3.14 Market Personality: Why Gold, FX, Crypto, and Equities Need Different Systems

Markets have personalities: efficiency ratio, autocorrelation, skew, vol regime, macro driver. Six families, six framework fits. SPX is not gold, gold is not BTC. Match framework to personality.

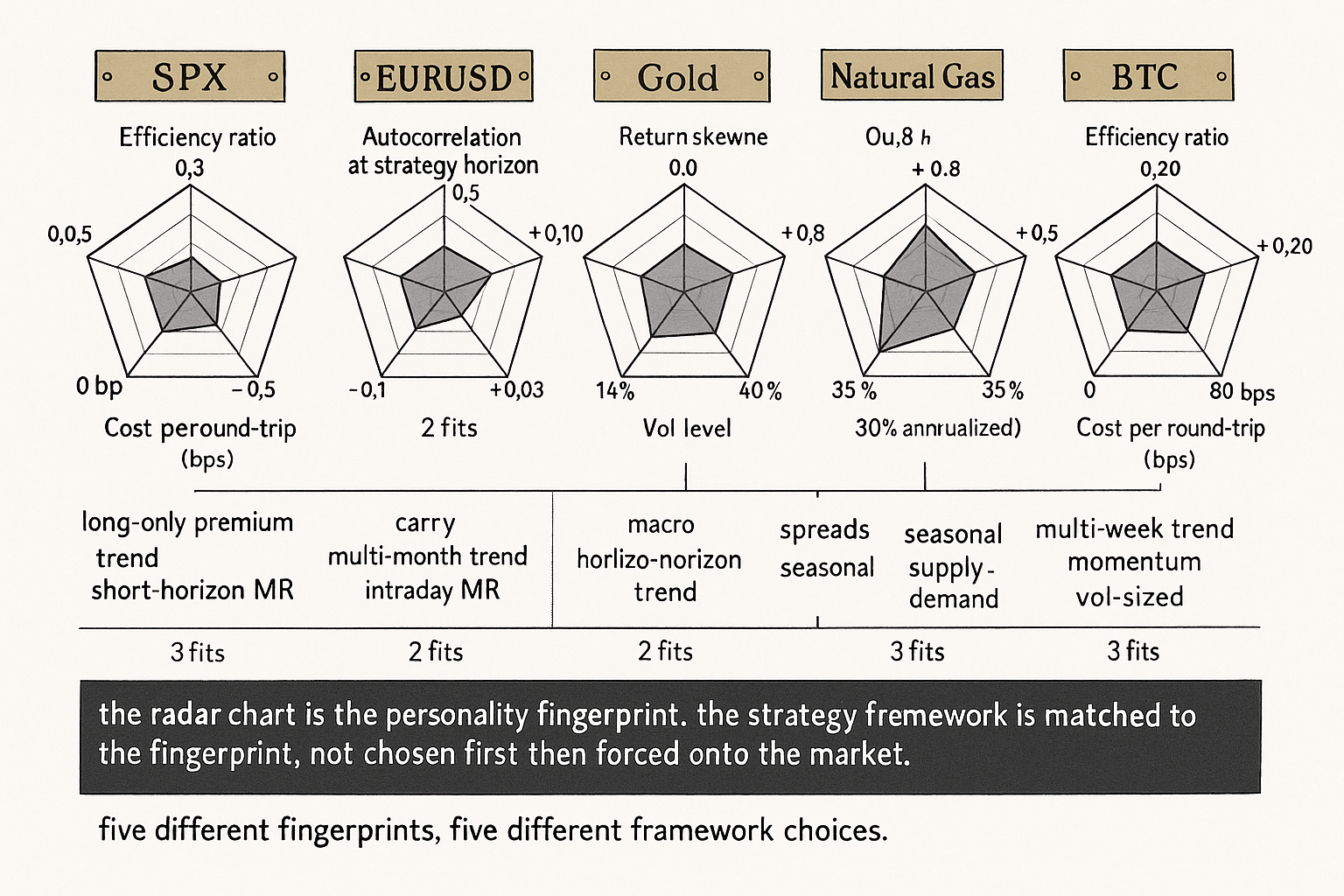

Compute the efficiency ratio (the ratio of net price change to total absolute path length over a fixed window) on five markets across the same calendar window of 2015-2024 with the same 22-day lookback. The values are diagnostic. SPX cash index: efficiency ratio averages approximately 0.30, with a long-run drift bias and persistent above-average ER during sustained bull regimes. EURUSD: efficiency ratio averages approximately 0.18, with no long-run drift and ER hovering near 0.20 across most regimes. Gold (XAU): efficiency ratio averages approximately 0.22, with two distinct regime modes (a low-ER chop mode below 0.15 and a high-ER trend mode above 0.30 during inflation hedging or risk-off episodes). Natural gas: efficiency ratio averages approximately 0.12, with high noise and seasonal-storage-driven shifts. BTC: efficiency ratio averages approximately 0.28, with extreme regime variation between 0.05 (sideways consolidation lasting months) and 0.50 (sustained breakout regimes lasting weeks).

Five different markets, five different efficiency-ratio profiles. The same trend-following strategy that earns Sharpe 0.6 on SPX (where ER is reliably 0.30 and trend persistence is the dominant feature) will earn approximately Sharpe 0.0 to 0.2 on natural gas (where ER is 0.12 and noise dominates) regardless of how the parameters are tuned. The strategy is not failing; the strategy is being misapplied to a market whose personality does not provide trend signal at the relevant horizon. The article "Why Works on All Markets Is Usually a Red Flag" gave the skeptical view of cross-market claims. This article gives the constructive complement: each market class has a personality determined by its participants, microstructure, and macro driver, and the strategy framework needs to match the personality.

The mistake that most retail and emerging-shop research makes is to treat markets as interchangeable backtesting venues. Run the same strategy on SPX, then on EURUSD, then on BTC, then on gold, and report the per-market results as if the strategy was tested across an unbiased sample of conditions. The conditions are very different. The strategy is doing different things on each market. The aggregated result is meaningless without the per-market context. The right discipline is to characterize each market's personality first, choose the strategy framework that matches the personality second, and only then begin parameter selection.

Personality, defined operationally

Five measurable dimensions, each diagnostic.

Dimension 1: efficiency ratio and noise level. The efficiency ratio measures how much of the total path length translates into net directional change. ER near 1 is pure trend. ER near 0 is pure chop with no net direction. Most markets sit between 0.1 and 0.4. Trend-following strategies need ER above approximately 0.25 to be profitable after costs. Mean-reversion strategies thrive at ER below 0.20.

$$ \text{ER}_W = \frac{|P_t - P_{t-W}|}{\sum_{i=1}^{W} |P_{t-i+1} - P_{t-i}|} $$

Dimension 2: autocorrelation structure. The first-lag autocorrelation of returns at the strategy's horizon. Positive autocorrelation favors trend strategies. Negative autocorrelation favors mean reversion. Near-zero autocorrelation argues for both being approximately useless. The article "Why Volatility Is More Non-Stationary Than Trend" framed the daily-horizon autocorrelation; the personality test extends to the strategy's actual horizon.

Dimension 3: return distribution shape. Skewness (right or left) and kurtosis (fat tails or thin tails). SPX has slightly negative skew (tail in losses) and high kurtosis. EURUSD has approximately zero skew and moderate kurtosis. BTC has positive skew (long-tail upside) and very high kurtosis. Gold has near-zero skew and elevated kurtosis. Natural gas has positive skew and extreme kurtosis. The shape determines which risk metrics are meaningful and which strategy P&L profiles are sustainable.

Dimension 4: volatility regime structure. The unconditional vol level, the vol-of-vol, the typical regime durations, the implied-vs-realized vol relationship. Covered in detail in "Volatility Regimes and Strategy Survival" and "Why Volatility Is More Non-Stationary Than Trend"; for cross-market comparison the relevant numbers are the unconditional vol level and the vol-of-vol relative to that level.

Dimension 5: macro driver and participant mix. SPX is dominated by institutional flow and ETF rebalancing, with a structural long-bias and a strong relationship to GDP growth and earnings. EURUSD is dominated by central-bank flows and trade balances. Gold is driven by real interest rates and macro hedge demand. BTC is driven by retail flows, exchange events, and a network effect. Natural gas is driven by weather, storage, and seasonal demand. Each driver implies a different signal hierarchy.

Strategy frameworks by market personality

Six market families with their structural strategy fits.

Family 1: large-cap equity indices (SPX, NDX, RTY, NIKKEI, EURO STOXX). High ER, structural long-bias, deep liquidity, low transaction costs. Suited for: long-only buy-and-hold (the equity premium), trend-following on multi-week horizons, mean reversion on short (1-5 day) horizons, factor strategies (value, momentum, quality, low-vol). Hostile to: pure carry, pure microstructure (already arbitraged out), strategies that depend on heavy directional shorts.

Family 2: G10 FX crosses (EURUSD, GBPUSD, USDJPY, AUDUSD). Low ER, near-zero unconditional drift, deep liquidity, very low costs (interbank). Suited for: carry trade (interest-rate differential), trend-following on multi-month horizons, mean reversion at intraday horizons, value-based strategies (PPP-deviation reversion). Hostile to: equity-style factor frameworks, microstructure strategies that assume retail-flow patterns.

Family 3: precious metals (gold, silver, platinum). Mixed ER (regime-dependent), near-zero drift, moderate liquidity, moderate costs. Suited for: macro-hedge positioning (real-rates, inflation), trend-following on medium horizons (gold has multi-year trends), volatility-conditioned position sizing. Hostile to: short-horizon mean reversion (the regime breaks come too suddenly), high-frequency strategies.

Family 4: industrial and energy commodities (copper, crude oil, natural gas). Low to mixed ER, no drift, seasonal patterns, wide spreads, storage and convenience-yield structure. Suited for: spread trades (calendar spreads, crack spreads), seasonal patterns, supply-demand-fundamental positioning. Hostile to: trend-following at short horizons (the noise dominates), naive long-bias (no positive expected return on the futures, only basis), strategies that ignore storage and roll structure.

Family 5: government bonds (US Treasuries, Bunds, JGBs). Mostly low ER, dominant central-bank flows, very deep liquidity, very low costs. Suited for: yield-curve trades, macro-conditional positioning, term-premium-based strategies. Hostile to: technical strategies that ignore the central-bank reaction function, equity-style trend-following, high-frequency strategies that fight the market-maker hierarchy.

Family 6: cryptocurrencies (BTC, ETH, major alts). High ER on regime-active periods, very high vol, high costs, fragmented liquidity, retail-dominated flows. Suited for: trend-following on multi-week horizons during active regimes, momentum on long horizons, vol-conditional position sizing. Hostile to: classical mean-reversion frameworks (the regime breaks are too violent), pair trades that assume stable cointegration, strategies that ignore exchange-specific risk and venue events.

The point of the families: a strategy framework is not market-agnostic. Each family demands a different framework and the wrong framework on the wrong family produces near-zero returns regardless of parameter tuning.

Diagnosing personality before strategy selection

A four-step protocol.

Step 1: compute the dimensions. ER, autocorrelation at strategy horizon, return distribution skewness and kurtosis, vol regime distribution, macro driver and participant mix. The first three are quantitative and produced by short scripts; the last two require domain knowledge.

Step 2: classify the market into a family. The article "Volatility Regimes and Strategy Survival" gave the operational regime gating; the family classification is one level above and is determined by the structural characteristics rather than the current regime.

Step 3: list the strategy frameworks compatible with the family. From the family-fit catalog above. Reject any framework that the family is hostile to before any backtesting.

Step 4: prototype the strategy in the framework with structural-prior parameters. The first backtest is at the structural prior, no optimization. The result tells you whether the framework matches the personality. If the prototype is profitable at the structural prior, optimization (with the discipline from "The Difference Between Robustness and Optimization") can improve it. If the prototype is near-zero or negative at the structural prior, optimization will not save it and the framework is wrong for the market.

Cases of personality drift

Market personalities are not perfectly stationary. The article "Slow Wandering: The Most Dangerous Type of Market Change" framed the slow-drift problem; the personality drift is one specific case. Three structural personality changes that have been visible in the data.

Change 1: equity microstructure transition. Pre-decimalization SPX (before 2001) had wider spreads, higher mean-reversion at short horizons, more visible market-making structure. Post-2010 SPX has tight spreads, weaker short-horizon mean-reversion, dominant ETF arbitrage. A strategy tested on 1995-2000 SPX that does not test on 2010-2024 is testing on a different SPX personality. The article "Microstructure change" (mechanism 3 in "Why Systems Work Until They Don't") is the operational manifestation.

Change 2: crypto market maturation. Pre-2017 BTC was a retail-heavy market with extreme regime breaks and low liquidity. Post-2020 BTC has institutional flows, futures and ETF infrastructure, and tighter spreads. The personality has shifted toward the equity-index family on multi-day horizons, while keeping crypto-specific traits at intraday horizons. Strategies tuned to 2014-2017 BTC will not generalize to 2024 BTC.

Change 3: FX response to monetary policy regimes. Pre-2008, G10 FX carry trades were the dominant flow. Post-QE the carry-rate dispersion compressed and the trade decayed (covered in "Slow Wandering: The Most Dangerous Type of Market Change"). Post-2022 with rate normalization, the carry trade has partly returned. The FX family's personality is regime-conditional in a way that requires monitoring rather than one-time characterization.

The protocol response: re-characterize the personality every few years and verify the strategy framework still matches. A strategy that was correctly framed in 2015 may be misapplied in 2025 if the personality drifted.

Anti-patterns

Five mistakes specific to market-personality misapplication.

Anti-pattern 1: applying the equity-index strategy framework to commodities. Commodities have no long-run drift and the equity-index trend strategy is implicitly long-biased. The strategy on commodities earns no premium and produces noise.

Anti-pattern 2: applying the FX carry framework to crypto. Crypto has no carry in the FX sense (the rate-differential premise is absent) and the regime breaks are too violent for a carry-style framework that assumes slow drift. The framework is misapplied.

Anti-pattern 3: applying the same strategy framework to a market whose personality changed structurally. Pre-2010 SPX is not the same market as post-2020 SPX, and a backtest spanning the structural change is testing two different personalities. Stratify by personality era as well as by regime.

Anti-pattern 4: ignoring transaction costs that vary by family. SPX costs are 1-2 basis points round-trip. Crypto costs are 50-200 basis points. The same gross signal that produces Sharpe 1.0 on SPX produces Sharpe 0.2 on crypto after costs, even with identical price dynamics.

Anti-pattern 5: assuming personality from headline stats only. SPX 14% annualized vol and EURUSD 8% annualized vol look like they differ only in scale. The personalities also differ in microstructure, drift, autocorrelation, and participant mix. Headline vol is one dimension; the personality is many.

Decision matrix

| Market family | Recommended frameworks | Hostile frameworks |

|---|---|---|

| Large-cap equity indices | Long-only equity premium, multi-week trend, short-horizon mean reversion, factor strategies | Pure carry, microstructure arbitrage |

| G10 FX | Carry, multi-month trend, intraday mean reversion, PPP-value | Equity factors, retail-flow microstructure |

| Precious metals | Macro-hedge, medium-horizon trend, vol-conditioned sizing | Short-horizon mean reversion, HFT |

| Industrial / energy commodities | Calendar spreads, seasonal patterns, supply-demand fundamental | Naive long-bias, short-horizon trend ignoring noise |

| Government bonds | Yield-curve trades, macro-conditional positioning, term premium | Technical strategies ignoring central-bank reaction |

| Crypto majors | Multi-week trend in active regimes, momentum, vol-conditioned sizing | Classical mean reversion, stable-cointegration pairs |

| Single-stock equities | Cross-sectional factors, event-driven, statistical arbitrage | Index-style trend without sector control |

| Volatility products (VIX futures, vol ETFs) | Term-structure trades, vol carry with explicit gating | Naive long or short positioning ignoring structure |

The matrix matches market family to compatible frameworks. The pattern: characterize the family first, select the framework second, optimize the parameters last.

Visualizing market personality

KEY POINTS

- Each market class has a personality determined by efficiency ratio, autocorrelation structure, return distribution shape, volatility regime, and macro driver / participant mix. The personality determines which strategy frameworks can earn an edge on that market.

- Five measurable dimensions: efficiency ratio (net change over total path length), autocorrelation at strategy horizon, return skewness and kurtosis, volatility regime distribution, macro driver and participant mix.

- Six market families with structural strategy fits: large-cap equity indices, G10 FX, precious metals, industrial/energy commodities, government bonds, cryptocurrencies. Each family demands different frameworks and is hostile to others.

- Equity indices suit long-bias trend, short-horizon mean reversion, and factor strategies. FX suits carry, multi-month trend, intraday mean reversion. Precious metals suit macro-hedge positioning. Commodities suit spreads and seasonal patterns. Bonds suit yield-curve and macro-conditional. Crypto suits multi-week trend and momentum with vol gating.

- A four-step diagnostic protocol: compute the personality dimensions, classify into a family, list the compatible frameworks, prototype at structural-prior parameters with no optimization. The prototype tells you whether the framework matches.

- Optimization at structural-prior parameters that produces near-zero or negative returns is a personality mismatch. Optimization will not save it; the framework is wrong for the market.

- Personalities are not stationary. Three documented structural personality changes: equity microstructure transition (pre-2001 vs post-2010), crypto maturation (pre-2017 vs post-2020), FX carry decay across QE eras. Re-characterize every few years.

- Anti-pattern: applying the equity-index strategy framework to commodities (no long-run drift). Anti-pattern: applying the FX carry framework to crypto (no carry in the FX sense, regime breaks too violent). Anti-pattern: same framework across pre- and post-personality-change eras. Anti-pattern: ignoring transaction-cost differences across families.

- The right discipline: characterize first, select framework second, optimize parameters last. The parameters are the smallest decision; the framework choice is the larger one; the personality understanding is the largest.

- The current article gives the constructive view. Combined with the prior article ("Why Works on All Markets Is Usually a Red Flag"), the operational rule: claim cross-market robustness only within a family, and check the personality before claiming any cross-family generalization.

- The next article in the publication ("Optimization Comes After Testing, Not Before") covers the procedural sequencing that follows from this framework: test at structural-prior parameters first, optimize last.

References

- Testing and Tuning Market Trading Systems - Timothy Masters (Amazon)

- Data Mining Algorithms in C++ - Timothy Masters (Amazon)

- THE RETURN OF THE ROGUE

- HedgeAgents: A Balanced-aware Multi-agent Financial Trading

- Machine Learning Enhanced Multi-Factor Quantitative Trading - arXiv

- TECHNICAL ANALYSIS - CFA Institute Research and Policy Center

- Towards Multi-agent Financial System via Simulated Trading - arXiv

- SHARP: A Self-Evolving Human-Auditable Rubric Policy for ... - arXiv

- Agentic AI in Derivatives Markets: Counterparty, Risk, and the

- AlphaForgeBench: Benchmarking End-to-End Trading Strategy