6.4 Cost-Aware Ranking: The Missing Step in Cross-Sectional Strategies

Ranked systems churn at the slice boundaries, where names flicker across on noise and you pay for each swap. A no-trade buffer holds them, and only net-of-cost performance tells the truth.

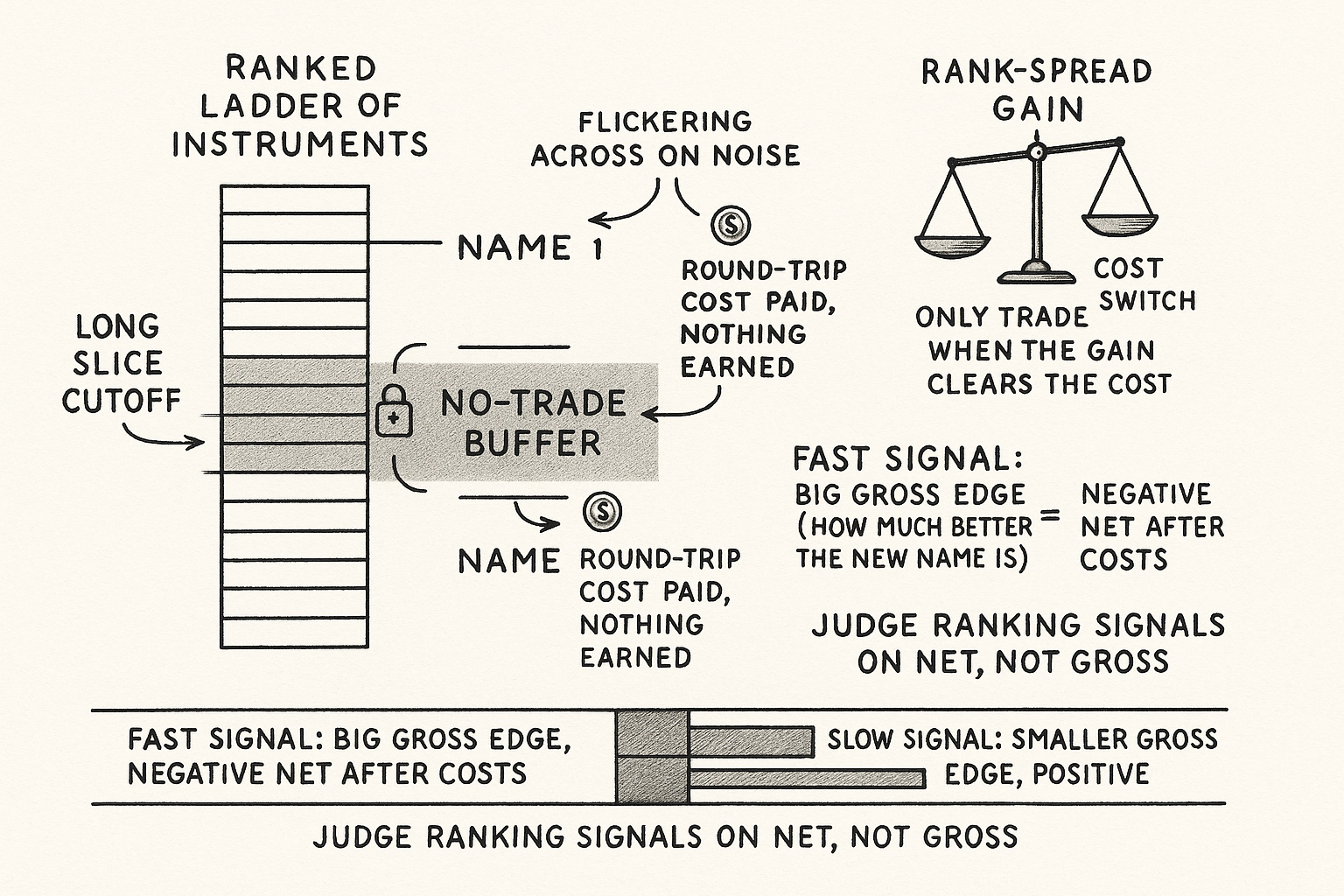

A ranked long/short system has a hidden expense that never shows up in the signal research and wrecks the strategy in production: every time an instrument crosses a slice boundary, you trade. The signal updates, copper slips from rank 3 to rank 5, falls out of your long slice, and now you sell copper and buy whatever climbed into its place. Each of those crossings is a round trip with a cost, and a ranked book that rebalances on every twitch of the ranking can churn its entire portfolio many times over before the spread it was chasing ever pays off. "Ranked Long/Short Systems Explained" built the book; this is the step almost everyone skips when they put it into production.

The turnover is in the boundaries, not the signal

The cost of a ranked system lives at the edges of the slices. Names deep in the long slice or deep in the short slice stay put; the churn comes from the marginal names hovering at the cutoff, flickering in and out as the score wobbles. A signal that reorders the universe gently still produces constant boundary crossings if the cutoff is a hard line, because two names near the threshold will swap rank back and forth on noise alone, and each swap is a pair of trades you pay for and earn nothing from.

$$ \text{net edge}_i = \underbrace{(\hat{r}_i - \hat{r}_{\text{boundary}})}_{\text{rank-spread gain}} - \underbrace{c_i \cdot \Delta w_i}_{\text{cost to switch}} $$

Before you act on a ranking change, compare the gain to the cost. The rank-spread gain is how much better the new name's expected return is than the one it would replace at the boundary; the cost to switch is the per-unit trading cost times the position change the swap requires. If a name is only marginally better than the one already in your slice, the rank-spread gain is small, and the cost to switch eats it. You should only make the trade when the gain clears the cost, which means a name has to be meaningfully better, not trivially better, to justify swapping into it.

The fix: a buffer around the boundary

The practical tool is a no-trade buffer, a band around each slice cutoff where you do nothing. Once a name is in your long slice it stays in until its rank deteriorates past the lower edge of the buffer, not merely past the cutoff itself; a new name only enters once it climbs past the upper edge. The buffer turns the hard boundary into a sticky zone, so the marginal names flickering on noise no longer trigger trades. You give up a little selection sharpness, holding a name a bit longer than the raw ranking would prefer, in exchange for killing the noise-driven turnover that was the real cost.

This is the same logic as a position buffer in a single-instrument system, where you do not adjust a position until it drifts far enough from target to be worth the trade. The wider the buffer, the lower the turnover and the staler the book; the narrower, the fresher and the more expensive. You set the width from the actual cost of trading the universe, not from whatever makes the backtest prettiest, because the buffer is exactly the kind of knob that overfits if you sweep it for performance.

Costs decide which signals are even tradable

Cost-aware ranking changes more than turnover; it changes which signals survive at all. A fast signal that reorders the universe daily might have a real gross edge and a negative net edge once you pay to chase it, while a slower signal with half the gross edge but a tenth the turnover clears costs comfortably. You cannot judge a ranking signal on its gross rank correlation alone. The right test runs the signal through the buffer, charges realistic costs on the trades that survive, and reports the net, because a strategy that looks brilliant before costs and bleeds after them is the most common way a cross-sectional backtest lies to you.

Visualizing cost-aware ranking

KEY POINTS

- A ranked book's hidden cost is turnover. Every time an instrument crosses a slice boundary you trade, and a book that rebalances on every twitch can churn its whole portfolio before the spread pays off.

- The churn lives at the slice boundaries, not in the signal. Marginal names hovering at the cutoff flicker in and out on noise alone, and each swap is a paid round trip that earns nothing.

- Before acting on a ranking change, weigh the rank-spread gain (how much better the new name is) against the cost to switch. Only trade when a name is meaningfully better, not trivially better.

- The fix is a no-trade buffer: a band around each cutoff where you hold. Names stay in until they deteriorate past the band's far edge, and new names enter only once they climb past it, which kills noise-driven turnover.

- Buffer width trades turnover against staleness. Set it from the real cost of trading the universe, not from whatever makes the backtest prettiest, because it overfits if swept for performance.

- Costs decide which signals are tradable at all. A fast signal can have a real gross edge and a negative net edge, so judge ranking signals on net performance after realistic costs through the buffer, never on gross rank correlation.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Optimal multifactor trading under proportional transaction costs

- The Impact of Volatility Targeting

- Trade Strategy and Execution

- Behavioral Finance: Theories and Evidence

- Strategic Hedge Fund of Fund Portfolio Construction

- Trade Sizing Techniques for Drawdown and Tail Risk Control

- Portfolio Construction with LASSO

- Understanding Behavioral Finance Through Biases and Traits of Investors