2.73 Volume Momentum

Volume Momentum ignores price and asks one thing: is the tape hotter than its own baseline. Short volume over long volume, logged and CDF-squashed into a bounded regime gauge that tells you if your signals have fuel.

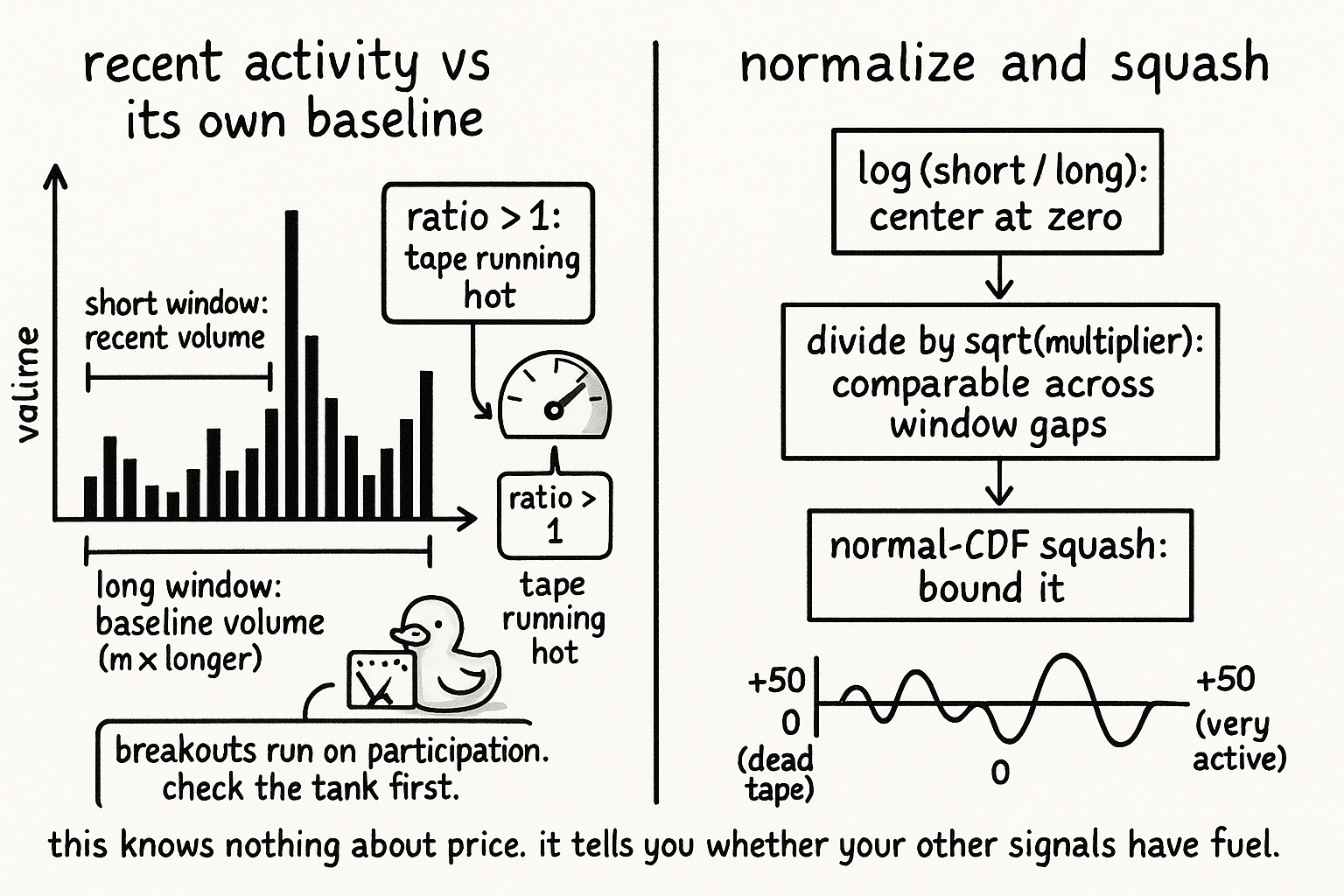

Every other volume indicator in this group ties volume to price, the close position, the direction of the change, the price level. This one ignores price entirely. Volume Momentum asks one question: is the market more active now than it has been, and by how much. That sounds trivial until you remember why activity matters. Volume surges precede and accompany regime changes, breakouts run on participation, and dead tape kills mean-reversion edges that need turnover to work. A clean reading of recent volume against its own recent baseline is a regime gauge, and like every raw volume quantity it is unusable until you normalize it. This article builds it from the same recipe the rest of the group uses: a short window over a long window, a log, and a CDF squash.

Recent activity against its own baseline

The construction borrows the structure of a price momentum oscillator and swaps price for volume. Take the average volume over a short recent window and divide it by the average volume over a longer window that sets the baseline, the way a fast moving average over a slow moving average reads price momentum. The longer window is a multiple of the shorter one, so a single lookback and a multiplier define both. Take the log of the ratio so the result centers on zero and the spread between an activity surge and an activity drought becomes symmetric.

$$ \text{Raw} = \log\!\left(\frac{\frac{1}{1 + m \cdot LB}\sum_{k=0}^{LB} V_k}{\sum_{k=0}^{m \cdot LB - 1} V_k}\right) $$

The numerator is recent average volume over the short window of length LB, the denominator the broader volume over the longer window scaled by the multiplier m. Their ratio reads above one when recent volume runs hot relative to the baseline and below one when the tape has gone quiet. The log does the same job it did in the volume-weighted MA ratio: it turns the multiplicative center of one into an additive center of zero and makes a doubling of activity and a halving of activity equal distances from the middle. The old article "Why Most Indicators Should Be Transformed Before Modeling" is the reason every one of these constructions ends with a log and not a raw ratio; a ratio bunched around one with a heavy upper tail is the textbook case for it.

Normalize for the multiplier, then squash

The log ratio still has a spread that depends on how far apart the two windows sit, governed by the multiplier. A wide gap between short and long windows produces a larger swing than a narrow gap, so to keep the indicator comparable across settings you scale by the square root of the multiplier before compressing. Then run it through a normal-CDF squash to bound the output and rescale to plus or minus fifty.

$$ V_{\text{norm}} = 100 \cdot \Phi\!\left(\frac{3 \cdot \text{Raw}}{\sqrt{m}}\right) - 50 $$

The Raw log ratio sits inside, divided by the square root of the multiplier to normalize for the window gap, times a constant of three to spread the bulk of the distribution across the linear region of the CDF rather than letting it bunch in the middle. Phi is the standard normal CDF, the bounded squashing transform from the old article "Taming Indicator Tails with Sigmoid Transforms", which maps the whole real line into a fixed interval while keeping the body of the distribution roughly linear and pulling rare volume spikes back inside the range. The minus fifty recenters the output to swing around zero. The result is a volume-activity oscillator on a fixed minus-fifty to plus-fifty axis, stationary, bounded, and comparable across instruments and across decades despite the relentless growth in raw volume.

A regime gauge, not a signal

Volume Momentum does not tell you which way to trade, because it knows nothing about price. It tells you whether the conditions your other tools assume are present. A reading near plus fifty says the tape is far more active than its baseline, which is when breakouts and trend continuations tend to have fuel and when the high-noise mean-reversion regime can flip; a reading near minus fifty says activity has collapsed, which is when momentum signals tend to fail for lack of participation and when illiquidity makes every fill expensive. Use it as a filter and a context variable, the input that decides which of your other indicators to trust right now, rather than as a thing you act on directly. This is the same role volume plays throughout the group, with the noise warning from the old article "Why Median Filters Are Useful for Volume and Outliers" still in force: volume is the most spike-prone series you will handle, so the smoothing built into the two windows is doing real work before the log and the squash ever see the data.

KEY POINTS

- Volume Momentum ignores price and measures only whether current activity runs hot or cold against its own recent baseline, a regime gauge rather than a directional signal.

- It divides average volume over a short window by average volume over a longer window set by a multiplier, the same short-over-long structure a price momentum oscillator uses, then takes the log to center on zero and symmetrize surges against droughts.

- The log is mandatory because a raw ratio bunched around one with a heavy upper tail is the textbook defect from the old article "Why Most Indicators Should Be Transformed Before Modeling".

- The log ratio's spread depends on the window gap, so dividing by the square root of the multiplier keeps it comparable across settings before a normal-CDF squash bounds it to plus or minus fifty, the transform from the old article "Taming Indicator Tails with Sigmoid Transforms".

- The two-window averaging does heavy smoothing before any transform sees the data, which matters because volume is the most spike-prone series you handle, the warning from the old article "Why Median Filters Are Useful for Volume and Outliers".

- Use it as a context filter: high activity is when breakouts and trend continuations have fuel, dead tape is when momentum fails and fills get expensive, so it decides which of your other indicators to trust now.