9.28 Adverse Selection Is Adverse Selection: Porting Fast-Fills-Are-Bad-Fills to FX and Futures

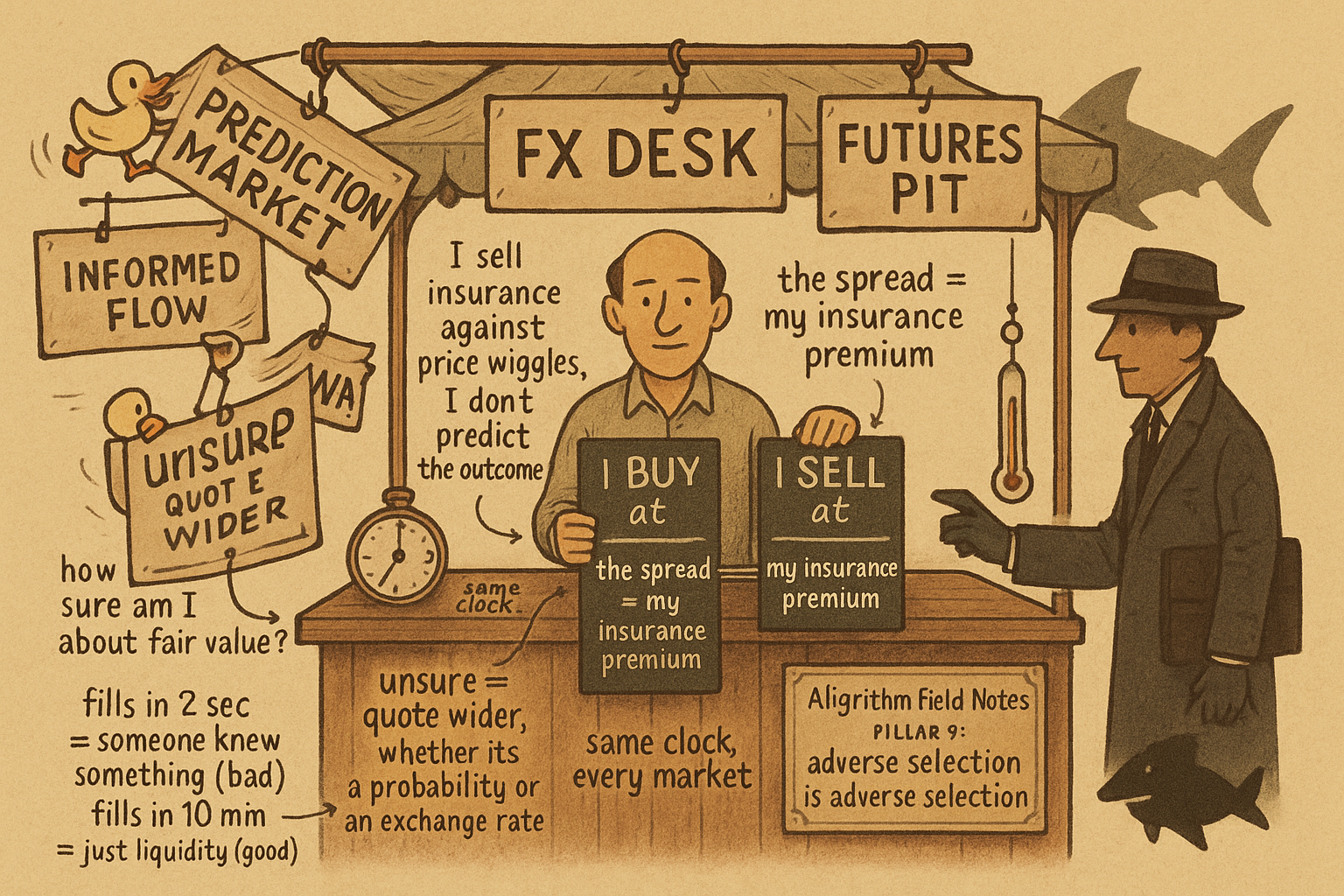

Fill quality, the maker's profit equation, and the markout test move from a Polymarket CLOB to an FX or futures book unchanged. The payoff structure differs; adverse selection is adverse selection.

Your limit order fills in two seconds and you feel quick. On Polymarket that fast fill means the market ran through your price toward something you will not like. On EURUSD it means the same thing. On a bund future it means the same thing. The counterparty who took your resting order was faster to the news or knew more, and the speed of the fill is the tell in every market with an order book, because adverse selection is a property of who chooses to trade against you, not of what the contract pays at the end.

The article "Fast Fills Are Bad Fills" made this case for prediction markets, where the contract pays a dollar or zero and the information asymmetry is sharp. The old article "Adverse Selection Explained for Traders" made the general case for order books before that. This is the bridge: the same fill-quality metric, the same market-making profit equation, and the same markout diagnostic move between a Polymarket CLOB and an FX or futures book without changing a symbol.

Fill quality: one metric, every book

When your order fills, someone took the other side. Ask why, and measure the answer with a single ratio.

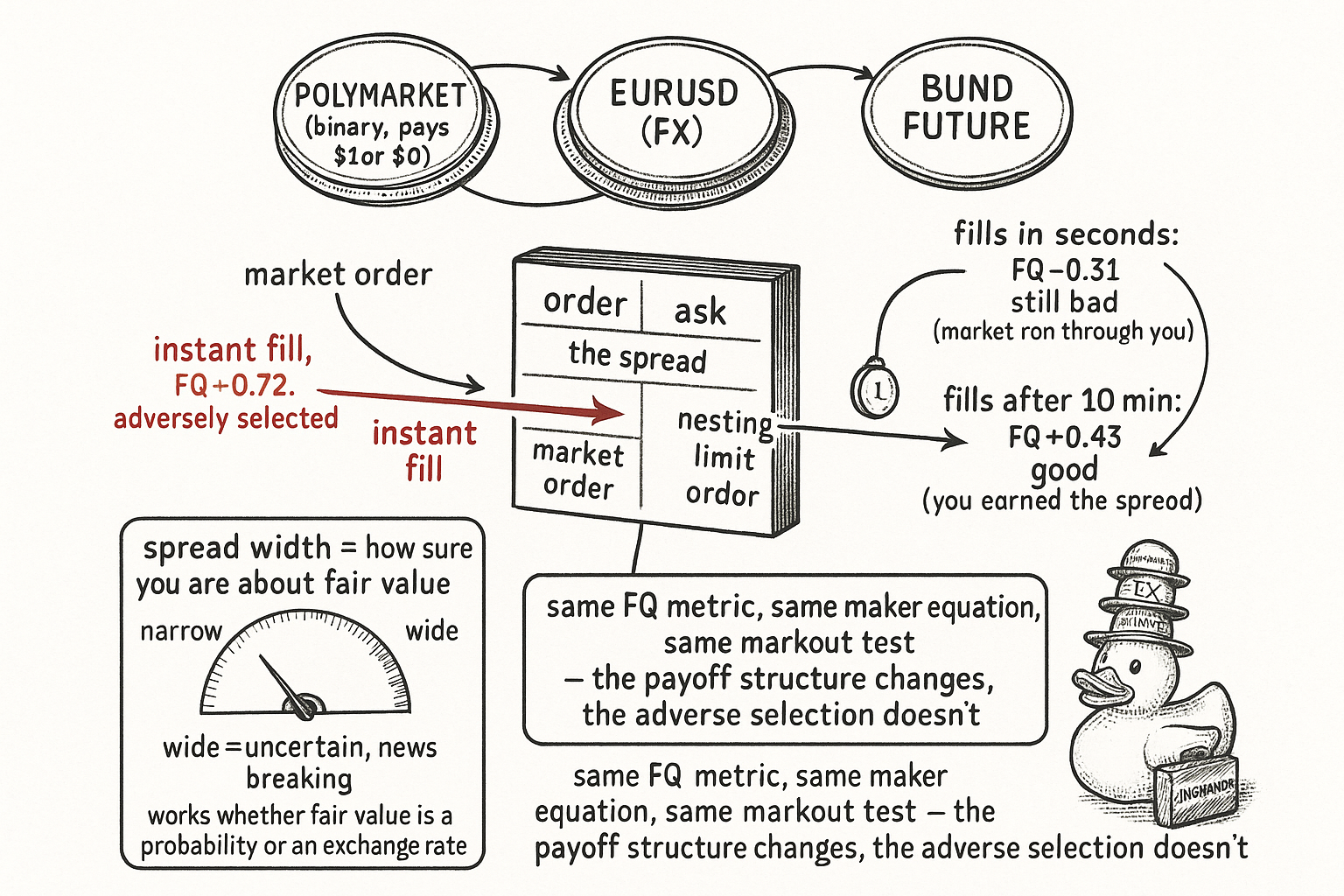

$$ \mathrm{FQ} \;=\; \frac{p_{\text{exec}} - p_{\text{mid}}}{p_{\text{ask}} - p_{\text{bid}}} $$

For a buy, the numerator is how far above the midpoint you actually executed and the denominator is the spread. Negative fill quality means you bought above where the market thinks fair value sits, the fingerprint of adverse selection. The prices in the formula are a probability on Polymarket and a currency rate on EURUSD, but the ratio is dimensionless and reads identically. Track it by order type and the pattern holds across markets.

| Order type | Average fill quality |

|---|---|

| Market orders | -0.72 |

| Limit orders filled in under 1 minute | -0.31 |

| Limit orders filled in over 10 minutes | +0.43 |

Market orders are badly adversely selected because you cross the spread against resting flow that had every chance to pull if your price was wrong. Fast limit fills are still negative because a quick fill means the market came to your price on its way through it. Slow limit fills come out positive because someone traded against you for liquidity reasons, not information, and you earned the spread you posted for. The slogan is market-agnostic: the faster the fill, the worse the adverse selection. The old article "Why Bid/Ask Bounce Matters for Intraday FX Systems" showed the FX residue of the same effect, where the spread-sized oscillation that a naive mean-reversion system reads as signal is the microstructure cost you pay on every fast fill.

The market maker's equation is the same equation

A maker in any of these markets is selling short-term insurance against price fluctuation, not forecasting the outcome. The profit model has two terms and the second is what separates a desk from a donor.

$$ \text{Profit} \;=\; \text{spread} \times \text{volume} \;-\; \text{adverse selection} \times \text{informed volume} $$

The first term is the spread earned across uninformed flow that trades for liquidity. The second is what informed traders extract when they pick you off. The business is profitable only when the spread collected from noise exceeds what the informed take, and this is true whether the contract is a binary on an election or a quarterly rate future. The old article "Market Making Is Not Just Collecting the Spread" built exactly this point for order books: the quoted spread is gross, one adversely-selected fill erases several spreads, and net-of-pickoff spread is what you keep. Nothing in that argument used a feature specific to any one market.

The defenses port too. Inventory skew, tightening the ask and widening the bid when you are already long to attract offsetting flow, is the old article "Why Skewing Is Simpler Than People Think" applied to whatever you are quoting. And the truth serum for whether you are making money or accumulating toxic inventory is markouts, the old article "Markouts: The Truth Serum of Market Making": look at where price sits a few minutes after your fill, not at the spread you nominally captured, because a book can show a healthy gross spread and a deeply negative markout at the same time on Polymarket and on crude alike.

Spread is posterior variance, on any instrument

How wide should you quote? As wide as your uncertainty about fair value. On Polymarket the fair value is a probability you hold a posterior distribution over, and the optimal spread tracks that posterior variance: confident, quote tight and capture volume; uncertain because news is breaking or the book is thin, quote wide, because a tight quote under uncertainty invites informed traders to pick the side you got wrong. Rename fair value from a probability to a currency rate and the rule is unchanged. The old article "Spread Widening During Volatility Expansion" is this reflex on continuous instruments, mapping short-horizon volatility to quoted width, and volatility is just the observable proxy for how uncertain you are about where price will be when you get filled. Uncertainty up, spread up, in both markets.

What actually differs, and why it does not matter

The honest difference is the payoff structure. A prediction-market contract terminates at a dollar or zero, so as resolution approaches the information asymmetry gets discrete and sharp, and a fast fill near resolution can mean the counterparty already knows the answer. FX and futures have no terminal binary payoff; adverse selection there is about short-horizon drift, someone trading ahead of a move measured in pips or ticks. The mechanism is the same, informed flow choosing your resting order at the moment it is about to hurt, and the difference is only in the shape of what "hurt" means. It changes your markout horizon and your spread calibration, not the existence or the sign of the effect.

This is why the make-versus-take decision is the same decision everywhere. The old article "Maker vs Taker Edge: Same Signal, Different Economics" made the general point that one signal is two different businesses depending on which side of the spread you sit on, and the old article "Market Orders vs Limit Orders in FX" turned it into an order-type rule: momentum and breakout need market orders because a resting limit never fills on a real breakout and captures only the failed ones, while mean-reversion suits limit orders because you want to fill at the overshoot you intend to fade. Structural arbitrage from "Arbitrage Is Just Projection" is a taking decision in prediction markets because the edge dies in a Polygon block; a breakout in futures is a taking decision because a resting limit inverts the edge. Same logic, edge magnitude against time decay, deciding whether paying the spread is worth the certainty.

The lesson survives the port intact. Fast fills are bad fills, the spread is not free money, markouts not nominal spread tell you if you are winning, and quote width is a readout of what you know. None of it is a Polymarket fact or an FX fact. It is an order-book fact.

KEY POINTS

- Fill quality, execution price minus midpoint over the spread, is dimensionless and reads identically on a Polymarket CLOB, EURUSD, and a bund future. Negative means adverse selection.

- The fill-quality pattern is market-agnostic: market orders average -0.72, sub-minute limit fills -0.31, ten-minute-plus limit fills +0.43. The faster the fill, the worse the adverse selection, in every order book.

- Market-maker profit equals spread times volume minus adverse selection times informed volume, whether the contract is a binary or a currency pair. It is positive only when noise-trader spread beats informed-trader losses.

- The defenses port without change: skew quotes to manage inventory, and check markouts a few minutes after the fill rather than the nominal spread, because a healthy gross spread can sit on a deeply negative markout in any market.

- Spread width equals posterior variance over fair value, and fair value being a probability or an exchange rate does not change the rule: confident, quote tight; uncertain, quote wide. Volatility is the observable proxy on continuous instruments.

- The only real difference is the payoff structure: prediction-market asymmetry gets sharp and discrete near resolution, FX and futures adverse selection is short-horizon drift. That changes the markout horizon and spread calibration, not the existence or sign of adverse selection.