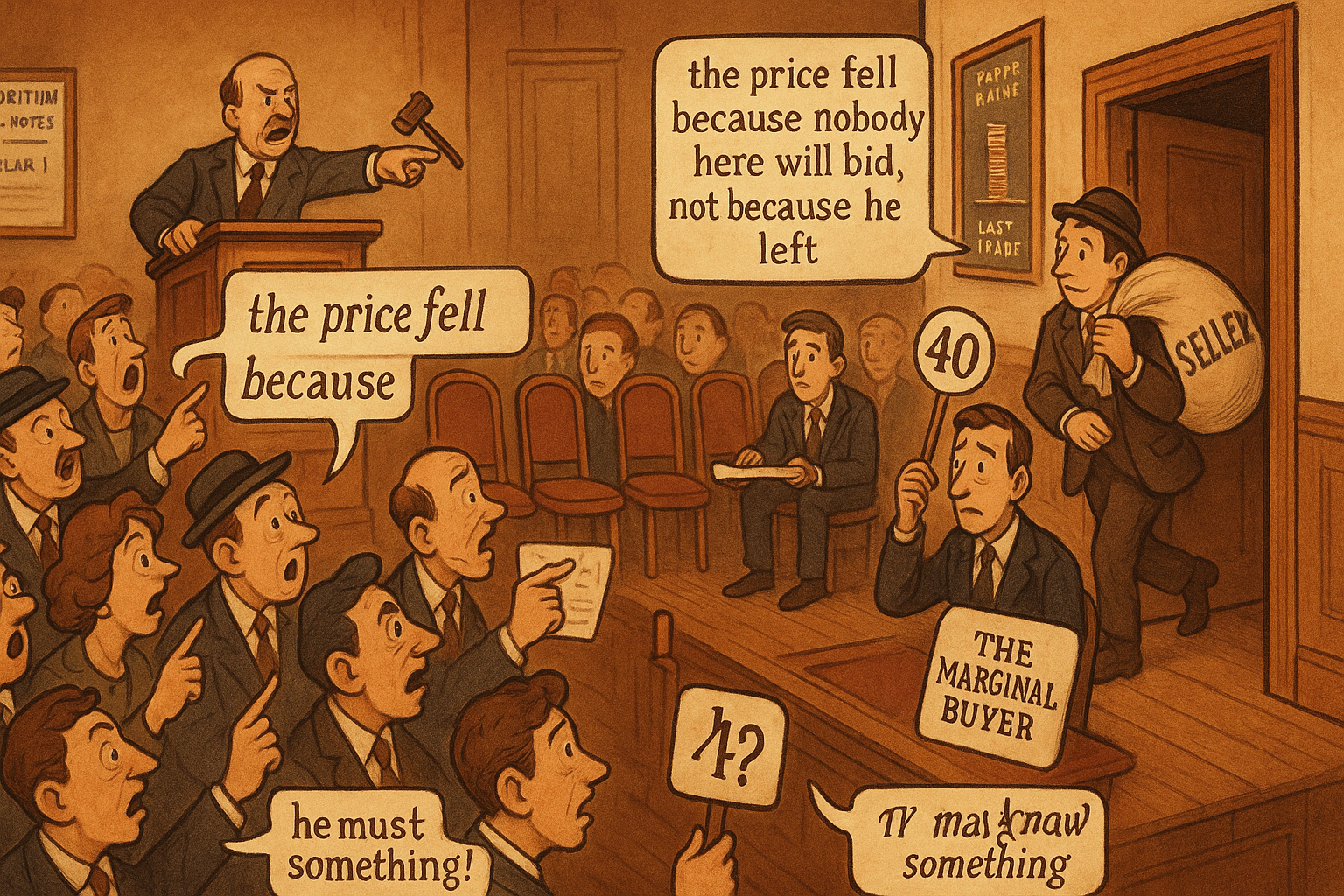

1.25 Who Is the Marginal Buyer?

The seller is easy to picture, so everyone narrates the seller after a crash. Price is set at the margin: the question that forecasts anything is who the marginal buyer is, and where they step back.

A thinly traded name gives back a quarter of its value before lunch, and the explanations land before the tape settles. A big holder dumped. The float was always fake. Somebody knows something the rest of us don't. Each of these talks about the seller, and each one feels right because you can see the seller in your head. People sell to pay for things, so a wave of exits is easy to picture. Almost nobody asks the question that actually fixed the number on the screen: who was willing to pay $40 a share for a speculative position, and why did they walk away?

Price is set at the margin. The seller's story tells you nothing about where price goes next, because the move was never about the seller alone. It was about the buyer who stood there yesterday and is gone today.

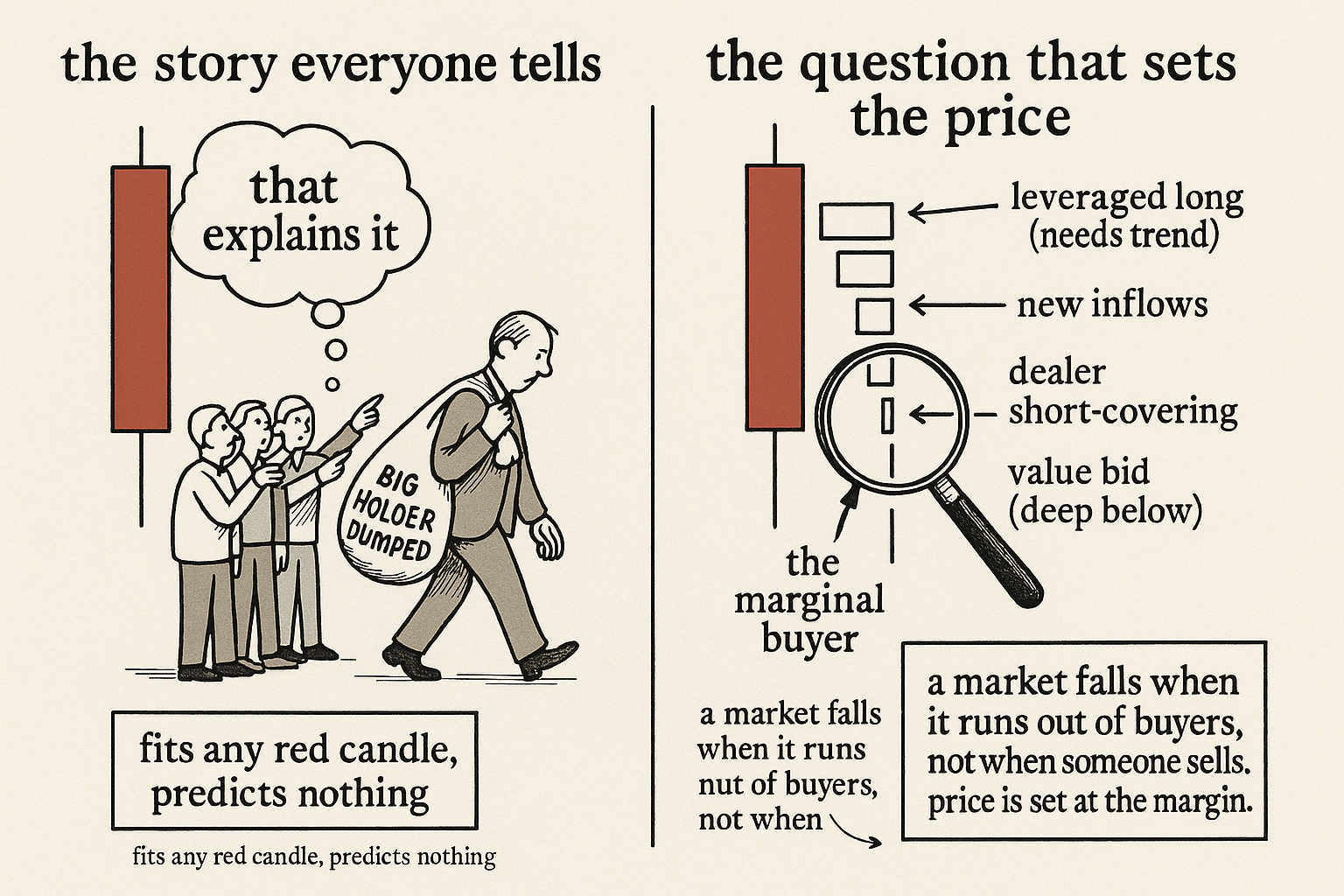

Price is set by the marginal trade, not the average holder

A market clears where the most desperate seller meets the least reluctant buyer. The number on the screen is the last price at which one marginal buyer and one marginal seller agreed, and that trade is a sliver of the float. Everyone else holding the position never transacted at that price. They are along for the ride on a valuation set by a tiny fraction of supply.

$$ \text{paper value} = P_{\text{last}} \times \text{supply}, \qquad P_{\text{last}} = \text{price of the marginal trade} $$

Read it as: the headline valuation multiplies the last traded price by the entire supply, but that last price came from the marginal trade alone, often a rounding error against the float. Mark ten million shares to a price set by a few hundred changing hands and you get a paper number nobody could realize by selling. The valuation holds only at the margin and only for the next small clip. That is why a position with a half-billion paper cap can shed a third of it in a session without anything close to a half-billion of selling. The marginal buyer stepped back, and the whole stack reprices to wherever the next willing buyer sits.

A market falls because it runs out of buyers, not because someone sells

The cleanest way to feel this: a market does not need a seller to fall. It needs the bids to disappear. With no bids, the position goes to zero on the spot, and nobody had to sell a single share to make that happen. You ran out of buyers. The recurring puzzle, how does price drop if no one is selling, is the same confusion in a different costume. Selling is not the cause. The withdrawal of the marginal buyer is the cause, and selling is the visible symptom that earns the headline.

Turn your attention to the bid side and the down move stops being a mystery. Somebody was absorbing supply at the old level. They ran out of capital, ran out of conviction, or marked their reservation value lower. The size of the drop is the distance to the next buyer standing firm.

The seller's story is explanation; the buyer's question is prediction

The old article "The Difference Between Explanation and Prediction in Markets" drew the line that matters here. Narrating the seller is explanation: a tidy after-the-fact account that feels like understanding and carries no forecast. You can pin "a big holder dumped" to any red candle, which is the reason it predicts nothing. An explanation that fits every outcome constrains none of them.

Asking who the marginal buyer is forces you into prediction, because you have to name a cohort and a price at which they will or will not show up. Leveraged longs adding on strength. New inflows from a fresh allocation. Dealers covering a short they were forced into. Index or fund flows that buy regardless of view. Each is a buyer with a different trigger and a different reservation price, and each can be modeled, falsified, and watched. The moment you switch from "who sold" to "who buys here," you stop collecting stories and start building a demand curve.

What the question buys you

If you cannot name a willing buyer at the current price, the price has nothing under it. That is the practical payoff. A level holds only because of the buyers who will defend it, and an inventory of those buyers tells you where the air pockets sit. When the only marginal buyer you can identify is the leveraged long who needs the trend to continue, you are one liquidation cascade from learning how far down the next real bid lives.

This is where the old article "The Death of the Single-System Trader" rhymes. A trader who leans on one rule is one regime change from broke, and a price that leans on one cohort of buyers wears the same fragility under a different hat. If every marginal buyer at $40 is the same participant running the same playbook, their demand is one correlated bet, and it vanishes at once when the regime turns. A market with diverse marginal buyers, inflows and short-covering and value bids that activate at different prices, has structural support a single-buyer market lacks. Counting the kinds of buyer under a price is the demand-side version of counting uncorrelated systems in a portfolio.

Visualizing the marginal buyer

KEY POINTS

- Price is set by the marginal trade, a sliver of the float, not by the average holder; the headline valuation marks the entire supply to a price only the next small clip could realize.

- A market does not need a seller to fall, it needs the bids to disappear; running out of buyers, not the act of selling, is the cause of a down move.

- Narrating the seller is explanation that fits any outcome and forecasts nothing, the failure the old article "The Difference Between Explanation and Prediction in Markets" named.

- Asking who the marginal buyer is forces a prediction: name the cohort (leveraged longs, inflows, dealer short-covering, fund flows) and the price at which they show up or step back.

- If you cannot name a willing buyer at the current price, the level has no support; an inventory of marginal buyers tells you where the air pockets are.

- A price propped by one buyer type is one regime change from collapse, the demand-side echo of the old article "The Death of the Single-System Trader"; diverse marginal buyers are structural support.