9.18 Fast Fills Are Bad Fills: Make vs Take, Adverse Selection, and Why the Spread Is Posterior Variance

A limit order that fills in seconds is bad news: fast fills are adversely selected. Take liquidity only for arbs and large edges, provide it for small ones, and set your spread equal to your uncertainty about the true probability.

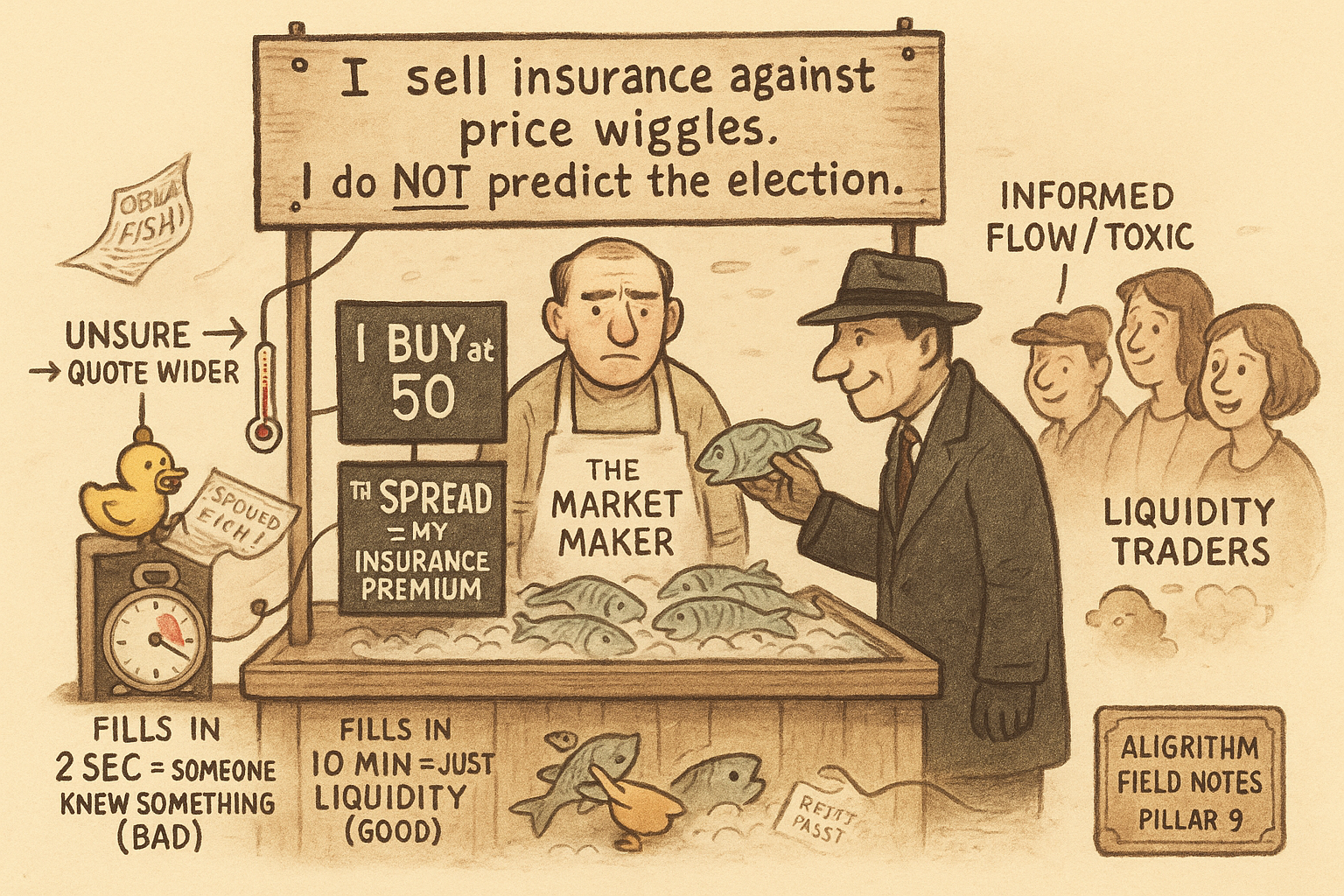

You post a limit order to buy NO at 41 cents. Two seconds later it fills. Feels great. It is a warning. A limit order that fills in seconds almost always filled because the market moved through your price on its way somewhere, and the somewhere is against you. The counterparty who hit your order knew something you did not, or was faster to the same news, and you just bought the thing that is about to be worth less. Slow fills are the good ones. Fast fills are the market telling you it agreed with your price for a reason you will not like.

That inversion, fast fills are bad fills, sits under every decision to use a market order or a limit order in a prediction market. The old article "Adverse Selection Explained for Traders" built the general case for order books. This is the prediction-market cut, where the contract pays a dollar or zero and the information asymmetry is sharp.

Two ways to touch the book

There are exactly two modes, and they trade opposite risks.

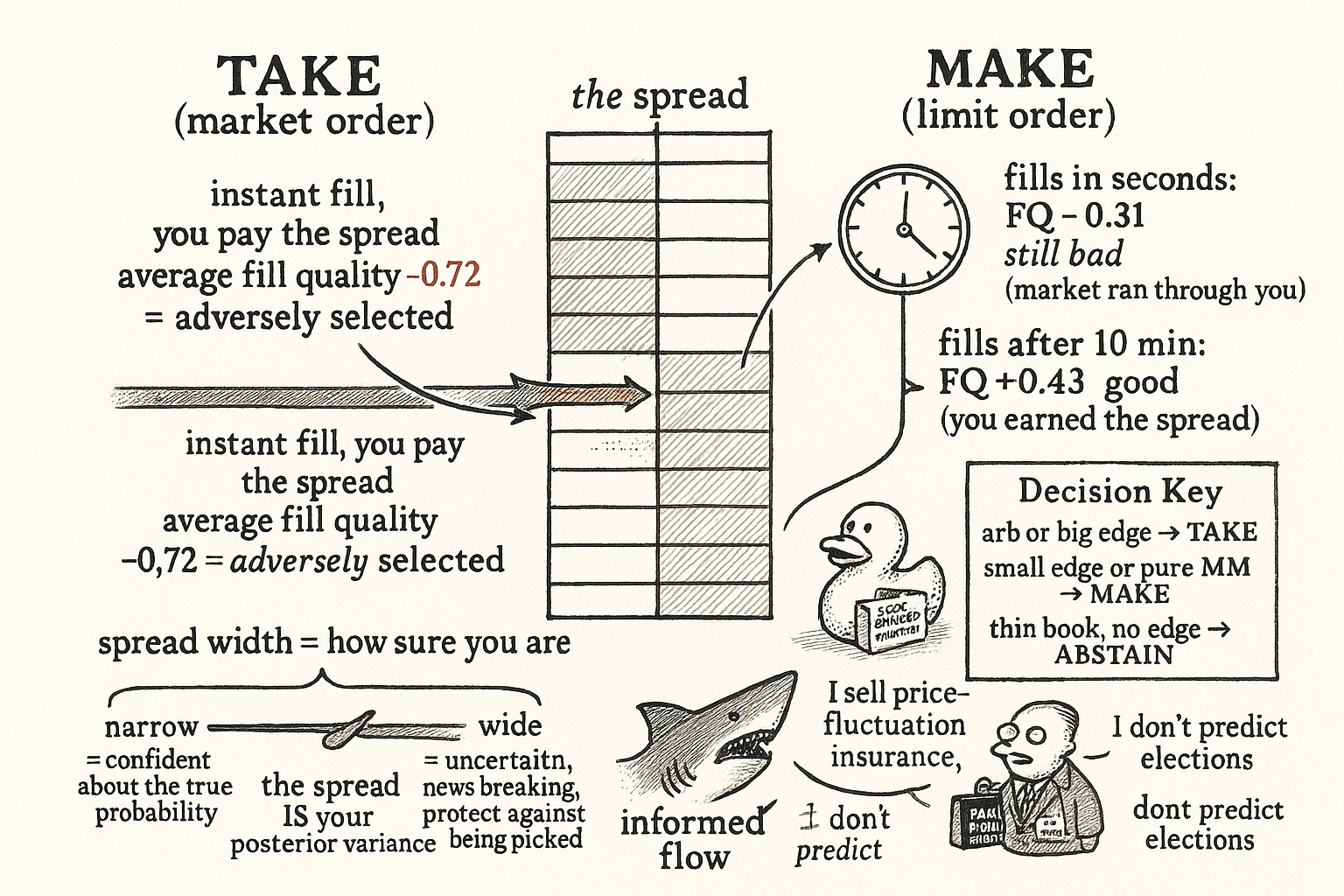

Taking liquidity means sending a market order or an aggressive limit that crosses the spread and fills immediately against resting orders. You get certainty of execution and you pay the spread, and you expose yourself to adverse selection because you are trading right now, against whoever is resting there, for reasons you have not checked.

Providing liquidity means posting a limit order at or inside the spread and waiting. You earn the spread when someone trades against you, and you carry the opposite risk: informed counterparties pick off your quote when the fair value has moved and you have not updated yet. The old article "Market Making Is Not Just Collecting the Spread" makes the point that the spread is not free money, it is payment for taking that risk.

Structural arbitrage from "Arbitrage Is Just Projection" is a taking decision, because the edge disappears in a block and you cannot wait. Most other edges are not, and treating them as taking decisions burns the spread for no reason.

Adverse selection, measured

When your market order fills, someone took the other side. Ask why. Most of the time the answer is that they had better information, and you can measure how badly that hurt with a single ratio: fill quality.

$$ \mathrm{FQ} \;=\; \frac{p_{\text{exec}} - p_{\text{mid}}}{p_{\text{ask}} - p_{\text{bid}}} $$

For a buy, the numerator is how far above the midpoint you actually executed, and the denominator is the spread. A negative fill quality means you bought above where the market thinks fair value sits, which is the fingerprint of adverse selection. Track it across order types and the pattern is stark.

| Order type | Average fill quality |

|---|---|

| Market orders | -0.72 |

| Limit orders filled in under 1 minute | -0.31 |

| Limit orders filled in over 10 minutes | +0.43 |

Read top to bottom. Market orders are badly adversely selected, because you cross the spread and trade against resting flow that had every chance to pull if the price was wrong. Limit orders that fill fast are still negative, because a quick fill means the market came to your price on its way through. Limit orders that sit for ten minutes before filling come out positive, because a slow fill means someone traded against you for liquidity reasons, not information, and you earned the spread you posted for. The metric confirms the slogan: the faster the fill, the worse the adverse selection. The companion piece "Fast Fills Are Bad Fills: The Numbers" digs into just this table if you want the narrow version.

Market making is selling insurance, not forecasting

A market maker in a prediction market is not predicting the election. They are selling short-term insurance against price fluctuation and getting paid the spread for it. The profit model has two terms, and the second is the one that kills amateurs.

$$ \text{Profit} \;=\; \text{spread} \times \text{volume} \;-\; \text{adverse selection} \times \text{informed volume} $$

The first term is the spread you earn across all the uninformed flow that trades against you for liquidity. The second term is what you pay when informed traders pick you off. Market making is profitable only when the spread you collect from noise traders exceeds what the informed ones extract. That is the entire business, and it is why "just collect the spread" is a way to go broke: you collect the spread and pay it back to the people who knew more, and your edge is the difference.

Two levers manage the second term. Inventory skew: when you are already long a contract, tighten your ask and widen your bid to encourage flow that flattens you, because a lopsided book is a directional bet you did not intend to make. This is the same skew logic as the old article "Why Skewing Is Simpler Than People Think," ported to binary contracts. And the truth serum for whether you are actually making money as opposed to accumulating toxic inventory is markouts, the subject of the old article "Markouts: The Truth Serum of Market Making": look at where the price is a few minutes after your fill, not at the spread you nominally captured.

The spread is posterior variance

Here is the part specific to prediction markets, and it ties this chapter to the Bayesian machinery. How wide should you quote? As wide as your uncertainty about the true probability.

The fair value of a binary contract is a probability, and you do not know it exactly. You hold a posterior distribution over it, and the width of that posterior is your uncertainty. The optimal spread should track that posterior variance. When you are confident about the true probability, quote tight and capture volume. When you are uncertain, because news is breaking or the market is thin or resolution is far off, quote wide, because a tight quote in high uncertainty is an invitation for informed traders to pick the side you got wrong. This is the direct link to the article on Bayesian edge in log-odds: greater uncertainty about the event probability means wider optimal spreads, and the spread is not a fee schedule, it is a readout of how much you know. The old article "Spread Widening During Volatility Expansion" shows the same reflex on continuous instruments: uncertainty up, spread up.

The decision table

Put edge type, magnitude, and time decay together and the make-versus-take choice falls out.

| Situation | Mode |

|---|---|

| Structural arbitrage detected (prices outside the fair set) | Take. Speed matters, the edge dies in a block. |

| Large informational edge | Take. Capture it before it diffuses into the price. |

| Small informational edge | Provide. Earn the spread on top of the edge. |

| No edge, heavy flow | Provide. Pure market making, sell the insurance. |

| Thin book, no flow | Neither. Abstain. |

The logic is edge magnitude against time decay. A structural arb that vanishes in one Polygon block demands aggressive taking, and paying the spread is worth it because the alternative is not getting the trade. A small informational edge that persists for hours is wasted on a market order, because you pay the spread to capture something you had time to earn passively. The old article "Maker vs Taker Edge: Same Signal, Different Economics" makes the general version: the same signal is a different trade depending on which side of the spread you are on. The bottom row matters most for discipline. Thin book, no flow, no edge: do nothing. Abstaining is a position, and it beats manufacturing trades to feel busy.

Visualizing make vs take

KEY POINTS

- Fast fills are bad fills. A limit order that fills in seconds filled because the market moved through your price toward something bad. Slow fills earn the spread from liquidity traders; fast fills hand you adverse selection.

- Two modes only: take liquidity (market order, instant, pay the spread, exposed to adverse selection) or provide it (limit order, earn the spread, get picked off by informed flow). Structural arbitrage is a take; most edges are not.

- Fill quality is the execution price minus the midpoint over the spread. Negative means adverse selection. Market orders average -0.72, sub-minute limit fills -0.31, ten-minute-plus limit fills +0.43. Speed and fill quality move opposite.

- Market making is selling insurance against price fluctuation, not forecasting. Profit is spread times volume minus adverse selection times informed volume, and it is positive only when noise-trader spread exceeds informed-trader losses. Skew quotes to manage inventory, and check markouts, not nominal spread, to know if you are winning.

- The spread should equal your posterior variance over the true probability. Confident, quote tight and capture volume. Uncertain, quote wide, because a tight quote under uncertainty invites informed traders to pick your wrong side. This is the Bayesian-edge link.

- Make-versus-take follows edge magnitude and time decay: take a structural arb (dies in a block) or a large informational edge (before it diffuses); provide on a small persistent edge or pure flow; abstain on a thin book with no edge.