6.37 Why Financial Markets Are Complex Systems

A market is a complex system where crashes emerge from millions of decisions, leaving power-law fingerprints. Fat tails and clustering are permanent; the lens explains markets, it can't time them.

A market is not a machine with a few dials you can turn to predict its output, and it is not a casino where every spin is independent. It is a complex system, a large collection of interacting agents whose collective behavior produces patterns that no individual agent intended and no simple equation captures. Calling markets complex is not hand-waving; it is a specific claim with testable consequences, the power-law distributions, the clustering of volatility, the crashes that behave like avalanches, all of which follow from the structure of a complex system and none of which fit the tidy random-walk picture. This pulls together the fat tails, the anomalous diffusion, and the entropy of the preceding articles into one frame, because they are all symptoms of the same complex-systems nature.

Emergence: the whole is not the sum

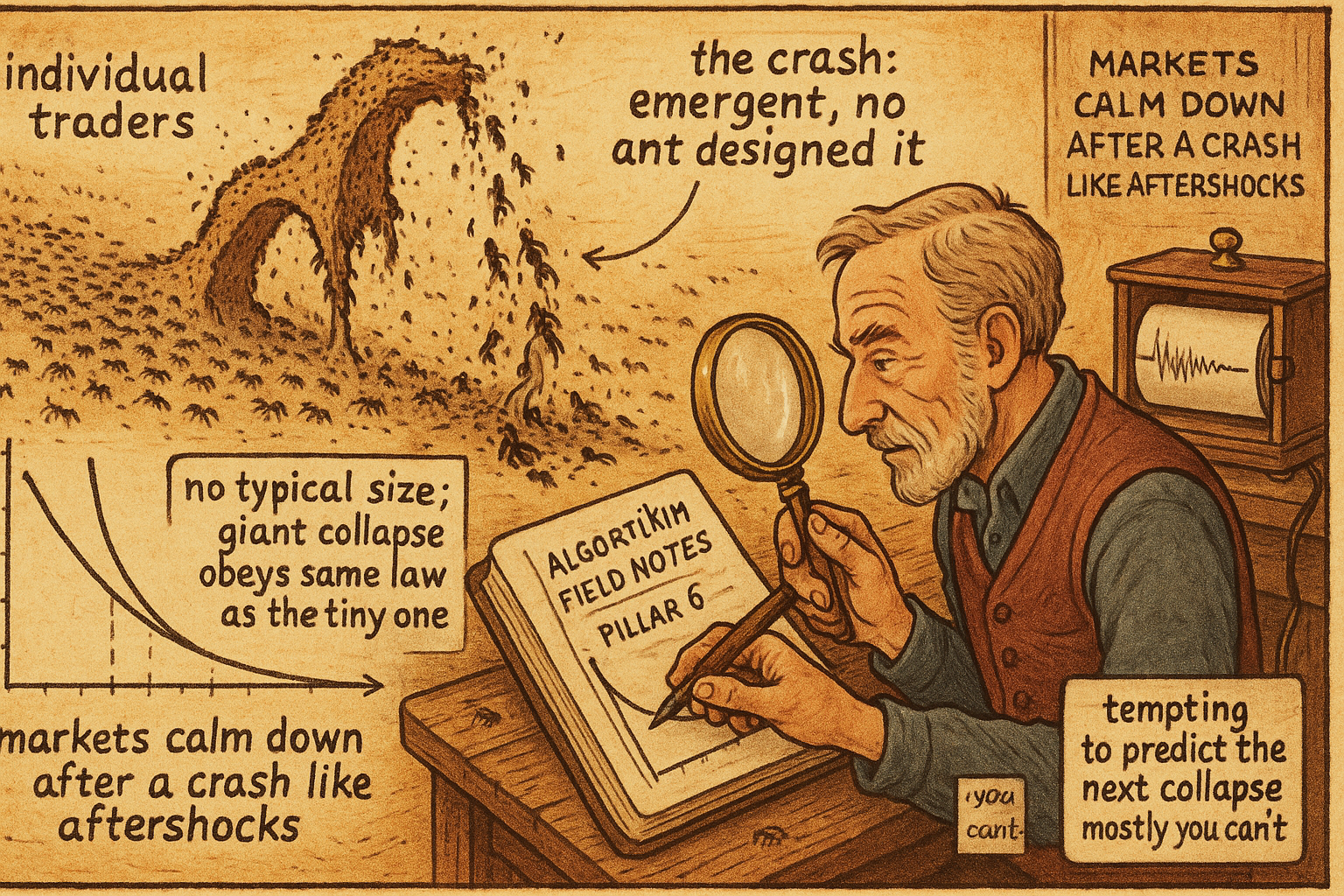

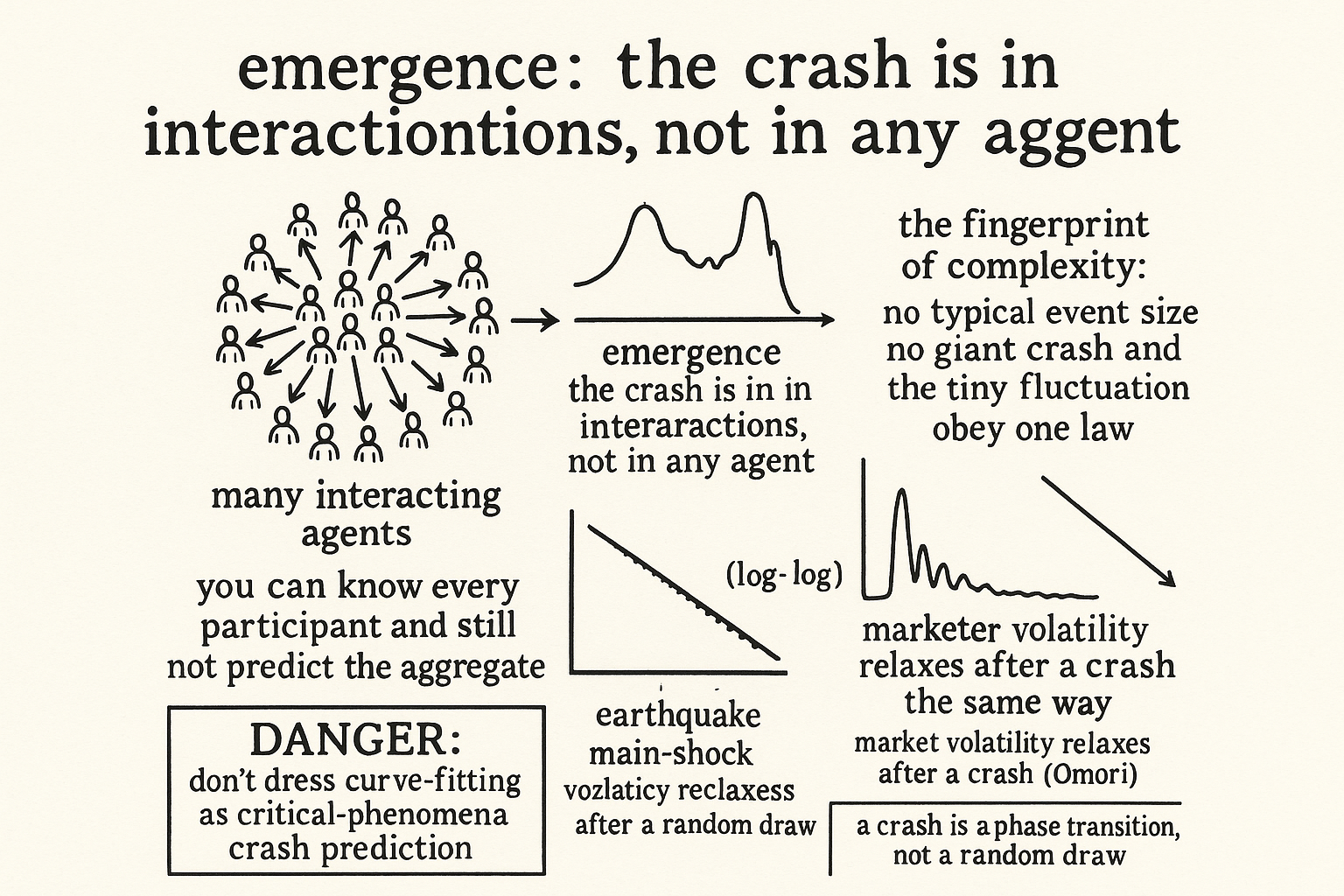

The defining feature of a complex system is emergence, where the interactions between many simple components produce collective behavior that you cannot predict from the components alone. No single trader decides the market will crash; the crash emerges from millions of individual decisions, each locally reasonable, interacting through prices and feedback loops into a collective cascade. This is why reductionism fails on markets: you can understand every participant's strategy perfectly and still not predict the aggregate, because the behavior lives in the interactions, not in the parts. The herding from the behavioral articles in this pillar is a microscopic input; the emergent output is a price bubble, and the bubble has properties the individual herding instinct does not.

Emergence explains why markets resist the clean models that work in physics-with-few-bodies. A complex system has too many interacting degrees of freedom and too much feedback to collapse into a simple law, and the attempts to force one, the Gaussian returns, the efficient-market equilibrium, the single fitted distribution, all break on the parts of behavior that emerge from the interactions rather than from the average agent. The fat tails of "Fat Tails: Why Gaussian Thinking Breaks Trading Systems" are emergent: they come from the way agents' decisions correlate and cascade, not from any single agent's return distribution.

Power laws are the fingerprint of complexity

Complex systems leave a characteristic signature, and it is the power law. Across wildly different complex systems, earthquakes, avalanches, city sizes, word frequencies, the distribution of event sizes follows a power law, where events occur with a frequency proportional to their size raised to a negative power, so there is no typical scale and the rare giant event is a natural part of the same distribution as the common small ones. Markets show this fingerprint everywhere: the distribution of price moves, the distribution of trade sizes, the distribution of drawdowns. The power law is why the fat tail exists, why there is no characteristic size of a crash, and why the same statistical law governs a tiny fluctuation and a market-wide collapse.

The earthquake analogy runs deep enough to be useful. After a large earthquake, aftershocks follow the Omori law, their rate decaying as a power of the time since the main shock, and market volatility after a crash relaxes the same way, with elevated turbulence decaying as a power law rather than snapping back to calm. Some researchers go further, proposing that crashes have a precursor signature, a log-periodic oscillation superimposed on a power-law acceleration as the system approaches a critical point, the bubble building toward a most-probable crash time. Whether or not that specific signature is reliably tradable, the framing matters: a crash is a critical phenomenon, a phase transition in a complex system, not a random bad draw, which is a completely different thing to prepare for than a Gaussian tail event.

What complexity means for a trader

The complex-systems view is a stance, not a strategy, and the stance has concrete consequences for how you trade. It tells you to expect the fat tails and the volatility clustering as permanent structural features rather than anomalies, which reinforces every survival argument in this pillar: the catastrophes are built into the system's nature, so you size for them always. It tells you that the structure you exploit, the trending, the reversion, emerges from agent interactions that can shift when the agents or their incentives change, which is why edges decay and systems die, the subject of "When to Switch Off a Trading System". And it tells you that prediction has hard limits, because emergence means the aggregate is not deducible from the parts, so the honest goal is not to forecast the complex system but to find the statistical regularities it throws off and harvest them while they last.

The danger of the complex-systems framing is the opposite of the Gaussian one, and worth naming. Where Gaussian thinking lulls you into ignoring the tail, complexity thinking can seduce you into over-claiming, dressing ordinary curve-fitting in the language of critical phenomena and log-periodic precursors to sell a crash-prediction model that does not work out of sample. The same skepticism applies here as everywhere in this pillar: the complex-systems lens is valuable for understanding why markets behave as they do and why the tails are permanent, and it is not a license to believe you can time the next crash because you fit a power law to the last one. Use it to respect the system's nature, not to claim mastery over it.

Visualizing markets as complex systems

KEY POINTS

- A market is a complex system: many interacting agents whose collective behavior produces patterns no individual intended and no simple equation captures. This is a specific, testable claim, not hand-waving.

- The defining feature is emergence. A crash emerges from millions of locally reasonable decisions interacting through feedback, so you can understand every participant and still not predict the aggregate, because the behavior lives in the interactions.

- Emergence is why clean models break on markets. The fat tails are emergent, coming from how agents' decisions correlate and cascade, not from any single agent's return distribution.

- Power laws are the fingerprint of complexity. Price moves, trade sizes, and drawdowns all follow them, so there is no typical event size and the rare crash belongs to the same distribution as the common fluctuation.

- A crash behaves like a critical phenomenon, a phase transition. Volatility after a crash relaxes as a power law like earthquake aftershocks, which is a different thing to prepare for than a Gaussian tail event.

- The view is a stance, not a strategy: expect fat tails and clustering as permanent, expect edges to decay as agents shift, and accept hard limits on prediction. The danger is over-claiming, dressing curve-fitting as crash prediction, so respect the system rather than claiming to time it.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Power-Law Distribution in Venture Capital Returns and Its Implications for Portfolio Construction

- Stochastic Volatility as a Simple Generator of Financial Power-Laws and Scale Invariance

- The Power Law and Dividend Yields

- Optimal CVaR Portfolio Construction Under Power Law Stochastic Walks

- Cross-Sectional Variation of Risk-Targeting Option Portfolios

- Yet Another Analysis of the S&P 500 At-the-Money Skew

- Power-law ansatz in complex systems: excessive loss of information

- Trade clustering and power laws in financial markets - Nirei - 2020