6.38 The Three Stages of a Trading Idea: Absurd, Familiar, Inevitable

Trading ideas go absurd, familiar, inevitable; the edge is largest at absurd, gone at inevitable. Hunt in uncomfortable places but verify ruthlessly, because most absurd ideas are wrong, not early.

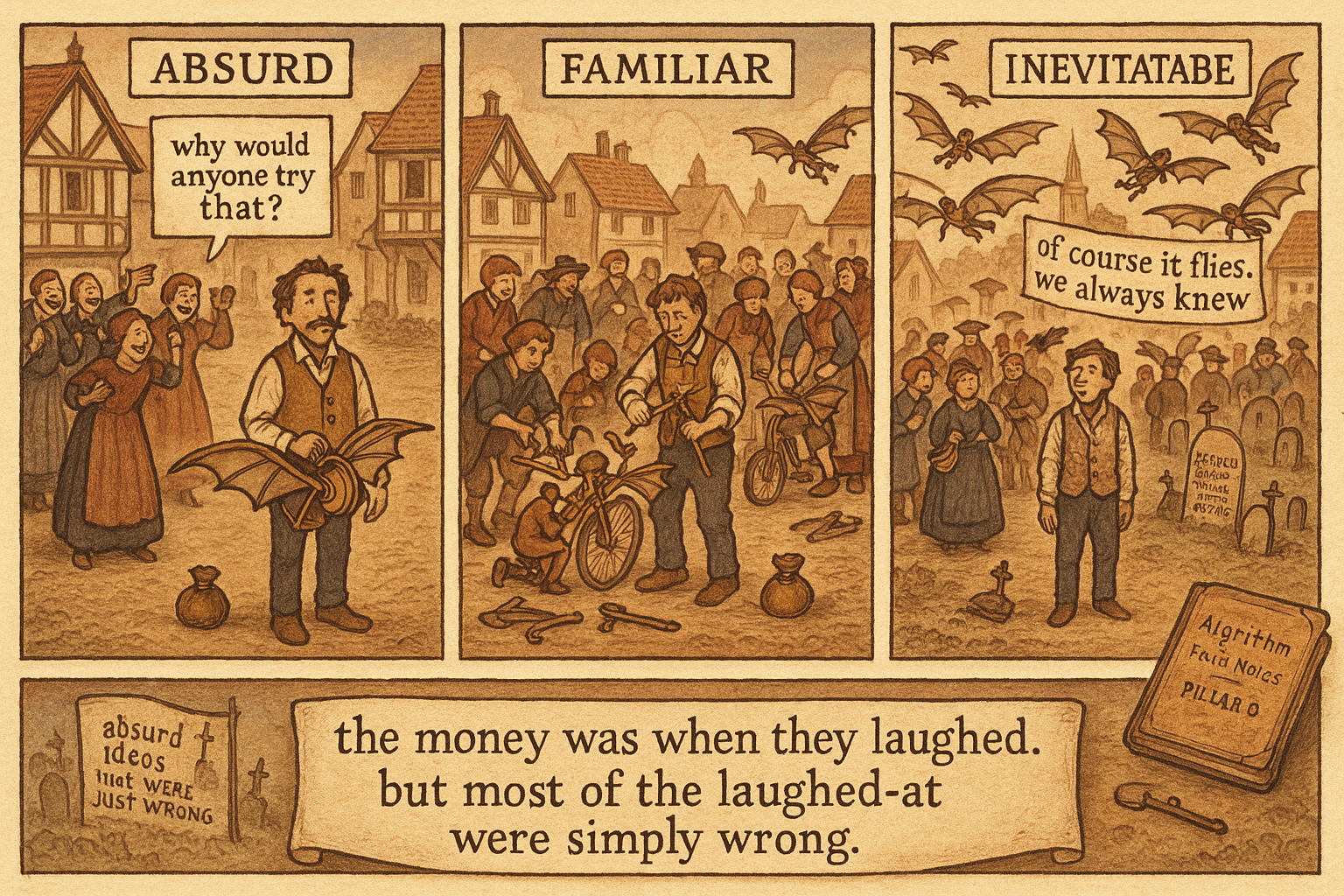

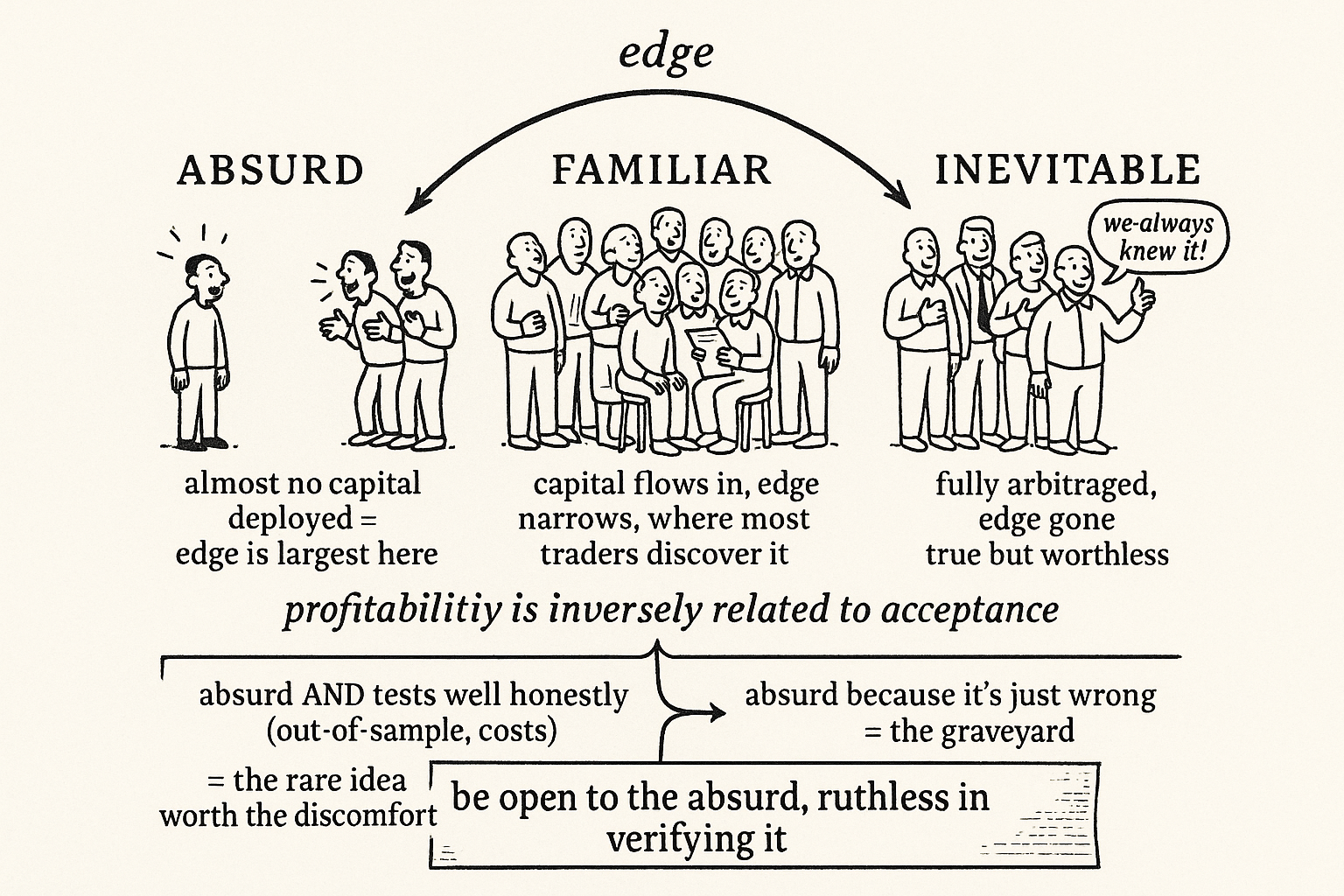

Every trading idea that ever made money passed through three stages. First it sounded absurd, so strange that people wondered why anyone would suggest it. Then it became familiar, as evidence accumulated and the idea entered the conversation. Finally it became inevitable, so obvious in hindsight that everyone agreed they always knew it. The cruel part for a trader is that the money is in the first stage, and by the third stage the edge is gone, competed away by the same consensus that made the idea obvious. Understanding this arc tells you where to hunt and why the comfortable, well-accepted ideas are the worst place to look. This sits near the end of the pillar because it reframes the whole enterprise: the goal is to find ideas while they are still absurd.

The arc of an idea

Stage one is absurdity. A new idea about how markets work, that price increments are not independent, that a physical diffusion model describes returns, that you should rank instruments rather than forecast them, lands as nonsense to the established view, because it contradicts what everyone knows. The reaction is dismissal: that cannot be right, why would anyone think that. The idea has almost no adherents, no respectability, and, crucially, almost no capital deployed against it, which is precisely why the edge is largest here. The inefficiency the idea exploits is wide open, because the consensus has not only failed to close it, it denies the inefficiency exists.

Stage two is familiarity. Evidence accumulates, a few practitioners demonstrate the idea works, papers appear, and the idea moves from absurd to plausible to discussed. More capital flows in as the respectability grows, and the edge begins to narrow, because each new entrant trades away a piece of the inefficiency. The idea is still profitable here but less so than at stage one, and the window is closing as familiarity spreads. This is where most traders discover an idea, which is the problem: by the time something is familiar enough to find easily, the easy money has already been taken.

Stage three is inevitability. The idea is now obvious, taught, assumed, built into everyone's models. In hindsight it seems absurd that anyone ever doubted it, and that universal acceptance is exactly what kills the edge, because when everyone trades an idea the inefficiency it exploited is fully arbitraged and the returns vanish. The idea is true, more established than ever, and worthless as a source of edge, because being right is not the same as being early, and at stage three everyone is right together.

The money is in the discomfort

The arc has a brutal implication: the profitability of an idea is inversely related to its acceptance. The maximum edge sits at maximum absurdity, when the idea is most uncomfortable to hold and most likely to make you look foolish, and the edge decays monotonically as the idea gains acceptance. This is the structural reason that comfortable, consensus ideas do not pay, the ones everyone agrees on are at stage three, fully priced, and the only ideas with real edge are the ones that still feel wrong, that you can barely defend at a dinner party without being laughed at.

This connects to the discipline premium from "The Discipline Premium in Trading", but at the level of ideas rather than execution. Just as the discipline premium pays you for tolerating the discomfort of following rules, the absurdity premium pays you for tolerating the discomfort of holding a view the consensus rejects. Both are paid for enduring something unpleasant that most people will not endure, and both are durable for the same reason: human nature reliably avoids discomfort, so the supply of people willing to hold absurd-but-correct ideas stays small. The trader hunting for edge should be uncomfortable, because comfort means consensus and consensus means stage three.

The trap: most absurd ideas are just wrong

The arc is seductive and the seduction is dangerous, because it can be read as a license to believe any absurd idea, on the theory that absurdity signals edge. It does not. The overwhelming majority of absurd ideas are absurd because they are wrong, not because they are early, and the graveyard of trading is full of people who held a ridiculous view to the end, convinced they were at stage one of a three-stage arc that was actually a one-stage delusion. Absurdity is necessary for a large edge and nowhere near sufficient, and distinguishing the absurd-but-correct idea from the merely-absurd one is the entire difficulty, the thing that no framework solves for you.

What separates the two is evidence, held to the same standard as everything else in this pillar. An absurd idea worth trading is one that is absurd to the consensus and supported by the data when you test it honestly, with out-of-sample validation, cost accounting, and the skepticism about overfitting that every signal demands. The arc tells you to look in uncomfortable places and to take seriously an idea that tests well even though it sounds wrong; it does not tell you to abandon the testing because the idea is exciting. The discipline is to be open to the absurd and ruthless in verifying it, holding the contrarian idea and the rigorous test at the same time, because the absurd idea that survives honest testing is the rare one worth the discomfort, and the absurd idea that you believe because it is absurd is just a bias wearing a contrarian costume.

Visualizing the three stages

KEY POINTS

- Every profitable trading idea passes through three stages: absurd (people wonder why anyone would suggest it), familiar (evidence accumulates), and inevitable (obvious in hindsight). The money is in the first stage.

- At the absurd stage the idea has almost no capital deployed against it, so the inefficiency is wide open and the edge is largest, precisely because the consensus denies the inefficiency exists.

- At the familiar stage capital flows in and the edge narrows. Most traders discover an idea here, which is the problem: by the time it is easy to find, the easy money is taken.

- At the inevitable stage universal acceptance fully arbitrages the inefficiency, so the idea is more established than ever and worthless as edge. Being right is not the same as being early.

- Profitability is inversely related to acceptance. The maximum edge sits at maximum absurdity, when the idea is most uncomfortable to hold, which is the structural reason consensus ideas do not pay.

- The trap is that most absurd ideas are wrong, not early. Absurdity is necessary for a large edge and nowhere near sufficient, so be open to the absurd and ruthless in verifying it with honest out-of-sample, cost-aware testing.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Target Volatility: Are there Benefits for Domestic and International Equity Investors?

- Volatility Scaling in Multi-Asset Portfolios

- Strategic Hedge Fund of Fund Portfolio Construction

- Capital Market Efficiency and Arbitrage Efficacy

- Market Efficiency with Costly Information

- Modern Machine Learning Tools in Finance: A Critical Perspective

- The Impact of Volatility Targeting

- Four Strategies, 562 Trades, Zero Edge