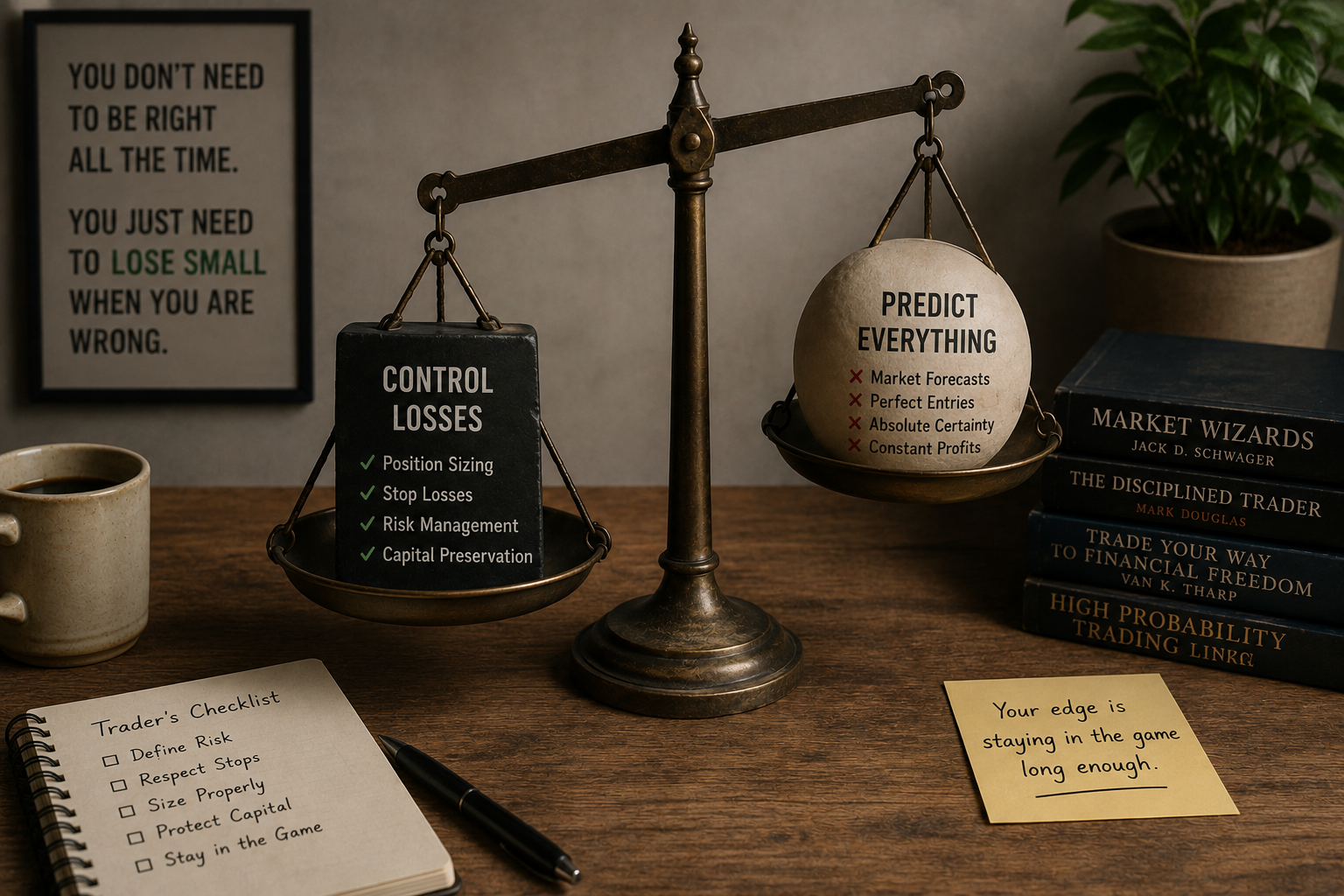

1.5 The Trader's Real Job: Control Losses, Not Predict Everything

Most traders focus on predicting markets instead of controlling risk. But survival, not prediction, is what compounds capital. Position sizing, drawdown limits, stop placement, and kill criteria matter more than being right about direction.

Most retail trading effort is allocated to the wrong job. The trader spends 90% of their attention on direction, which is outside their control, and 10% on position size, stop placement, and kill criteria, which are inside it. The math punishes the allocation. Direction has bounded informational return in the long run. Loss control has unbounded protective return in the short run. The trader who flips the split outlasts the one who does not.

Variables outside your control

Stack the five variables that decide your equity curve.

Direction. You do not know which way price moves next. You have a conditional expectation that shifts the distribution by a small amount in a measurable direction. You do not have certainty. No model removes this, and no amount of effort changes it.

Volatility. Realized volatility on any instrument varies by 3x to 5x between calm and active regimes. You do not control when the calm regime ends. You can measure the regime; you cannot schedule it.

Regime. Trend regimes turn into range regimes turn into crash regimes. The transitions are dated only in hindsight. In live trading, you see the transition once it has cost you something.

Returns. Even at full information about the rule, the return realized on any single trade is drawn from a distribution. The realized number is one sample, not a parameter.

Decay. Every working rule decays. You did not put it on a schedule. The market did.

These five variables together produce your equity curve. None of them respond to effort. None of them respond to attention. A trader who tries to control them through more analysis is paying for the illusion of control with real time.

Variables under your control

A different stack responds to discipline.

Position size per trade. Set it. Hold it.

Maximum risk per trade as a percentage of account equity. Set it. Hold it.

Maximum exposure across open trades. Set it. Hold it.

Drawdown stop on the account. The level at which all systems go flat regardless of signals. Set it. Hold it.

Kill criteria per system. The conditions under which an individual system is switched off. Set them in writing before going live. Hold them.

Cost assumptions. The slippage and spread numbers used to evaluate a rule. Set them above the worst observed live values. Refuse rules whose net edge depends on optimistic friction.

Diversification. The count and correlation of systems running at the same time. Set the rule for adding new systems. Set the cap on capital per system.

These seven knobs are the trader's actual control surface. They are not the sexy part. They do not make a podcast interesting. They are the entire job.

Loss control is the survival function

A trader's equity over time is the product of expected return per trade and survival. Expected return per trade is the slow variable. It changes by basis points across systems. Survival is the fast variable. It is the difference between a 20% drawdown and a 60% drawdown on the same expected return path.

Two traders, same system, same expected return per trade, same trade count. Trader A caps per-trade risk at 0.5% of equity. Trader B caps it at 4%. The system has a 55% win rate and a 1.2 reward/risk ratio. Over 200 trades:

- Trader A expects a 95th-percentile drawdown around 8% and ends the year up around 20%.

- Trader B expects a 95th-percentile drawdown around 35% and ends the year up around 60%, conditional on surviving the drawdown.

Trader B does not survive the drawdown in most paths. The combination of equity stress and emotional pressure produces an exit before the curve recovers. Trader B was right about direction in the same percentage of trades as Trader A. Direction did not save Trader B. The blowup was a loss-control failure.

The lesson sits at a different layer than most trading content addresses. The asymmetry lives in the survival function.

Control discipline compounds the edge

Three numbers tell the story.

A trader who keeps per-trade risk at 1% and runs a system with a 0.6 Sharpe finishes a 5-year run with an expected drawdown around 12% and a compound return around 35%. Survivable. Repeatable.

The same trader on the same system who lets per-trade risk drift to 3% during winning streaks and back to 1% during losing streaks finishes the same 5-year run with an expected drawdown around 25% and a compound return around 38%. Marginal return improvement. Drawdown depth around double.

The same trader at a flat 4% per-trade risk finishes the run with an expected drawdown around 45% and a compound return around 60%, conditional on not closing the account during the drawdown. Most paths do not survive.

The compound return numbers look like the trader is being rewarded for taking more risk. The drawdown numbers tell the survival story. The trader who held per-trade risk constant at 1% was the only one whose path stayed executable across human emotional states.

Loss control is what lets a small per-trade edge compound. Edge that cannot compound exists only on the backtest.

MAE-based stop placement

The mechanics of where to place a stop are not vibes. They come from the trade distribution.

Take every closed trade in the backtest. For each trade, record two numbers: the maximum adverse excursion (the worst intraday drawdown the trade went through before closing) and the final P&L. Plot the distribution.

A stop placed inside the MAE distribution cuts trades that would have recovered. A stop placed outside the MAE distribution does not protect against the trades that would have failed. The right stop sits at the boundary where the MAE distribution of losing trades stops overlapping with the MAE distribution of winning trades.

The right stop sits inside a region of the surface, not a single point. The region is the flat part of the net-profit-vs-stop-distance curve, where moving the stop 20% in either direction changes net profit by less than 5%. A stop that sits on a spike, where moving it 10 pips halves net profit, is curve-fit and will die in live trading.

The same logic applies to the account-level drawdown stop. The kill point sits at a multiple of the historical worst drawdown, large enough to absorb normal variation and small enough to preserve redeployable capital. A 1.5x multiplier on the worst historical drawdown is a starting point. Tighten from there based on capital constraints.

The illusion of control

The reframing is hard because prediction is the part of trading that feels like skill. The chart pattern, the macro narrative, the regime call, the indicator divergence. Loss control is the part of trading that feels like clerical work. Set the size and the stop. Walk away.

The market pays the clerk and burns the analyst. The clerk is doing the only job that responds to effort. The analyst is paying for the feeling of being able to forecast the variables outside their control.

Two consequences fall out of this.

First, most trading education sells prediction because prediction is what people want to buy. The audience pays for chart patterns, narrative trades, and proprietary indicators. Few pay for "I am going to make you set a stop and not move it." The market for trading education is misaligned with the market for trading survival.

Second, your own attention is the scarce resource. Every hour you spend refining a signal at the third decimal place is an hour not spent improving your control surface. The marginal hour on signal research is worth less than the marginal hour on risk-rule audit, given how poorly most retail risk rules are written.

Reallocate the 90/10 split.

Reading the equity curve

You can read whether a trader is doing the right job from the equity curve shape, not from the headline number.

Loss-controlled equity curves are choppy and grinding. They have shallow drawdowns and slow recoveries. They look boring. They produce mid-teens annual returns over many years with single-digit worst drawdowns.

Prediction-focused equity curves are steep and dramatic. They have sharp rises and 40%+ drawdowns. They look exciting. They produce double-digit annual returns in good years and end the account in the bad ones.

The first curve is repeatable across paths. The second is one path out of many, sampled by survivorship bias. The traders showing the second curve in screenshots are the ones who survived. The ones who did not are gone.

A live curve that looks like the second one points to the loss-control surface, not to the rule. Cap per-trade risk lower. Set the account drawdown stop tighter. Cut the count of simultaneous open positions. Realized return drops. Realized survivability rises. Survivability is the only variable that lets the edge compound.

KEY POINTS

- Direction, volatility, regime, returns, and decay sit outside trader control. Effort spent on them is paid in attention with no return.

- Position size, per-trade risk, drawdown stop, kill criteria, cost assumptions, and diversification sit inside trader control. They are the entire job.

- Survival, not signal, is the asymmetric variable. Two traders with the same rule and different per-trade risk produce different equity curves and different career lengths.

- Set loss-control points before the trade opens. The MAE distribution of historical trades shows where stops belong.

- A stop on a stable region of the optimization surface survives. A stop on a spike is curve-fit.

- Account-level drawdown stops sit at a multiple of the historical worst drawdown, large enough to absorb noise and small enough to preserve redeployable capital. 1.5x is a starting point.

- Boring grinding curves with shallow drawdowns are the signature of correct allocation. Steep curves with 40%+ drawdowns are survivorship bias, not skill.

- Reallocate research attention from signal refinement to risk-rule audit. The marginal hour on the control surface is worth more than the marginal hour on the signal.

References

- Evidence-Based Technical Analysis - David Aronson (Amazon)

- Systematic Trading - Robert Carver (Amazon)

- Evidence-Based Technical Analysis: Applying the Scientific Method and Statistical Inference to Trading Signals

- Traditional Traders vs. Quant Traders: A Comparative Analysis of Strategies, Performance, and Market Interactions

- Comparing Discretionary and Systematic Hedge Fund Performance

- The Power of Price Action Reading

- Portfolio Liquidity and Diversification: Theory and Evidence

- A Comprehensive Review of Statistical Methods in Quantitative Finance

- An Overview of Global Macro (chapter, in Global Macro Trading)

- The Classification and Regulation of Automated Trading Systems