8.2 The Omori Law: Why Aftershocks Follow Market Crashes

After a crash the violent days keep coming, dense then fading along the same power-law curve geologists use for aftershocks. Independent returns can't do that, so size down for weeks, not days.

Seismologists noticed something over a century ago that traders rediscover the hard way after every crash: the big shock starts a decaying sequence of smaller shocks. After a major earthquake the aftershocks arrive fast at first, then taper off along a fixed mathematical curve. Markets do the same thing. The crash hits, and then the violent days keep coming, dense right after the break and thinning out over weeks, following the same curve geologists use for aftershocks. The old article "Why Financial Markets Are Complex Systems" argued that crashes are critical phenomena, not random draws. This is the cleanest evidence for that claim: the aftermath of a crash is structured, predictable in its decay, and impossible if returns were independent.

The aftershock curve, borrowed from geology

The Omori law describes how the rate of aftershocks decays after a big earthquake. Count the number of aftershocks per unit time above some size threshold, and that rate falls off as a power of the time since the main shock.

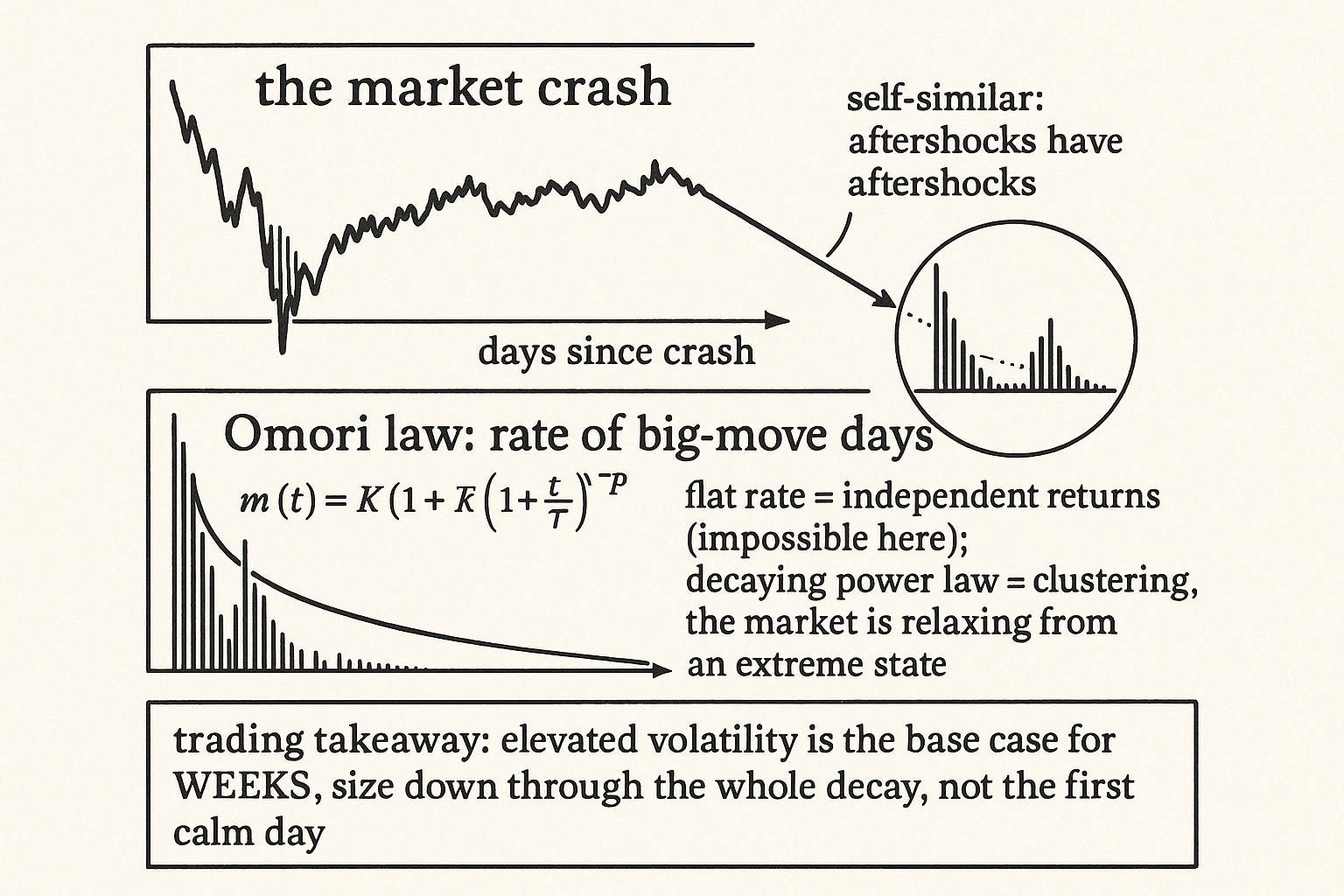

$$ m(t) = K\,(1 + t/\tau)^{-p} $$

Read it piece by piece. The term m(t) is the rate of aftershocks at time t after the main event, K and tau are constants that set the scale and the early plateau, and p is the exponent that controls how fast the rate decays, usually near 1. The shape is the point: a fast initial burst that bends into a slow power-law tail, so aftershocks stay more frequent than background for a long stretch after the shock. Now swap earthquakes for a market index and aftershocks for days where the absolute return exceeds a large threshold. Lillo and Mantegna ran that substitution and found the count of these threshold-exceeding days after a crash follows the same Omori curve, with volatility relaxing as a power law rather than snapping back or fading on an exponential.

Integrate that rate from the crash to time t and you get the cumulative number of big-move days, the thing you can watch tick up in real time.

$$ N(t) = \frac{K\left[(1 + t/\tau)^{1-p} - 1\right]}{1-p}\quad (p \neq 1), \qquad N(t) = K\,\ln\!\left(1 + t/\tau\right)\quad (p = 1) $$

The cumulative count N(t) grows fast at first and then bends over, the integral of a decaying rate. For a trader the formula matters less than what it rules out. A logarithmic or power-law cumulative count is what you see when the post-crash period has no fixed scale, when each day's chance of another violent move depends on how long ago the crash was. Independent returns cannot produce it.

Why this kills the independence assumption

Return the argument to the heart of the old article "Anomalous Diffusion in Financial Markets," which showed that price changes over successive intervals are correlated, not independent, because traders react to earlier moves. The Omori law is that correlation caught in its most dramatic form. If each day's return were an independent draw from some fixed distribution, the gap between violent days would itself be memoryless and the rate of big moves would be flat, not a decaying power law. The crash would carry no information about tomorrow. Markets refuse this. After a crash the conditional probability of another large move is elevated and comes down along a slow tail, so the days cluster, and that clustering is the signature of a system relaxing from an extreme state rather than a coin reshuffling its outcomes.

The structure goes deeper than a single crash. The aftershock sequence is self-similar: inside the relaxation period after a major break, smaller shocks set off their own miniature Omori sequences, aftershocks within aftershocks, the same power-law decay nested at finer scales. That self-similarity is the fingerprint of the complex, critical system the old article on complex markets described, and it is why a standard volatility model that assumes a single mean-reverting variance, like a plain GARCH specification, fails to reproduce the post-crash relaxation: the decay has no characteristic timescale to mean-revert toward.

What to do with it

Do not read this as a forecast of direction, because Omori says nothing about which way the aftershocks point, only that more violence is coming and roughly how its frequency will fade. The trading consequences are about risk, not entry signals. After a crash, treat elevated volatility as the base case for weeks, not days, because the power-law tail keeps the big-move rate high long after the headlines move on, and a volatility estimate that assumes a quick return to calm will understate your risk through the entire relaxation. Size down and keep sizing down until the aftershock rate has decayed, not for the first quiet session that tempts you back to full size. Expect the secondary shocks, the failed bounces and the second-leg-down days, as the normal anatomy of a post-crash tape rather than fresh surprises. And carry the lesson from the old article on complex systems into position management: the crash is a transition into a different regime with its own statistics, so the rules and volatility assumptions you calibrated in the calm period do not apply until the system has finished relaxing.

Visualizing the aftershock decay

KEY POINTS

- The Omori law from seismology says the rate of aftershocks after a big earthquake decays as a power law of time since the shock, a fast initial burst bending into a slow tail.

- Lillo and Mantegna showed market index returns obey the same law: after a crash, the count of days where the absolute return exceeds a large threshold decays along the Omori curve, with volatility relaxing as a power law.

- This is the strongest form of the correlation the old article "Anomalous Diffusion in Financial Markets" described. Independent returns would make big-move days memoryless and their rate flat, not a decaying power law, so the crash carries information about tomorrow.

- The aftershock sequence is self-similar: smaller shocks inside the relaxation period spawn their own nested Omori decays, the fingerprint of the critical system from the old article "Why Financial Markets Are Complex Systems."

- A single mean-reverting volatility model like plain GARCH cannot reproduce the post-crash relaxation, because the power-law decay has no characteristic timescale to revert toward.

- Use it for risk, not direction. After a crash, treat high volatility as the base case for weeks, size down through the entire decay rather than the first calm session, and expect secondary shocks as the normal anatomy of a post-crash tape.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Power law relaxation in a complex system: Omori law after a financial market crash (Lillo & Mantegna)

- Dynamics of a financial market index after a crash (Lillo & Mantegna)

- Relation between volatility correlations in financial markets and Omori processes occurring on all scales

- Aftershock prediction for high-frequency financial markets' dynamics

- Power Laws in Economics and Finance