5.31 Limit Order Book Behavior: Negative Spreads, Wipeouts, and Why Size Tightens the Market

Crypto books break the textbook: negative spreads are data artifacts, blowouts are wipeouts from large orders clearing levels, and more resting size means a tighter spread because deep books are competitive books.

The bid-ask spread is the first thing you read off a book and the most abused. Most people treat it as a clean number that goes up when things get scary and down when they calm, then build features on top of that cartoon. Crypto books do three things that break the cartoon: the spread sometimes goes negative, it blows out when a single large order eats through levels, and it gets tighter, not wider, when there is more size resting. Each one tells you something about the matching engine and the participants underneath, and a maker who does not account for them quotes against a fiction.

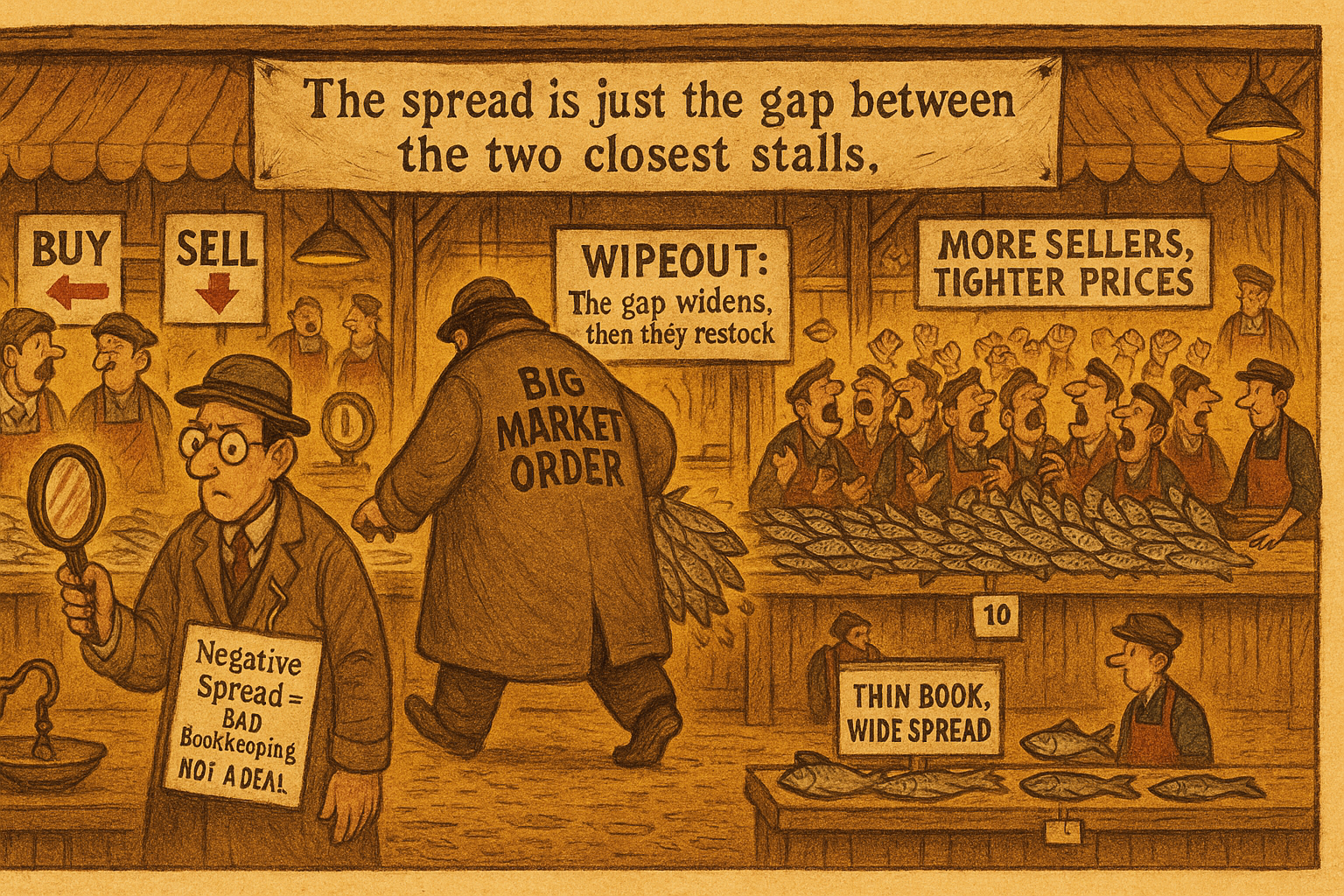

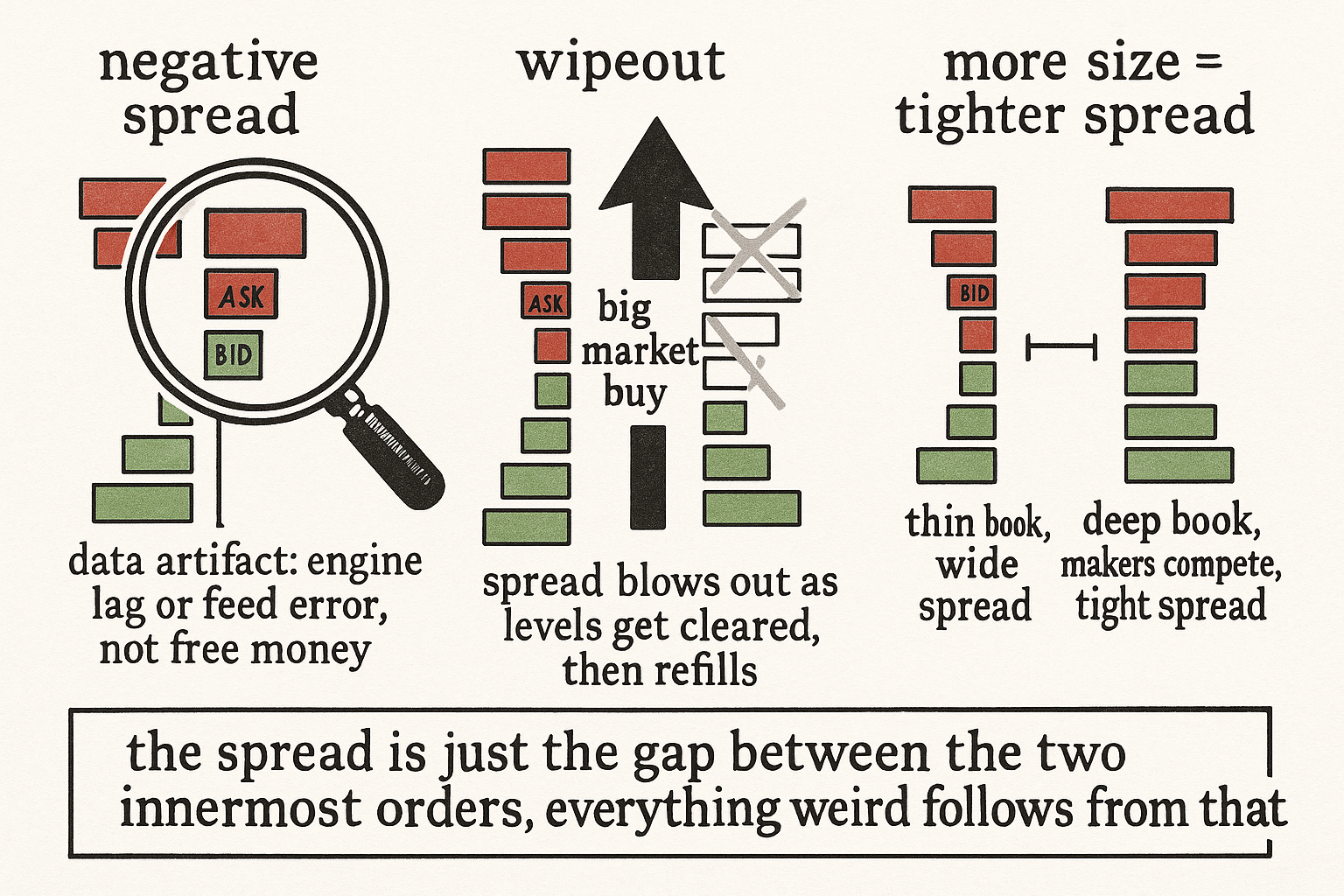

Start with the definition, because the quirks all come from it. The best bid is the first order you hit on the buy side, the best ask the first on the sell side, and the spread is the gap between them. That is all it is, the distance between the two innermost resting orders. Every odd behavior below is what happens when that distance does something a textbook says it cannot.

Negative spreads: the engine is behind

A negative spread means the best bid is higher than the best ask, someone is willing to buy at a price above where someone else is willing to sell. In a sane market that cannot persist for a microsecond, because those two orders should cross and trade instantly. Yet crypto L2 data shows negative spreads, and you have to know why before you let one into a feature.

Two causes. The first is matching-engine lag: the engine has not caught up to the book yet. The crossing orders exist in the data you received, but the engine has not processed the match that will annihilate them, so for a brief window your snapshot shows a state that is about to be resolved. The second is plain data error, dropped messages, out-of-order deltas, a feed that reconstructed the book wrong. Either way a negative spread in your data is not an arbitrage waiting for you. It is a measurement artifact, and a model that ingests it as a real price relationship will generate phantom signals. Filter negative spreads out or flag them; do not feed them to a fair-value model as if the book were genuinely crossed in your favor.

Wipeouts: where the spread blowout comes from

The second behavior is the spread suddenly widening, and the cause is mechanical. A large market order does not stop at the best level. It eats the first level, then the next, then the next, walking up the book until its size is exhausted. After it clears several levels, the new best ask is wherever the order ran out, far from where it started, and the spread is now wide because the inner levels are gone.

This is the same level-walking that drives the square-root market impact law, and it is the dynamic behind the "disappearance of size is a price-moving event" point from the old article "Spoofing, Sturdy Liquidity, and Book Pressure." A wipeout is not the market deciding to be volatile in the abstract. It is one participant removing the resting liquidity that was holding the spread tight, and the widened spread is the crater left behind. For a maker this matters in two directions: your own quotes inside that range get filled as the order walks through you, and the post-wipeout wide spread is a transient, the book refills, so reading the blown-out spread as the new normal and quoting that wide leaves money on the table while liquidity comes back.

Why more size means a tighter spread

The third behavior is the counterintuitive one: the more size in the book, the smaller the spread. Naively you might think a big book and a wide spread go together, lots of size means lots of caution. The opposite holds, and it falls out of competition between makers.

$$ \text{size resting} \uparrow \;\Longrightarrow\; \text{spread} \downarrow $$

When many makers want to provide liquidity on a name, they queue up, and the way you get to the front of the queue is to quote a better price, a higher bid or a lower ask, than the maker beside you. That competition compresses the gap between best bid and best ask. A deep book is a crowded book, and a crowded book is a competitive one, so the spread tightens. A thin book is the reverse: few makers, no one undercutting anyone, so the lone maker present charges a wide spread because nothing forces them tighter. The old article "How to Use Order Book Density for Better Limit Orders" treated density as a landscape of walls and gaps that changes fill speed and toxicity; this is the price-level consequence of that density, dense means tight, thin means wide.

This also tells you which markets to make. Liquid, deep books offer thin spreads but fierce competition for the queue; thin books offer fat spreads but you carry the inventory alone with no one to share the flow, which is exactly the volatility-liquidity tradeoff a maker has to price.

A worked number

Take an alt at the best bid 100.00 and best ask 100.10, a 10 bps spread, with about 5 BTC resting in the top few levels each side. A market buy of 8 BTC arrives. It clears the 100.10 level, the 100.13 level, the 100.17 level, and stops at 100.22 where its size runs out. The new best ask is 100.22, the bid is still 100.00, and the spread just went from 10 bps to 22 bps on a single order, a wipeout, not a volatility regime change. Seconds later, makers seeing the gap and the now-attractive wide spread repost inside it, size rebuilds toward its old 5 BTC, and the spread compresses back toward 10 bps as the queue refills and competition resumes. A feature that logged the 22 bps reading as the prevailing spread, instead of as a transient wipeout that more size will heal, mis-prices the next several quotes.

Visualizing the three behaviors

KEY POINTS

- The spread is only the gap between the two innermost resting orders, the best bid and best ask. Every odd behavior comes from that definition, not from some separate volatility dial.

- Negative spreads in crypto data are artifacts, either the matching engine has not processed the crossing orders yet, or the feed is wrong. Filter or flag them; do not feed a "crossed in my favor" book to a fair-value model.

- Spread blowouts come from wipeouts: a large market order walks up through multiple levels, and the widened spread is the crater of removed liquidity, not a regime change. It is transient and refills, so do not quote the blown-out width as the new normal.

- More resting size means a tighter spread, because a deep book is a crowded book and makers compete for the queue by undercutting each other. A thin book is wide because no one forces the lone maker tighter.

- Worked size: an 8 BTC buy clearing three levels can push a 10 bps spread to 22 bps on one order, then compress back toward 10 bps as makers repost; a feature that logs 22 bps as prevailing mis-prices the next quotes.

- Read deep-tight versus thin-wide as the volatility-liquidity tradeoff: liquid books pay thin spreads with queue competition, thin books pay fat spreads but you hold the inventory alone.

References

- Trades, Quotes and Prices: Financial Markets Under the Microscope (Bouchaud, Bonart, Donier, Gould)

- The Price Impact of Order Book Events (Cont, Kukanov, Stoikov)

- Spread, Depth, and the Determinants of Bid-Ask Spreads in Limit Order Markets

- Crossed Quotes and Stale Data in Cryptocurrency Order Books

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Limit order books

- Analysis of Limit Order Book and Order Flow

- Trading Costs on a Limit Order Book Market: Evidence from the Paris Bourse

- On the (Market Microstructure) Origins of the Return Distribution

- High-Frequency Market Making: Liquidity Provision, Adverse Selection, and Competition

- Limit Order Strategic Placement with Adverse Selection Risk

- Deep order flow imbalance: Extracting alpha at multiple horizons from the limit order book

- Order Book Filtration and Directional Signal Extraction at ... - arXiv