4.69 Why a Weak Dollar Means Strong Commodities

Commodities are priced in dollars, so a weaker dollar makes them cheaper abroad, lifts foreign demand, and raises their price, which lifts the commodity currencies. Use it as a directional gate, and count the dollar once.

Crude, copper, gold, wheat, all of them carry a price tag written in dollars. That single fact is the reason commodity prices and the dollar lean against each other, and it is more mechanical than most intermarket links in this pillar. The old article "Gold, Dollar, and Rates: A Practical Intermarket Map" worked one corner of this with gold; the same logic runs across the whole commodity complex, and it feeds straight back into the commodity currencies.

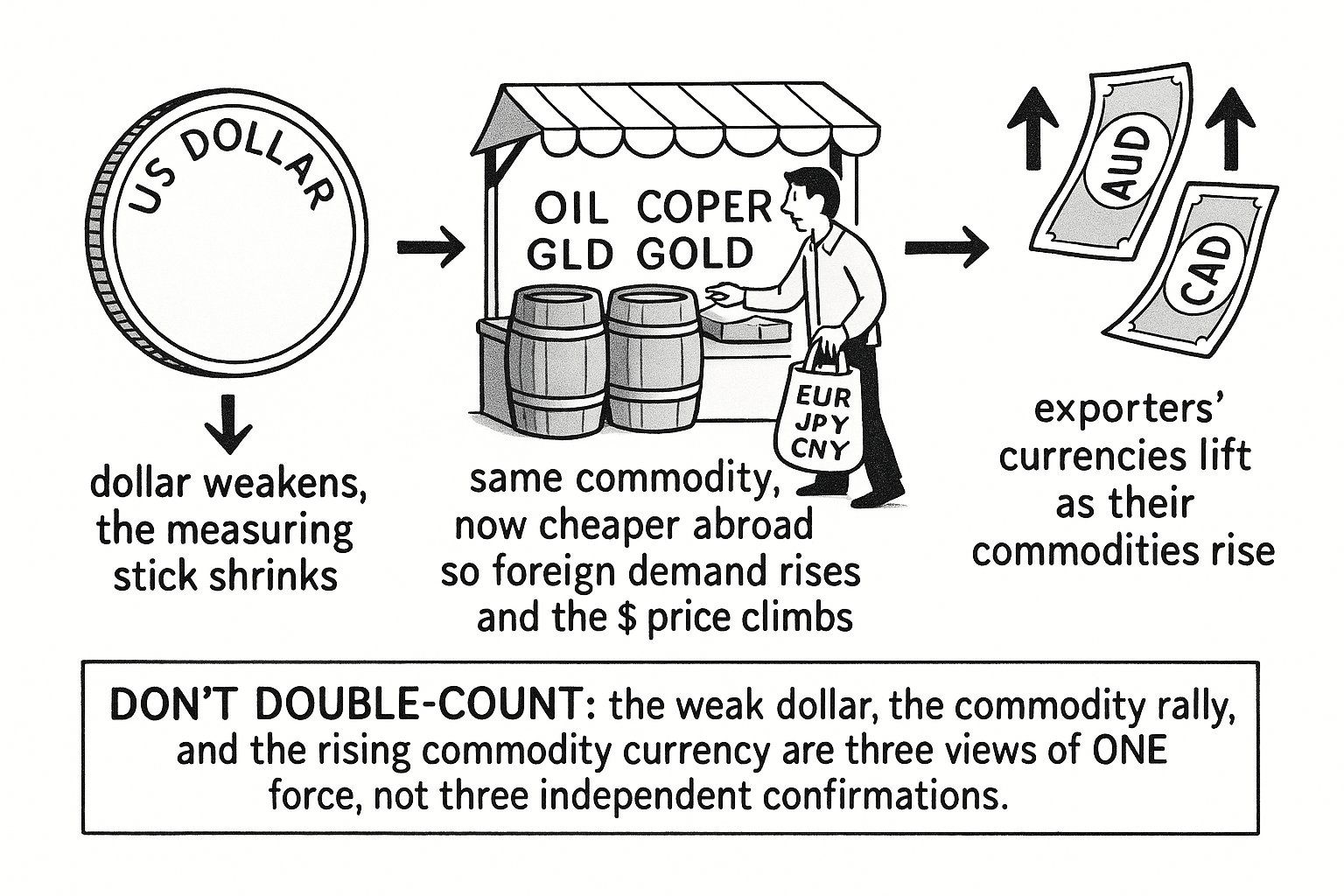

Start with the arithmetic, because it is cleaner than any story. A barrel of oil has some real value to a refiner in Europe or Japan, set by supply and demand for energy. The dollar price of that barrel is the real value translated through the dollar's exchange rate. Hold the real value fixed and weaken the dollar, and the dollar price has to rise to represent the same real worth. Nothing about oil changed. The measuring stick shrank, so the number printed in dollars got bigger.

The mechanism: a cheaper dollar makes commodities cheaper abroad, so demand lifts the price

The arithmetic has a behavioral engine behind it that turns a measurement effect into a real price move. When the dollar weakens, a commodity priced in dollars instantly becomes cheaper for anyone holding euros, yen, or yuan, because their currency now buys more dollars and therefore more of the dollar-priced commodity. Cheaper goods draw more buyers, foreign demand rises, and that real demand pushes the actual price up rather than just rescaling the quote.

$$ P^{\text{foreign}} = P^{\text{USD}} \times \frac{1}{\text{USD strength}} $$

The price a foreign buyer pays in their own currency equals the dollar price times the inverse of the dollar's strength against that currency. Weaken the dollar, the inverse term rises, and for an unchanged dollar price the foreign buyer would pay more, but the chain runs the other way in practice: the foreign buyer was about to pay less, so demand picks up, and the extra demand pulls the dollar price up until the foreign-currency cost settles back. A worked feel: crude sits at 80 dollars, and a European buyer with the euro at 1.10 pays about 72.7 euros. The dollar drops 5% against the euro (euro to 1.155), and if crude held at 80 the European pays only 69.3 euros, a 5% discount on the same barrel. That discount is the trigger; European demand lifts, and crude's dollar price drifts up toward the level that restores the euro cost. The weak dollar did not change the oil. It changed who could afford it and at what dollar number.

This is why the link shows up as a broad, persistent inverse correlation between the dollar index and commodity indices, not a tick-for-tick mirror. The old article "Gold, Dollar, and Rates: A Practical Intermarket Map" used exactly this for gold, where gold-up is a direct dollar-down read; the same reasoning generalizes to the whole complex because they all share the dollar denominator.

From commodities to the commodity currencies

The payoff for an FX trader is the second link in the chain, because a weak dollar lifting commodities lifts the currencies of the countries that export them. The old article "Why FX Traders Must Watch Gold, Rates, and Equities" laid out the per-currency commodity map, and the dollar sits underneath all of it. A weak dollar pushes crude up, and a higher crude price improves Canada's terms of trade and feeds the loonie, the chain the old article "Crude Oil, Inflation, and FX" worked through the trade balance and the inflation-then-rates channel. The same weak dollar pushes metals up and feeds the Aussie through copper, gold, and iron ore.

This produces a double-counting trap worth naming. A long-AUDUSD trade is partly a short-dollar trade by construction, since the dollar is the quote leg, and it is also a long-commodity trade through the Aussie's exports, and the commodities are themselves moving on the dollar. The dollar, the commodity, and the currency are three readings of an overlapping force, not three independent confirmations. Counting a weak dollar, a copper rally, and a rising Aussie as three votes for the same position is counting the dollar three times, the same correlated-confirmation warning the old article "Why FX Traders Must Watch Gold, Rates, and Equities" attached to its confirmation count.

Each currency to its own commodity

The chain is general but the wiring is specific, and watching the wrong commodity for a given currency adds noise. Each commodity currency links to the input that dominates its export economy, the per-currency map the old article "Why FX Traders Must Watch Gold, Rates, and Equities" built out.

| Currency | Primary commodity link | Why |

|---|---|---|

| CAD | crude oil | oil is Canada's dominant export, the loonie tracks crude |

| AUD | gold, copper, iron ore | Australia exports metals, the Aussie tracks the metals complex |

| NZD | dairy | New Zealand's export base is agricultural, dairy prices lead |

| NOK | crude oil | Norway is an oil exporter, the krone tracks crude |

The dollar denominator sits under every row, so a broad dollar move tends to lift all the commodity currencies together (the bloc behavior from the old article "Correlation Regimes: Positive Feedback, Breakdowns, and 'USDCAD Is the Truth'"), while a commodity-specific move (an oil supply shock, a dairy auction surprise) separates them and is what lets you trade one commodity currency against another. The cross between two commodity currencies is largely a bet on their two commodities' relative move, with the shared dollar cancelled out, the same cancellation the old article "Cross-Pair Signals: Can EUR Predict GBP?" used.

Where it earns its keep and where it lies

Used as a directional cross-check, the link is one of the more reliable in intermarket FX because the denominator mechanism is real rather than a fitted correlation. A long-commodity-currency trade taken while the dollar is broadly strengthening is fighting the denominator, and a short-dollar view gets confirmation from a rallying commodity complex. It is a clean read precisely because it is arithmetic before it is behavioral.

The honest failures are specific. The dollar is not the only thing moving a commodity, and a genuine supply shock swamps the dollar link entirely: an OPEC cut or a mine strike can rally crude or copper while the dollar is also rising, the supply-driven case the old article "Crude Oil, Inflation, and FX" flagged, and reading that rally as a dollar-weakness signal gets the dollar backwards. The correlation is non-stationary and can invert in a risk-off panic, when the dollar rallies as a safe haven while commodities and the commodity currencies all fall together, the dollar-smile and correlation-to-one regimes from the old articles "Why FX Traders Must Watch Gold, Rates, and Equities" and "Correlation Regimes." Gold carries an extra wrinkle the old article "Gold, Dollar, and Rates: A Practical Intermarket Map" insisted on, since it tracks real yields and the dollar at once, so a gold move is not a pure dollar read. And the double-counting trap is the easiest way to fool yourself into thinking a single dollar bet is a diversified, multiply-confirmed thesis. Use the link as a directional gate and a sanity check on the dollar leg, separate dollar-driven commodity moves from supply-driven ones before trusting it, and count the dollar once.

KEY POINTS

- Commodities are priced in dollars, so the dollar is the measuring stick. Weaken the stick and the dollar price of an unchanged commodity rises, before any real supply or demand changes.

- The behavioral engine: a weak dollar makes dollar-priced commodities instantly cheaper for foreign buyers, foreign demand rises, and the real demand pushes the actual dollar price up. A 5% dollar drop hands a European crude buyer a 5% discount, which lifts demand and the price.

- The link is a broad, persistent inverse correlation between the dollar and commodity indices, not a tick-for-tick mirror, and it generalizes the gold-dollar relationship to the whole complex because they share the dollar denominator.

- The FX payoff is the second link: a weak dollar lifts commodities, which lifts the exporters' currencies (crude to the loonie, metals to the Aussie). The dollar sits under the whole per-currency map.

- Double-counting trap: a long-AUDUSD trade is a short-dollar trade, a long-commodity trade, and the commodity is moving on the dollar. Those are three views of one force, not three independent confirmations. Count the dollar once.

- Wire each currency to its dominant export (CAD-crude, AUD-metals, NZD-dairy, NOK-crude). A broad dollar move lifts them together; a commodity-specific shock separates them and lets you trade one against another.

- Limits: a real supply shock swamps the dollar link and inverts the read, the correlation flips in a risk-off panic (safe-haven dollar rallies while commodities fall), gold tracks real yields too, so separate dollar-driven from supply-driven commodity moves and use the link as a directional gate, not a standalone trigger.

References

- Commodity prices and the US dollar (FRED data and discussion)

- The Dollar and Commodity Prices (IMF working paper)

- Purchasing power parity (Wikipedia)

- Terms of trade (Wikipedia)

- Commodity currency (Wikipedia)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Commodity prices, interest rates and the dollar

- The Relationship between Commodity Prices and Currency Exchange Rates: Evidence from the Commodity Currencies

- Commodity Currencies and Monetary Policy

- The market microstructure approach to foreign exchange

- Foreign Exchange Market Microstructure and the WM/Reuters 4pm Fix

- Exchange rates and commodity prices: Measuring causality at multiple horizons

- Commodity price effects on currencies

- Commodity prices and the US dollar - ScienceDirect.com