1.26 Large Trades Are Insider Trades by Definition

A large order moves price by construction, so it manufactures the move it seemed to predict. Size needs capital and a firm view, which reads like information on the tape, so the market prices large flow as informed because it cannot tell you apart. Read the permanent impact to separate knowing from

A large market order moves the price whether or not the trader knows anything. It takes out the resting bids or offers, the book reprices around the hole it punched, and by the time the order finishes it has manufactured the very move it looked like it predicted. The trader did not need a secret. Size alone did the work. So the clean question is not whether a big trade was informed. It is whether the distinction even survives contact with the order book, and mostly it does not.

This piece sits at the seam between markets philosophy and microstructure, because the argument is half definitional and half mechanical. The mechanics come from the old article "Market Impact and the Square-Root Law: Walking the Book to Price Your Slippage." The philosophy is what those mechanics imply about who counts as an insider.

Size moves price by construction

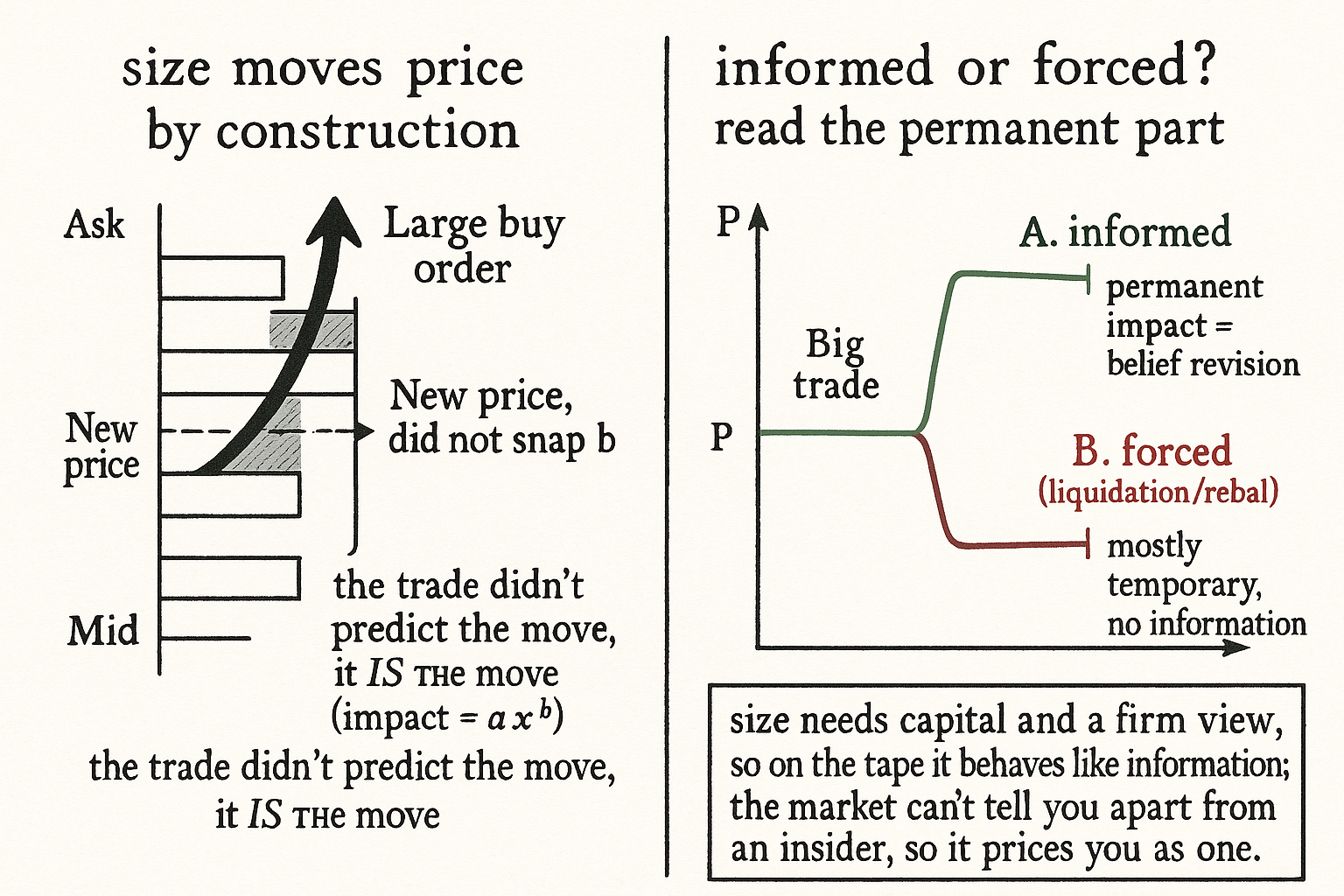

The old square-root article gave the shape. Walk a real order book with an order of size x and the slippage you eat follows a power law, impact equal to a times x to the power b, with b landing near one-half. The constant is the instrument's sensitivity, but the part that matters here is that the impact is non-zero for any order big enough to clear more than the top level.

$$ \text{impact}(x) = a \cdot x^{\,b}, \quad b \approx 0.5 \qquad\Longrightarrow\qquad \text{impact}(x) > 0 \text{ for large } x $$

Read it as: impact scales with order size raised to a power near one-half, and for a large order that quantity is strictly positive. There is no size large enough to be informed and small enough to be free. To move size, you move the price. The trade is not predicting the move. It is the move.

Why that makes the trader quasi-informed by definition

Size has a cost of entry. Committing real capital takes deep pockets and a view hard enough to risk them, because no one stakes that much on a thesis they hold loosely. From the tape's side, a participant with capital and a firm view behaves like someone trading on private information, and the book cannot separate the two while the order is live. Both leave the same footprint: a sweep through several levels and a book that reprices and does not snap all the way back.

The permanent part of that footprint is the tell. Split any impact into the piece that reverts and the piece that sticks.

$$ \Delta P = \underbrace{\text{temporary}}_{\text{reverts as book refills}} \;+\; \underbrace{\text{permanent}}_{\text{the market's belief revision}} $$

Read it as: the price change from a large trade has a temporary component that fades as makers refill the levels you ate, and a permanent component that the rest of the market keeps as a revised belief about value. The permanent component is information by behavior, regardless of intent. If a whale buys a billion because of genuine conviction or because of a forced short cover, the market still reads the residual as a signal and adjusts, because there is no way to query the whale's reasons and the safe assumption is that money that large knows something. Treating large flow as uninformed is the expensive assumption. Treating it as informed is the cheap one.

The maker's seat makes this concrete

From the market maker's chair this stops being philosophy. The old article "Using Trade Flow to Predict Short-Term Price Movement" built the signal: sign each trade by aggressor side, sum it over a decaying window, and the net signed flow predicts the next move because taker orders are autocorrelated, buys follow buys. Large flow is the strongest, most autocorrelated, hardest-to-fake version of that signal. You cannot spoof a trade that actually printed.

So a maker who gets run over by size does not waste time wondering whether the taker was a genuine insider. The maker skews the quote away from the flow and widens, because pricing large flow as toxic is the only assumption that survives a P&L review. Adverse selection does not care about the counterparty's motives. It cares about the footprint, and a large trade leaves the footprint of someone who knows. The market's revealed definition of an insider is whoever moves the price and makes it stick, and large traders do that by construction.

The caution: forced is not the same as informed

The argument has a real failure mode, and ignoring it costs money. Large does not always mean smart. A liquidation, a margin call, an index rebalance, or a fund unwinding a book all generate enormous signed flow with zero predictive information, and the permanent-versus-temporary split is exactly how you tell them apart. Forced flow tends to be mostly temporary impact: a violent move that reverts once the forced seller is done, because there was never a belief revision underneath it. Informed flow leaves a permanent mark because the rest of the market updates.

This also ties straight back to the old article "Who Is the Marginal Buyer?" A large buyer is not just reacting to the marginal price, they are setting it, becoming the marginal buyer for every unit they sweep. That is the same coin from the other face: the marginal trade sets the price, and a large trade is a marginal trade with enough size to drag the print somewhere new and leave it there. Follow the permanent component, not the headline size, and you are following information rather than someone else's forced exit.

Visualizing the large trade as information

KEY POINTS

- A large market order moves price by construction: it clears multiple book levels, so its impact (a·x^b with b near 0.5, from the old square-root-law article) is strictly positive for any real size. The trade is the move, not a forecast of it.

- Putting real size on takes capital and a firm view, and from the tape's side that behaves like trading on information; the market cannot tell a true insider from a large uninformed trader in real time because both leave the same footprint.

- Split impact into temporary (reverts as makers refill) and permanent (the market's belief revision); the permanent component is information by behavior, regardless of the trader's intent.

- From the maker's seat this is forced: large signed flow is the strongest, unspoofable version of the trade-flow signal from the old article "Using Trade Flow to Predict Short-Term Price Movement," so makers skew away and price it as toxic.

- The failure mode is forced flow: liquidations, margin calls, and rebalances move size with no information, and they show up as mostly temporary impact that reverts.

- A large trade is a marginal trade with enough size to reset the print, the other face of the old article "Who Is the Marginal Buyer?"; follow the permanent impact, not the headline size.