6.24 Why Traders Take Profits Too Early and Losses Too Late

Selling winners early and holding losers late is one asymmetry: prospect theory makes you risk-averse in gains and risk-seeking in losses, inverting a positive-skew edge into the blow-up shape.

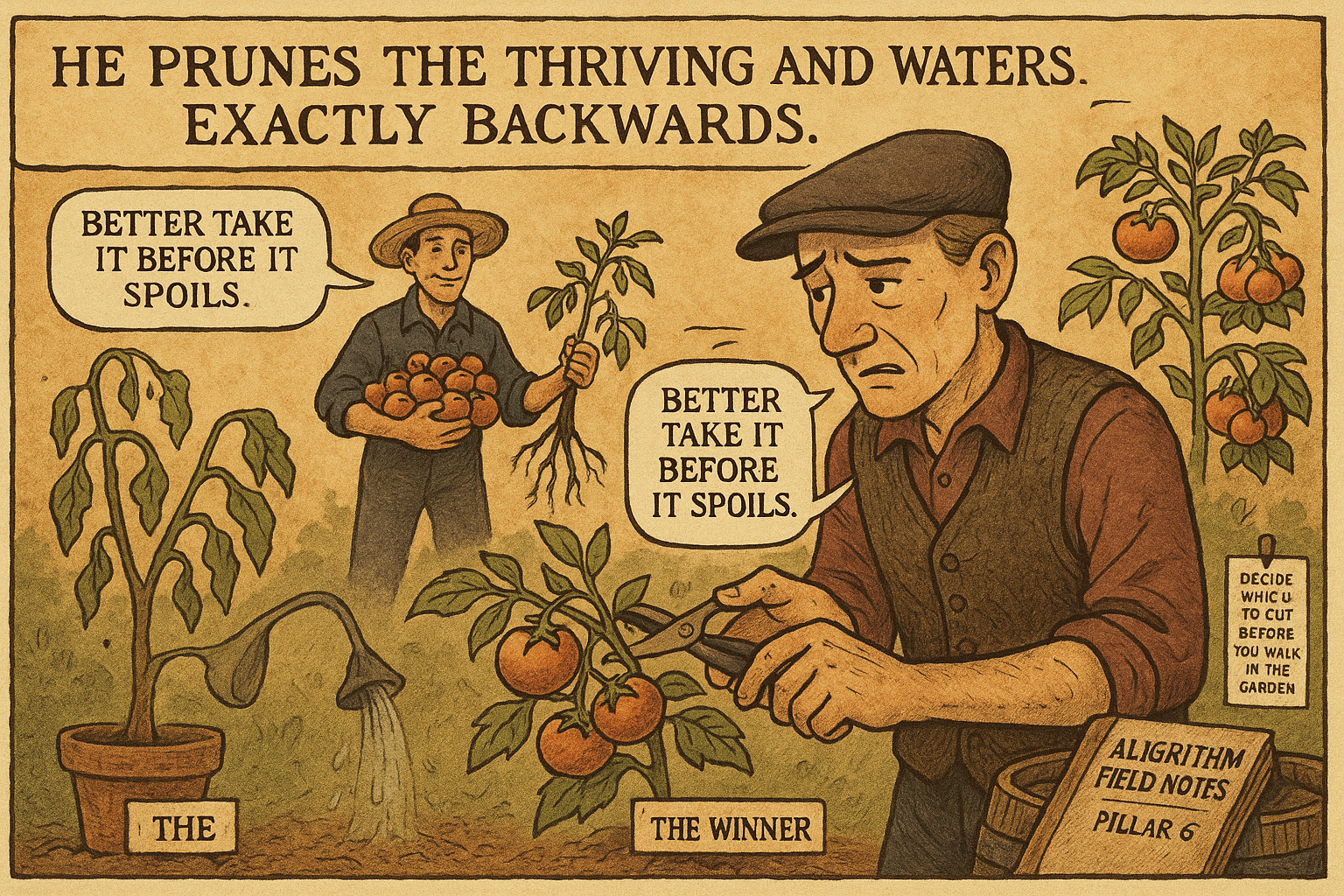

The same trader does two opposite things with winners and losers, and both are wrong. He grabs a small profit the moment it appears, terrified it will evaporate, and he clings to a loss long after it should have been cut, certain it will come back. Sell the winners early, ride the losers late: the disposition effect, and it is the exact reverse of the rule that makes money, which is to cut losses and let winners run. The disposition effect is not two separate mistakes; it is one asymmetry in how the brain treats gains and losses, producing two symmetric errors. "Get-Even-Itis: The Most Expensive Disease in Trading" covered the losing half; this is the full pattern and why it flips your edge upside down.

One asymmetry, two errors

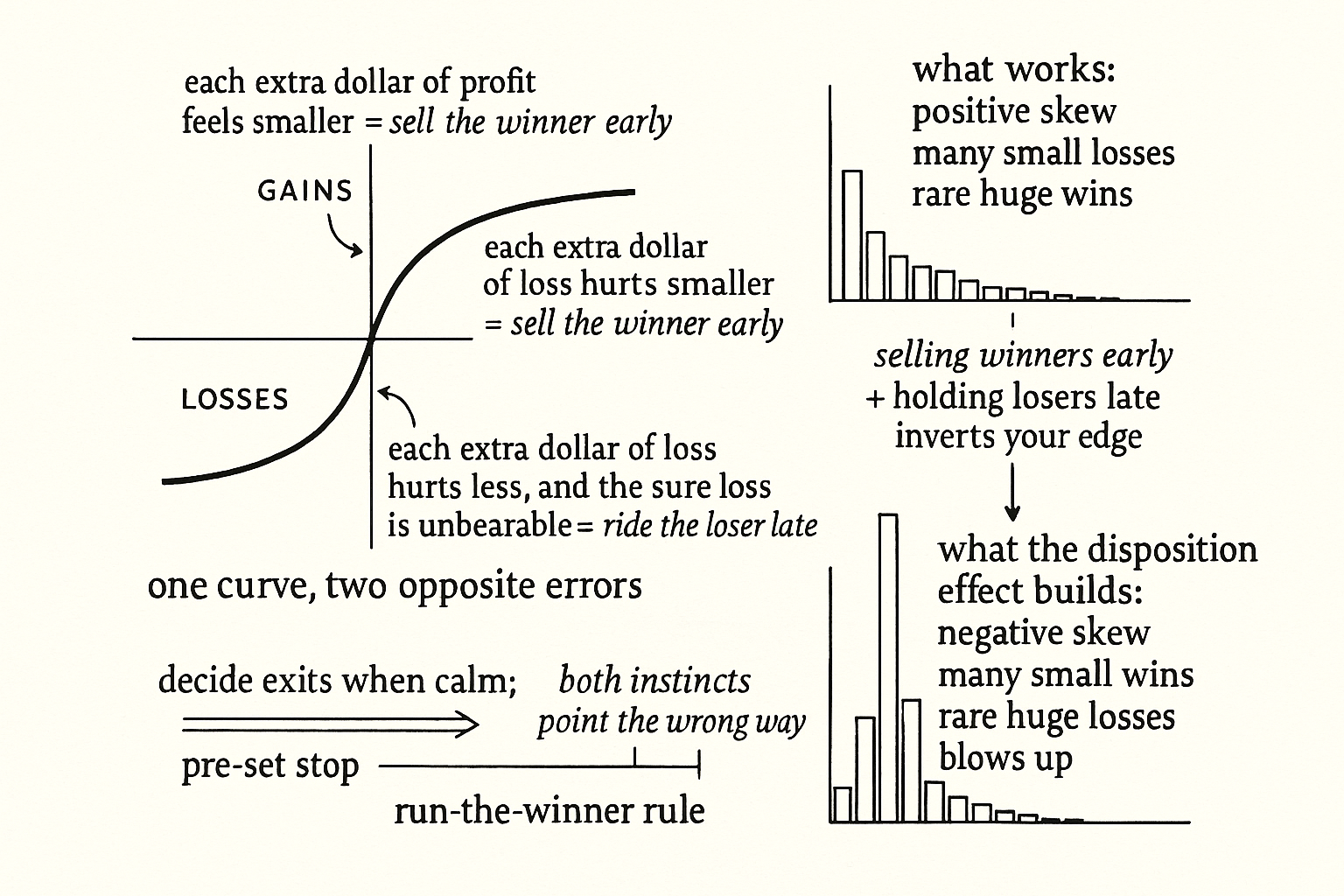

Prospect theory explains both halves with a single curved value function. In the domain of gains, people are risk-averse: a sure gain is preferred to a gamble with a higher expected value, because the pleasure of gains diminishes as they grow, so a bird in the hand beats two in the bush. In the domain of losses, people flip to risk-seeking: a sure loss is rejected in favor of a gamble that might avoid the loss entirely, because the pain of losses also diminishes with size, so a certain small loss feels worse than a coin-flip at a larger one.

$$ v(x) = \begin{cases} x^{\alpha} & x \geq 0 \quad (\text{gains: concave, risk-averse}) \\ -\lambda(-x)^{\beta} & x < 0 \quad (\text{losses: convex, risk-seeking, } \lambda > 1) \end{cases} $$

The value function bends differently above and below the reference point. For gains it is concave, so each additional dollar of profit feels less exciting than the last, which makes you want to lock in the sure thing and sell the winner. For losses it is convex and steeper, the steepness making losses loom larger and the curvature making each additional dollar of loss hurt less than the first, which makes you willing to gamble on the loser recovering rather than accept the certain loss. The same curvature that sells winners early holds losers late. It is one shape producing both errors.

This is exactly backwards from what works

The disposition effect flips the rule that actually generates returns. Profitable trading, especially trend following, depends on a few large winners paying for many small losers, the positive-skew payoff from "Why Percent Profitable Is Overrated". That payoff requires letting winners run far past the point where the bird-in-the-hand instinct screams to sell, and cutting losers fast, before the get-even instinct can talk you into holding. The disposition effect does the precise opposite: it amputates the large winners before they grow large, destroying the right tail that the whole strategy depends on, and it lets the small losers grow into large ones, fattening the left tail you were trying to keep thin.

A trader running on the disposition effect inverts his own edge. He turns a positive-skew strategy, many small losses and rare huge wins, into a negative-skew one, many small wins and rare huge losses, which is the shape that blows up accounts. Every time he sells a winner early he caps a gain; every time he holds a loser late he uncaps a loss; and the sum of those two habits is a system engineered to lose, built on top of signals that might have won.

You cannot feel your way out of it

The disposition effect is not a discipline problem you solve by trying harder, because the asymmetry operates below conscious control and feels like prudence from the inside. Selling a winner feels responsible, taking the profit, not being greedy. Holding a loser feels patient, giving the trade room, not panicking. Both feel like virtues, which is why willpower fails: you are not fighting an obvious vice, you are fighting an instinct that has disguised itself as good judgment.

The fix is mechanical. Set exits by rule before the trade, both the stop that cuts the loser and the logic that lets the winner run, so neither decision is made in the moment when the asymmetry is loudest. A disciplined framework does this by forbidding changes to a forecast once a bet is open, because the urge to take the profit or give the loser room is the disposition effect, and the only reliable defense is to have decided the exits when you were calm and then refuse to override them. Let the rule run the winner past your comfort and cut the loser against your hope, because your comfort and your hope are the two signals pointing exactly the wrong way.

Visualizing the disposition effect

KEY POINTS

- Traders sell winners too early and hold losers too late, the disposition effect, which is the exact reverse of the rule that makes money: cut losses, let winners run.

- Both errors come from one asymmetry. Prospect theory's value function is concave in gains (risk-averse, so you lock in the sure profit) and convex and steeper in losses (risk-seeking, so you gamble on the loser recovering).

- The same curvature that sells winners early holds losers late. It is one shape producing two symmetric errors, not two separate problems.

- This inverts the payoff that profitable trading depends on. Trend following needs a few large winners paying for many small losers, and the disposition effect amputates the winners and fattens the losers.

- A trader on the disposition effect turns a positive-skew strategy into a negative-skew one, the shape that blows up accounts, on top of signals that might have won.

- Willpower fails because selling winners feels responsible and holding losers feels patient. Both feel like virtues. Set exits by rule before the trade and refuse to override them, because your comfort and hope point the wrong way.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- A Position-Aware Trading Agent System for Real Financial Markets

- Harvesting the FX skew premium

- System Design and Testing

- Trends in Quantitative Finance

- Spurious Predictability in Financial Machine Learning - arXiv

- Enhancing Systematic Trend-Following Using Network Momentum

- A Profitable Day Trading Strategy For The US Equity Market

- Machine Learning Enhanced Multi-Factor Quantitative Trading - arXiv