6.8 Why Portfolio Construction Is Part of the Signal

The signal sets direction; construction decides how much of each you own, moving the result as much as the signal. Correlation, costs, and limits enter here, so construction is alpha.

Traders draw a clean line between the signal and the portfolio: the signal decides what to trade, the portfolio is just plumbing that turns the decision into positions. That line is fake. How you combine, weight, and net your positions changes what the strategy actually predicts, so portfolio construction is not a downstream wrapper around the signal; it is part of the signal. Two desks running the identical raw forecast and different construction end up with different strategies, different return streams, and different risk, which is why "From Indicator Value to Expected Value" and the sizing articles in this pillar are not separate from the alpha. They are the alpha.

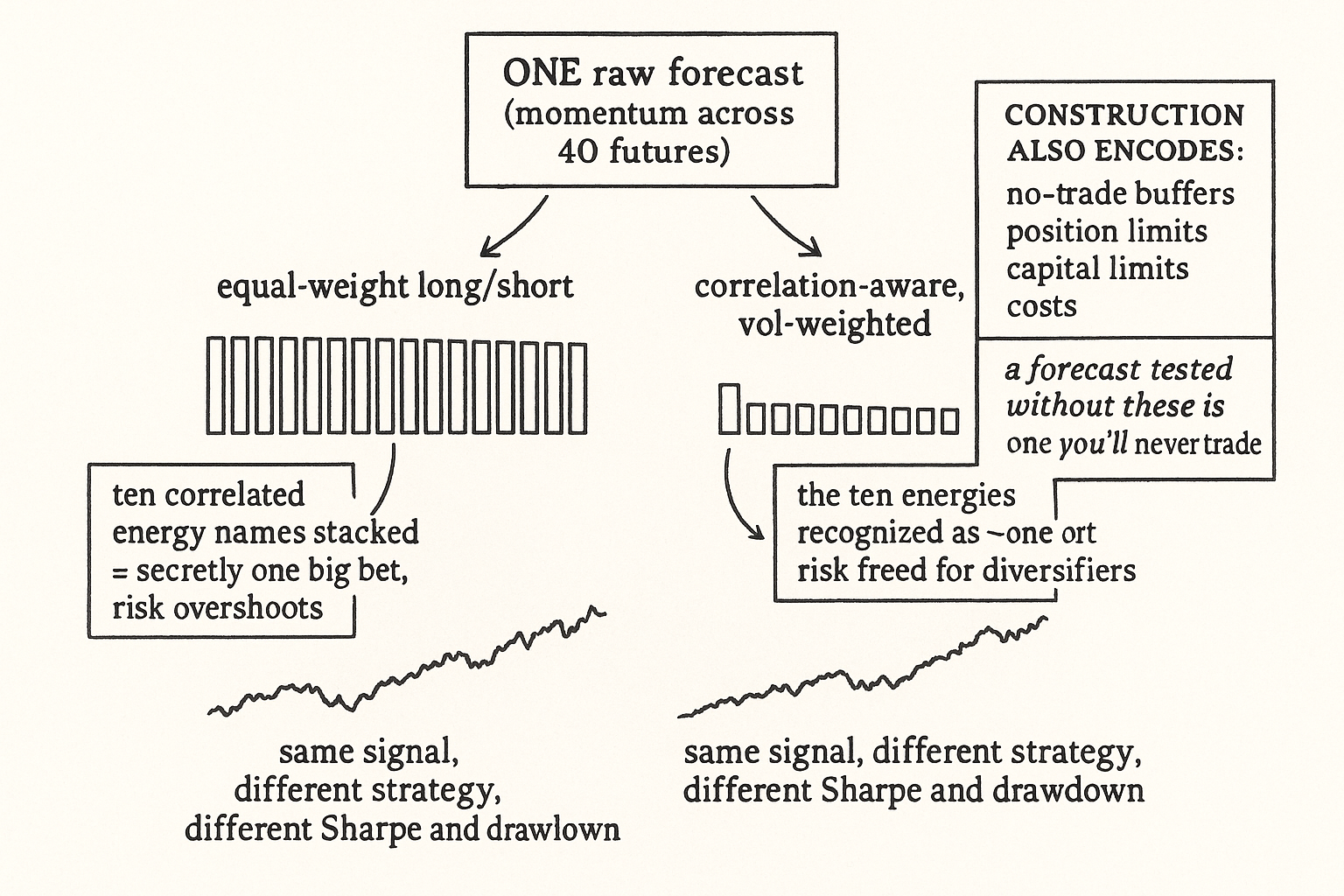

The same forecast, two portfolios, two strategies

Take one forecast: a momentum score across forty futures. Construct it as an equal-weight long/short and you have a diversified momentum strategy whose return is the cross-sectional spread. Construct the identical forecast with volatility weighting and a correlation-aware optimizer and you have shifted risk away from the crowded, correlated names toward the diversifying ones, and your return stream now looks different, often with a higher Sharpe and a different drawdown profile, from the same underlying score. Nothing about the signal changed. The construction changed what the signal expresses, because the construction decided which of the forecast's many bets actually carry size.

This is the part retail skips and the part that separates a backtest from a strategy. You can have a genuinely predictive forecast and destroy it in construction by concentrating risk in a few correlated positions, or by letting one volatile instrument dominate, or by netting two sub-signals that should have been kept separate. The forecast set the direction; the construction set how much of each direction you actually own, and that second decision moves the result as much as the first.

Correlation is where construction earns its keep

The clearest case is correlation. A forecast that says "long ten energy futures" looks like ten bets and is closer to one, because the energy complex moves together, so equal-weighting them stacks ten times the intended risk into a single factor. Construction that accounts for the correlation structure recognizes the ten as nearly one bet and sizes them down accordingly, freeing risk for genuinely independent positions elsewhere. The raw forecast cannot see this; it scores each instrument in isolation. The portfolio step is where the relationships between instruments enter the strategy, and those relationships carry real information about risk that the per-instrument signal never contained.

A proper systematic framework builds this in deliberately by optimizing instrument weights and forecast weights with correlations in view, rather than sizing each position as if it were alone. The weights are not administrative bookkeeping; they are a second model, layered on the first, that says how independent these bets really are. Get the weights wrong and a diversified-looking book is secretly a concentrated one, and the realized risk overshoots the target by the amount of hidden correlation you ignored.

Construction also encodes your costs and constraints

Beyond correlation, construction is where every real-world constraint enters and reshapes the signal. The no-trade buffers from "Cost-Aware Ranking: The Missing Step in Cross-Sectional Strategies" live here, and they change the effective signal by holding stale positions longer than the raw forecast wants. Position limits, capital limits, and gross-exposure caps all live here, and each one bends the realized strategy away from the unconstrained ideal. A forecast tested without these constraints is a forecast you will never actually trade, so the construction layer is where the strategy becomes real and where the difference between the paper return and the live return is decided. Treat construction as part of the research, not as an afterthought bolted on once the signal looks good, because the construction choices are themselves alpha decisions that you can get right or wrong.

Visualizing construction as signal

KEY POINTS

- The line between signal and portfolio is fake. How you combine, weight, and net positions changes what the strategy predicts, so portfolio construction is part of the signal, not downstream plumbing.

- The identical forecast under two constructions becomes two strategies. Equal-weight long/short and a correlation-aware vol-weighted build produce different return streams, Sharpes, and drawdowns from the same score.

- You can have a predictive forecast and destroy it in construction by concentrating risk in correlated names, letting one volatile instrument dominate, or netting sub-signals that should stay separate.

- Correlation is where construction earns its keep. Ten correlated energy futures are closer to one bet than ten; equal-weighting stacks the risk, and correlation-aware sizing frees risk for independent positions.

- Instrument and forecast weights are a second model layered on the first, encoding how independent the bets really are. Get them wrong and a diversified-looking book is secretly concentrated, overshooting the risk target.

- Construction encodes costs and constraints too: no-trade buffers, position limits, capital limits, gross caps. A forecast tested without them is one you will never trade, so treat construction as research, not an afterthought.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Volatility Scaling in Multi-Asset Portfolios

- Target Volatility: Are there Benefits for Domestic and International Equity Investors?

- Cross-Asset Style Premia Allocation

- Measuring the Diversification and Hedging Properties of Correlations

- Strategic Hedge Fund of Fund Portfolio Construction

- The Impact of Regulatory Constraints on Portfolio Risk Estimates

- The Impact of Volatility Targeting

- Behavioral finance factors and investment decisions: A mediating