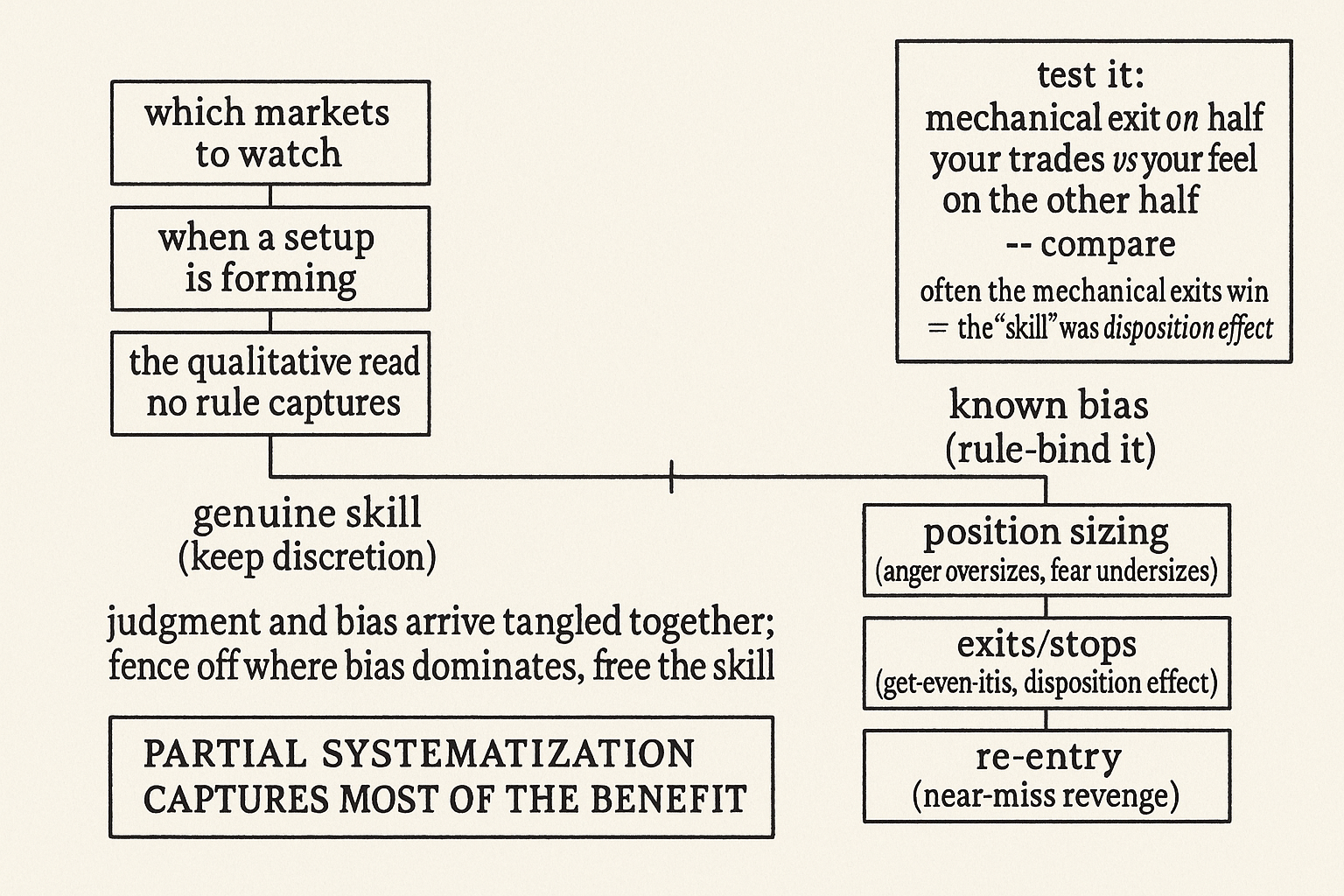

The resolution is not all-or-nothing. The discretionary trader does not have to choose between pure discretion and a fully automated system; he can rule-bind the specific decisions where bias is known to dominate and keep discretion where his skill is genuine. The decisions to systematize are the ones the behavioral articles in this pillar flagged: position sizing, because the urge to oversize after a loss is revenge and the urge to undersize after a win is fear, neither of them skill; exits and stops, because that is where get-even-itis and the disposition effect operate; and re-entry, because that is where the near-miss compulsion drives revenge trades. Hand those to rules. Keep discretion for the part that might be real: which markets to look at, when a setup is forming, the qualitative read that no rule captures.

This hybrid is a partial systematization, and it captures most of the benefit. The trader keeps the judgment that may be his edge and removes his hands from the levers where his judgment is reliably corrupted. A pre-set stop does not insult his market read; it protects the trade his read identified from the exit instinct that would mismanage it. A position-size rule does not override his conviction; it stops his conviction from being inflated by anger or deflated by fear. The rules constrain the failure modes and leave the skill alone, which is the most a trader who refuses full systematization can do, and it is a great deal better than nothing.

The honest part: some of the judgment is not real either

The hard truth the discretionary trader resists is that some of what he calls skill is also bias wearing a costume, and the rules help him find out which. A trader convinced his discretionary exits add value can test it: follow a mechanical exit rule on half his trades and his feel on the other half, and compare. Often the mechanical exits win, which is evidence that the discretion he was defending was the disposition effect all along. Rules are not just a constraint, they are a measurement, a way to separate the judgment that survives a fair test from the judgment that only felt like skill. The discretionary trader who is honest enough to run that test usually ends up rule-binding more of his process than he expected, because more of his judgment than he believed turns out to be bias, and the part that is genuinely skill is happy to be freed from the part that was not.

Visualizing the hybrid

KEY POINTS

- A discretionary trader without rules is not expressing pure skill; he is expressing skill contaminated by get-even-itis, the disposition effect, and revenge trading, which feel identical to skill from the inside.

- Judgment and bias arrive tangled together in the moment. A real read on which markets are setting up is valuable; holding a loser past plan because crystallizing hurts is loss aversion. Both are his judgment, only one is worth keeping.

- This is why a discretionary trader can have genuine alpha and still lose: good reads produce good entries, unconstrained biases produce bad exits and oversized revenge trades, and the second set eats the first.

- The fix is partial, not all-or-nothing. Rule-bind the decisions where bias dominates, position sizing, exits and stops, re-entry, and keep discretion for the qualitative reads where skill might be real.

- A pre-set stop protects the trade the read identified from the exit instinct that would mismanage it; a size rule stops conviction from being inflated by anger or deflated by fear. Rules constrain failure modes and leave skill alone.

- Rules also measure. Test mechanical exits against your feel on split samples; the mechanical version often wins, revealing that the defended discretion was the disposition effect, so honest traders end up rule-binding more than they expected.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Social Transmission Bias and Investor Behavior

- The Impact of Volatility Targeting

- Volatility Scaling in Multi-Asset Portfolios

- A Hybrid Systematic-Discretionary Channel Breakout Framework for Retail Traders

- The Impact of Volatility Targeting

- Do Investor Sophistication and Trading Experience Eliminate

- Applying Behavioral Finance to Investments: The Existence and

- The Impact of Volatility Targeting (Digest summary)

- Behavioral Finance: Theories and Evidence

- Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors

- Overconfidence, Position Size, and the Link to Performance

- On the Performance of Volatility-Managed Portfolios

- A Review on Drawdown Risk Measures and Their Implications for Risk Management and Portfolio Construction

- Trade Sizing Techniques for Drawdown and Tail Risk Control

- Behavioral Biases of Analysts and Investors - NBER

- Conditional volatility targeting strategy considering jump effects

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.