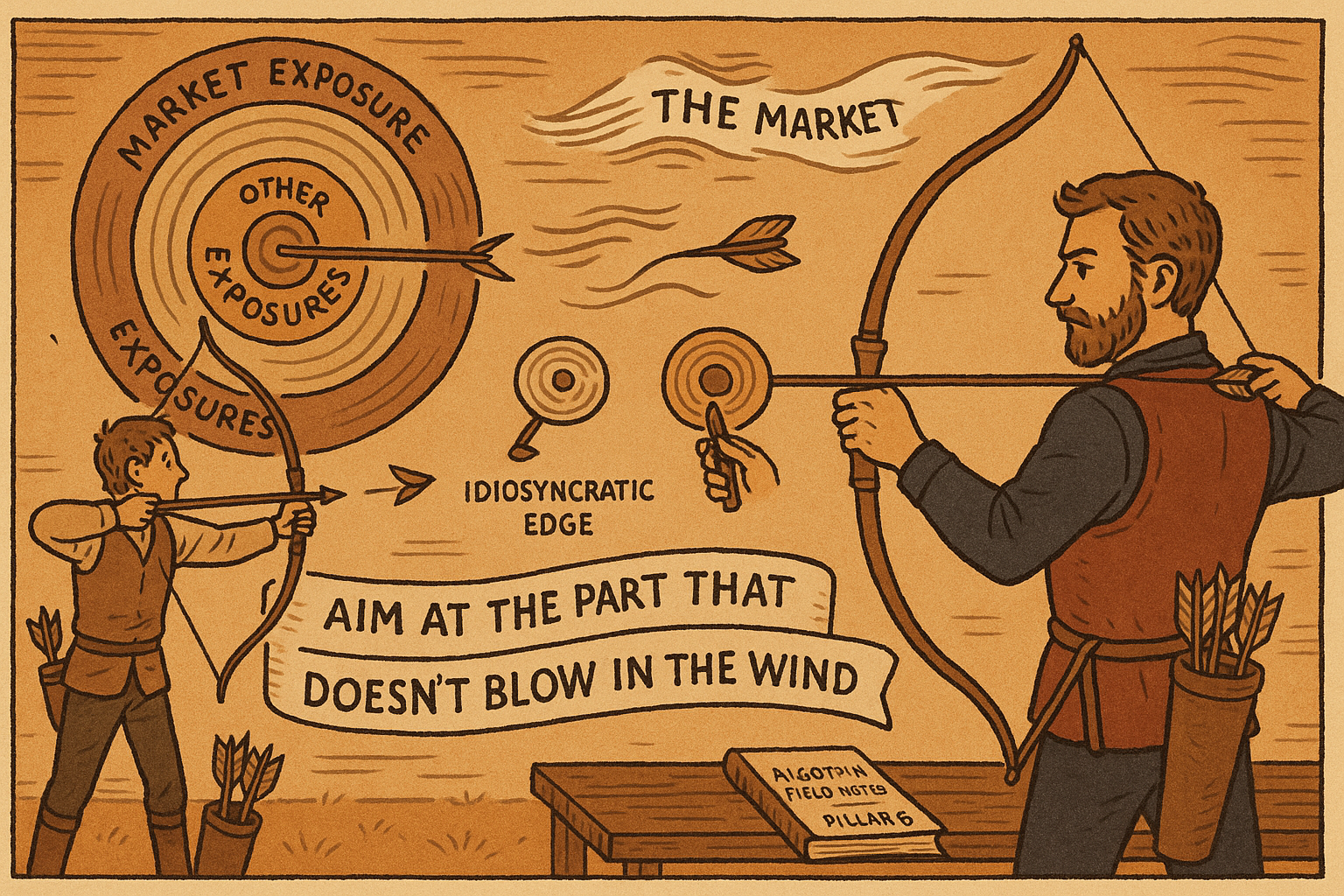

6.44 Predict Residual Returns, Not Gross

Predicting gross return secretly bundles a market-timing bet you're bad at. Strip out beta times the market and other exposures, forecast only the idiosyncratic residual, and the job gets honest.

Most people point their model at the wrong target and never notice. They take a predictor, build a forecast of where the price goes next, and call the gross return the thing to predict. The gross return is the worst possible target, because it secretly bundles a bet you did not mean to make and are bad at: timing the market. Forecast the residual instead, the part of the return that is the instrument being itself, and the job gets easier and more honest in the same move.

Decompose the return before you forecast it

An instrument's gross return is not one thing. It is a sum of pieces, and most of those pieces have nothing to do with the edge you think you have.

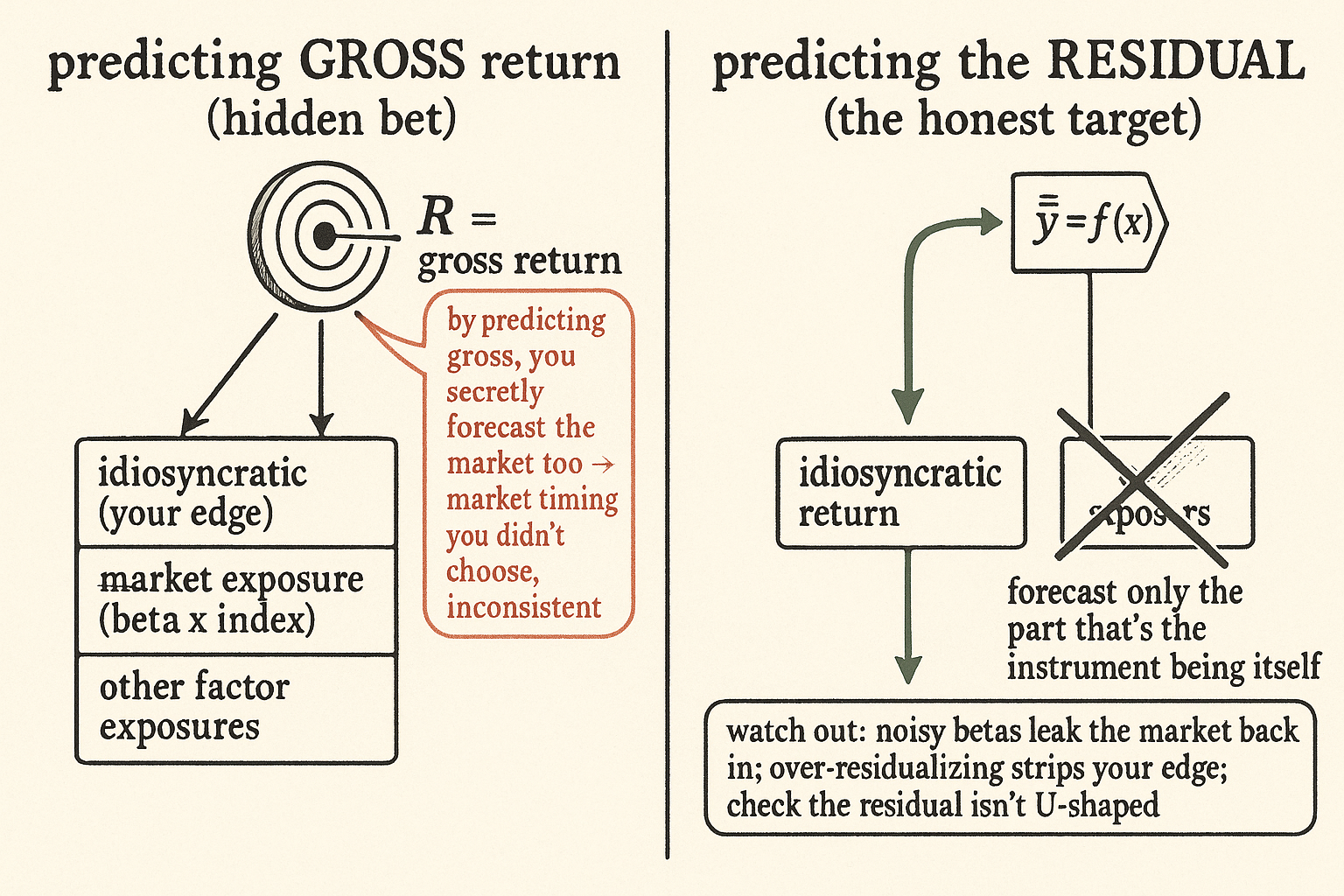

$$ R = R^{\text{idio}} + R^{\text{market}} + R^{\text{other exposures}} $$

The gross return R splits into the idiosyncratic part, the part driven by market exposure, and the part driven by other exposures like sector, size, or whatever factors your instrument loads on. The idiosyncratic piece is the instrument doing its own thing. The market piece is the instrument getting dragged along by the index through its beta. The other-exposures piece is the same drag from every other common factor. When you build a model of gross R, you are building a model of all three at once whether you wanted to or not.

This is the same decomposition behind the factor work in "What Is a Factor, Really," seen from the forecasting side instead of the attribution side. There the point was that a factor is an effect you keep re-finding and should subtract from returns. Here the point is what you should do with the leftover: forecast it, and only it.

Predicting gross secretly forecasts the market

Here is the trap, stated as arithmetic. If your forecast targets gross R, then your forecast is implicitly a forecast of every component.

$$ \hat{y}_{\text{gross}} = \hat{y}^{\text{idio}} + \beta \, \hat{y}^{\text{market}} + \hat{y}^{\text{other}} $$

To predict gross return well, you now need to predict the market return too, scaled by beta, because that term sits inside your target. You have signed up for market timing without deciding to. Most desks have no consistent edge timing the index, and the ones that think they do usually have a few good years and a blowup, because market direction is dominated by macro regime shifts that are hard to call and brutal when you are wrong. Active managers fold this in by accident constantly: a stock-selection model that looks like it picks winners is often half a long-the-market bet riding a bull run, and it falls apart the moment the index stops cooperating.

Forecasting residual returns is the consistent job. Forecasting the market is the inconsistent one. Bundle them and you contaminate the part you are good at with the part you are not, and your live performance inherits the volatility and inconsistency of the market-timing bet you never meant to place.

Strip the exposures, forecast what is left

The repair is to subtract the exposures before forecasting and point the model at the residual.

$$ R^{\text{idio}} = R - \beta \, R^{\text{market}} - R^{\text{other exposures}}, \qquad \hat{y} = f\!\left(x\right) \approx R^{\text{idio}} $$

Estimate the betas, remove beta times the market return and the contributions of the other factor exposures, and what remains is the idiosyncratic return. Train the model to predict that. The forecast no longer carries a hidden market call, so its success or failure is about the edge you actually have, and its return stream stops swinging with the index for reasons unrelated to your signal.

This is the same instinct that powers using one asset to clean another, the move in "Using Bonds to Filter Equity Signals": you remove a known common driver so the equity signal you keep is the part bonds did not already explain. Residualizing generalizes it. Pick the exposures you do not have an edge on, subtract them, and forecast the remainder. Your model gets a cleaner target, your backtest stops rewarding you for accidental market beta, and the thing you ship predicts what you meant to predict.

A caution on the residual itself

Subtracting exposures is not free, and the residual can mislead in its own way. The betas are estimated, so a noisy or unstable beta leaves market return leaking into your "idiosyncratic" target, and you are back to partial market timing without knowing it. Over-residualizing is the opposite failure: regress out so many factors that you strip the genuine edge along with the noise and forecast a flat, dead series. And the relationship between your residual predictor and residual return need not be monotone, the trap "When an Alpha Metric Is U-Shaped" warns about, so check the shape of the residual signal before trusting a linear forecast of it. Residualizing fixes the target. It does not exempt you from validating everything you would validate on a raw signal.

Visualizing the residual target

KEY POINTS

- Gross return is the wrong forecast target. It splits into idiosyncratic return plus market exposure plus other factor exposures, and a model of gross R models all three at once.

- Predicting gross secretly forecasts the market, scaled by beta, because that term sits inside the target. You sign up for market timing, which is hard and inconsistent, without deciding to.

- Active managers fold this in by accident: a stock-selection model is often half a long-the-market bet that works in a bull run and falls apart when the index stops cooperating.

- The fix is to estimate the exposures, subtract beta times the market return and the other factor contributions, and forecast only the idiosyncratic residual that remains.

- This generalizes filtering one asset with another. Pick the exposures you have no edge on, strip them, forecast the remainder, and your backtest stops rewarding accidental market beta.

- Residualizing fixes the target but not the validation. Noisy betas leak the market back in, over-residualizing strips the real edge, and the residual signal can be U-shaped, so check it like any other.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Predicting Relative Returns

- Residual momentum and the cross-section of stock returns: Chinese evidence

- Efficient Replication of Factor Returns

- Factor Models (Chapter II.1 of Active Portfolio Management / factor-model text)

- On Portfolio Optimization

- Volatility-Managed Portfolios

- Predicting Returns with Text Data

- Portfolio Structuring and the Value of Forecasting