6.35 Entropy as a Market Concept

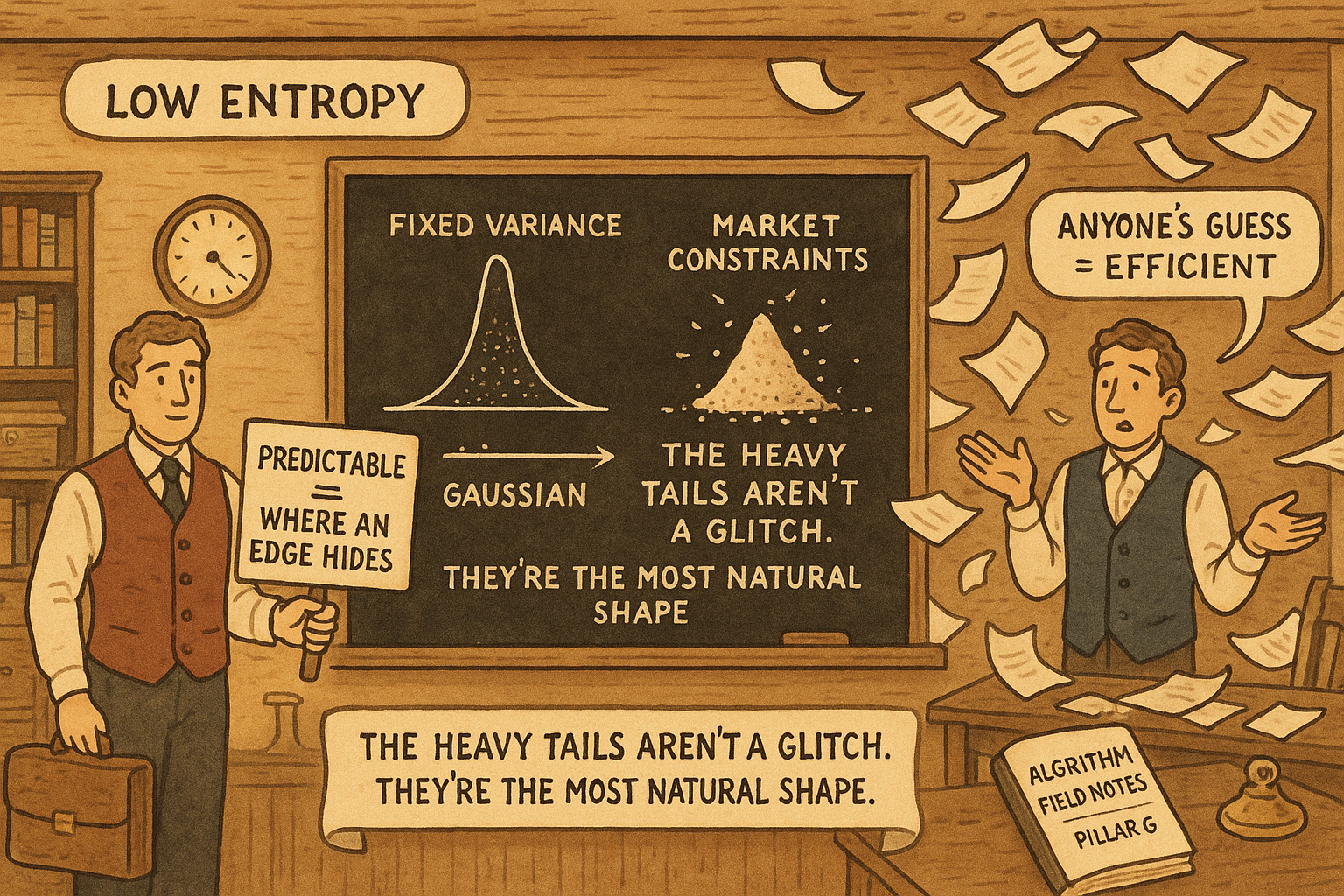

Entropy measures how unpredictable a series is, catching nonlinear structure the variance ratio misses. Maximizing it under market constraints produces fat tails: the tails are natural, not a glitch.

Entropy is a measure of disorder, of how much you do not know about a system, and that makes it a natural fit for markets, where the central problem is uncertainty. Borrowed from physics and information theory, entropy gives you a way to quantify how unpredictable a return series is, how much information a price move carries, and why the fat-tailed distributions from the last two articles show up at all. It is one of the more abstract tools in this pillar, and it pays off concretely: maximizing the right kind of entropy reproduces the heavy tails that the Gaussian misses, which tells you the tails are not an anomaly but the most natural state of a system under the constraints markets impose. "Lévy Distributions and Market Extremes" left us needing a reason the tails are fat; entropy supplies it.

Entropy measures what you cannot predict

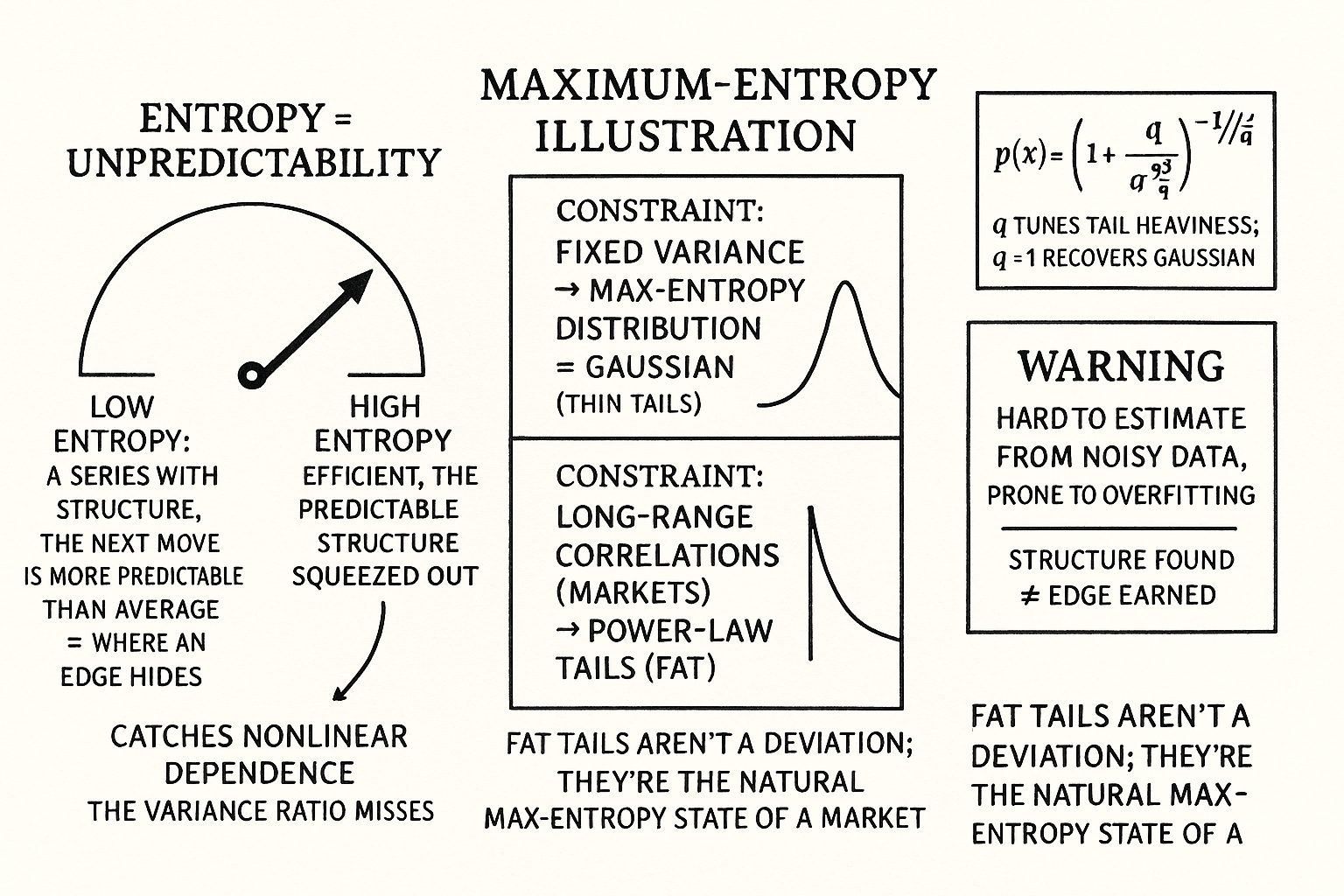

In information theory, entropy measures the average surprise of an outcome. A coin that always lands heads has zero entropy, because every flip is certain and carries no information. A fair coin has maximum entropy for two outcomes, because each flip is maximally surprising. Applied to returns, entropy quantifies how much uncertainty remains about the next move given what you know: a perfectly predictable series has low entropy, and a series where the next return is anyone's guess has high entropy. This reframes the efficient-market question from this pillar in physical terms, an efficient market is a high-entropy one where prices have squeezed out the predictable structure, and an edge is a pocket of lower-than-expected entropy, a place where the next move is more predictable than the market average.

The appeal of entropy over the autocorrelation-based tools like the variance ratio is that it captures nonlinear dependence. The variance ratio sees linear autocorrelation; a series can have zero linear autocorrelation and still be predictable through a nonlinear relationship, and entropy-based measures can detect that structure where a variance ratio reports randomness. So entropy is a more general detector of predictability, catching dependencies that the linear tools miss, at the cost of being harder to estimate and interpret.

Why maximum entropy gives fat tails

The deeper use of entropy explains where the heavy tails come from. The maximum-entropy principle says that, given some constraints on a system, the least-biased distribution to assume is the one with the highest entropy consistent with those constraints, because it assumes nothing beyond what the constraints force. Under the constraint of a fixed variance, the maximum-entropy distribution is the Gaussian, which is why the bell curve is everywhere. But markets are not constrained by a simple fixed variance; they have long-range correlations and the anomalous behavior of "Anomalous Diffusion in Financial Markets", and under those richer constraints the maximum-entropy distribution changes.

$$ S_q = \frac{1 - \sum_i p_i^{\,q}}{q - 1} $$

The Tsallis entropy generalizes the ordinary entropy with a parameter q that controls how much weight the measure puts on rare events. When q is 1 it reduces to the standard entropy, whose maximization under fixed variance gives the Gaussian. When q is not 1, maximizing the entropy produces distributions with power-law tails, the fat-tailed shapes that actually fit market returns. The parameter q tunes the tail heaviness, and the value that fits the data tells you how far the market sits from the simple Gaussian regime. The fat tails, in this light, are not a deviation from a natural order; they are the natural maximum-entropy state of a system with the kind of long-range structure markets have, which is why every thin-tailed model keeps failing against them.

What entropy buys you, and what it does not

The practical value of entropy is as a measurement of predictability and a justification for taking the tails seriously, not as a strategy in itself. As a measurement, an entropy estimate on a return series tells you whether there is exploitable structure, including the nonlinear structure the variance ratio cannot see, and a series whose entropy is meaningfully below the random benchmark is one worth investigating for an edge. As a justification, the maximum-entropy result explains why fat tails are unavoidable and stable, which reinforces every survival argument in this pillar: the tails are baked into the system, not a passing feature you can wait out.

The honest limits are real. Entropy is hard to estimate from finite, noisy financial data, because it requires estimating a whole distribution, and the estimate is sensitive to how you bin the data and how much data you have, so an entropy edge measured in-sample is as prone to overfitting as any other, maybe more, given the estimation difficulty. Low entropy tells you structure exists; it does not tell you the structure is tradable after costs or that it will persist, the same caveats that apply to every signal here. And the Tsallis machinery, while it fits the data, is a description, not a mechanism, it tells you the distribution that emerges, not why the market produces those constraints. Use entropy to detect nonlinear predictability and to understand why the tails are permanent, and keep the same skepticism you apply to every other measurement: a structure found is not yet an edge earned.

Visualizing entropy

KEY POINTS

- Entropy measures disorder, the average surprise of an outcome, so it quantifies how unpredictable a return series is. A predictable series has low entropy; one where the next move is anyone's guess has high entropy.

- In entropy terms, an efficient market is high-entropy with the predictable structure squeezed out, and an edge is a pocket of lower-than-expected entropy where the next move is more predictable than average.

- Entropy captures nonlinear dependence that the variance ratio misses. A series with zero linear autocorrelation can still be predictable, and entropy-based measures detect it, at the cost of being harder to estimate.

- The maximum-entropy principle says to assume the highest-entropy distribution consistent with the constraints. Under fixed variance that is the Gaussian; under the long-range correlations markets have, it changes.

- Tsallis entropy generalizes the standard measure with a parameter q that weights rare events. Maximizing it for q not equal to 1 produces the power-law fat tails that fit real returns, so the tails are the natural max-entropy state, not a deviation.

- Entropy is a measurement and a justification, not a strategy. It is hard to estimate from noisy data and prone to overfitting, and low entropy means structure exists, not that it is tradable after costs or will persist.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- The Maximum-Entropy Distribution of the Future Stock Price

- A New Method of Employing the Principle of Maximum Entropy to Retrieve the Risk Neutral Density of Future Stock Prices

- Incorporating Fat Tails in Financial Models Using Entropic Divergence Measures

- Modeling Heavy Tails with Tsallis Entropy and Adaptive KDE

- Maximum Entropy Production Principle for Stock Returns

- Rao’s Quadratic Entropy and Maximum Diversification Indexation

- Minimum Variance Portfolios with Enhanced Stability (entropy-related measures vs correlation-based measures)

- An Essay on Frictions in Stochastic Portfolio Theory (energy–entropy portfolios)