2.35 Frequency-Adaptive EMA: Smoothing That Reacts to Noise

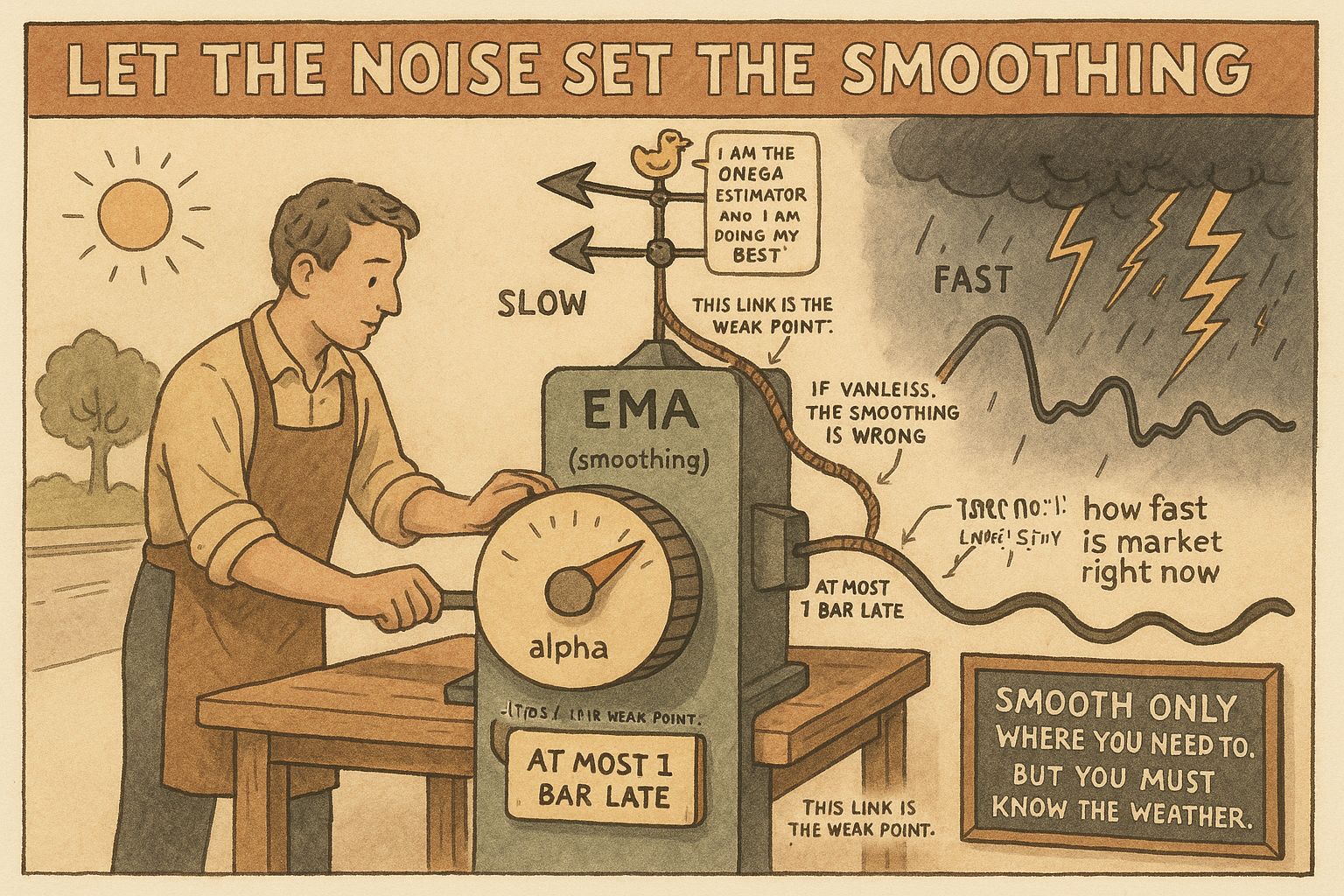

A fixed EMA smooths the same in calm and chaos. The adaptive EMA ties alpha to cycle speed: track tight when clean, smooth hard when noisy, at most one bar lag, if you can estimate omega.

The old article "EMA vs SMA: Why Simplicity Still Matters" left the EMA's smoothing fixed: you pick alpha once, and the filter smooths the same amount whether the market is calm or thrashing. That is the wrong behavior. When the data is quiet you want a light touch that tracks closely; when the data is noisy you want heavy smoothing to reject the thrash. The old article "Automatic Gain Control for Trading Indicators" made an indicator's output adapt to changing amplitude. This makes the smoothing itself adapt, by letting alpha depend on the cycle content of the data: smooth hard when the signal is fast and noisy, smooth lightly when it is slow and clean, and pay at most one bar of lag for it.

Make alpha a function of cycle speed

The standard EMA fixes alpha through the length M, and a fixed M means fixed smoothing forever.

$$ y[n] = \alpha\, x[n] + (1-\alpha)\, y[n-1], \qquad \alpha = \frac{2}{M+1} $$

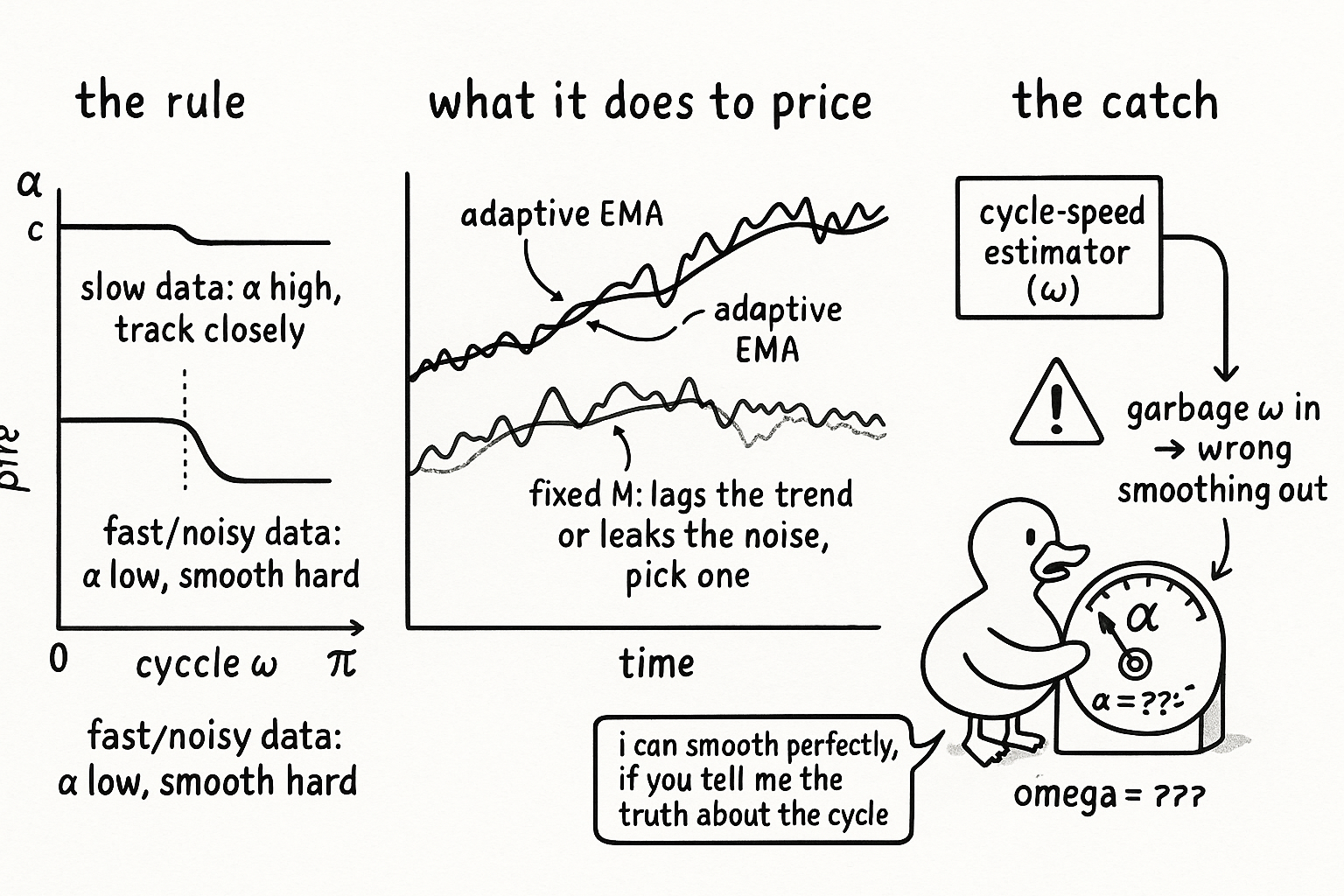

The adaptive version turns alpha into a variable that depends on the cycle speed omega present in the data. The rule is a clamp with a ramp: alpha stays at a high ceiling c, below 1, while the cycle speed is at or below a threshold omega-zero, then ramps down as the speed climbs toward the fast end at pi.

$$ \alpha = \begin{cases} c, & \omega \le \omega_0 \\[4pt] \dfrac{a\,\omega + b}{\omega_0}, & \omega_0 < \omega \le \pi \end{cases} $$

Read what the clamp does in plain terms. When the data is slow, omega small, alpha sits at its high ceiling, the filter leans on the new bar and tracks closely with little smoothing. When the data is fast, omega large, alpha shrinks, which is the same as a large M, so the filter smooths hard. The logic is exactly backwards from a fixed EMA's helplessness: the noisier the data, the larger the effective M, the more it gets smoothed. A fixed EMA cannot do this because its alpha has no idea what the market is doing.

The payoff: heavy smoothing without the usual lag bill

A fixed EMA forces an ugly choice. Set M large and you smooth noise well but lag badly in calm trends; set M small and you track calm trends well but let noise through when the market thrashes. You cannot have both with one alpha. The adaptive EMA escapes the choice by spending smoothing only where it is needed. In the slow, clean stretches it keeps alpha high and tracks tight; in the fast, noisy stretches it drops alpha and smooths hard. Don Mak's measurement on this construction is the headline: the adaptive EMA carries a lag of at most one bar, better than the fixed original at comparable smoothing. You get the noise rejection of a long EMA in the regions that need it without dragging that long-EMA lag through the regions that do not.

This is the same instinct as the old AGC article, applied to a different knob. AGC adapts the output amplitude so a fixed threshold keeps working across regimes; the adaptive EMA adapts the smoothing strength so a fixed filter keeps working across regimes. Both replace a constant that was secretly a regime bet with a quantity that tracks the regime. Both are one extra stage that makes the rest of the pipeline regime-independent.

The catch: omega has to be estimated, and badly estimated omega poisons it

The whole scheme rests on knowing the cycle speed omega, and omega is not handed to you. You have to estimate it from the data, in real time, before you can set alpha. Don Mak is blunt that this is the weak point: the adaptive EMA's one-bar-lag advantage holds only when omega is estimated accurately, and a bad estimate feeds the wrong alpha, which smooths the wrong amount at the wrong time. Estimate omega too fast and the filter under-smooths a noisy patch; estimate it too slow and it over-smooths a clean trend and reintroduces the lag you were trying to avoid.

This is where the cost moved, not vanished. The fixed EMA's problem was a frankly wrong constant. The adaptive EMA's problem is the accuracy and lag of the cycle-speed estimator sitting upstream of it. Dominant-cycle estimation is its own hard problem, and any lag or error in that estimate flows straight into the smoothing decision. The honest reading: the adaptive EMA is a real improvement when you have a trustworthy cycle-speed estimate, and it is a liability when you do not, because it will confidently smooth by the wrong amount. Before deploying one, prove that your omega estimator is good enough on your instrument, because the filter is only as good as the speed it is told.

KEY POINTS

- A fixed EMA smooths the same amount in calm and chaos, because alpha is set once through M. That is a regime bet baked into a constant, the limitation left open by the old article "EMA vs SMA: Why Simplicity Still Matters".

- The adaptive EMA makes alpha a function of the cycle speed omega: a high ceiling c when omega is small (slow, clean data, track closely) ramping down as omega rises (fast, noisy data, smooth hard).

- The behavior is the right way round: the noisier the data, the smaller alpha, the larger the effective M, the heavier the smoothing, automatically.

- It escapes the fixed EMA's forced tradeoff between tracking calm trends and rejecting noisy thrash, spending smoothing only where needed, with a lag of at most one bar per Don Mak.

- It is the same move as the old article "Automatic Gain Control for Trading Indicators": replace a regime-blind constant with a quantity that tracks the regime, as one extra pipeline stage.

- The whole scheme depends on estimating omega accurately in real time. A bad cycle-speed estimate feeds the wrong alpha and smooths by the wrong amount, so prove your omega estimator before trusting the filter.

References

- Statistically Sound Indicators for Financial Market Prediction - Timothy Masters (Amazon)

- Cycle Analytics for Traders - John Ehlers (Amazon)

- MESA Software Technical Papers: adaptive filters and removing moving average lag (John Ehlers)

- Trend Without Hiccups: adaptive and Nyquist-criterion moving averages reviewed (arXiv)

- The Scientist and Engineer's Guide to Digital Signal Processing: Recursive Filters