9.3 The Six Ways to Lose Money on Polymarket

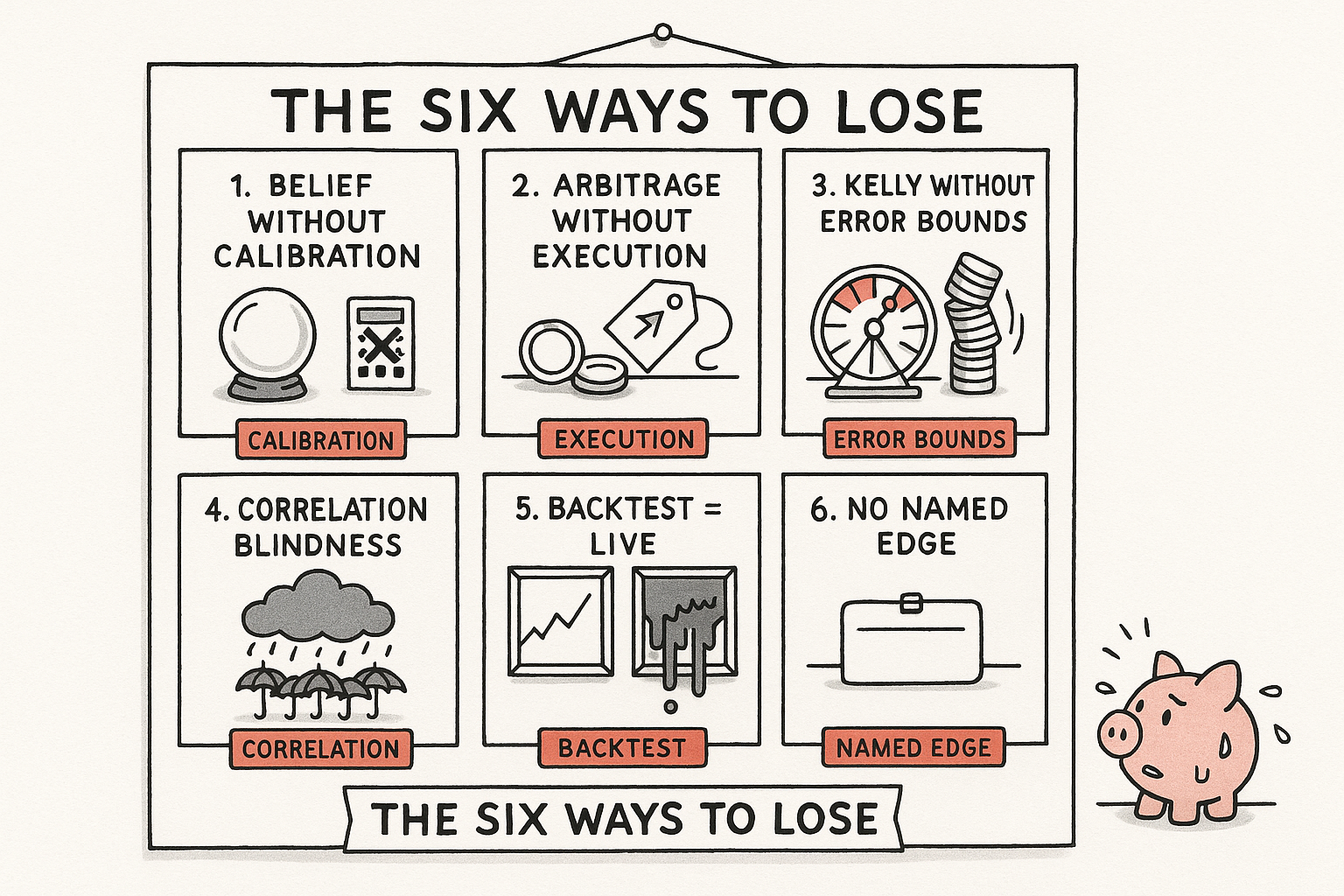

Prediction-market losses cluster into six anti-patterns: belief without calibration, arbitrage without execution, Kelly without error bounds, correlation blindness, backtest-equals-live, and no named edge. Each is a skipped step you can catch before you lose.

Most participants in prediction markets lose, and they lose in a small number of recognizable ways. Each way is a skipped step in the life of a trade, and each maps to one of the five invariants from the article on what a good trade is. Learn the six failure modes as a diagnostic. Before you enter, ask which one you might be committing. After you lose, the autopsy is faster because the suspects are named.

Every anti-pattern below follows the same shape: how it looks, why it kills, which invariant it breaks, and the fix. The numbers are worked, because a failure mode you cannot quantify is a failure mode you will repeat.

1. Belief without calibration

You assign 85% to an event the market prices at 52%, and you bet big. The 85% is a feeling. You never computed a likelihood ratio, never tracked whether your past "85%" calls resolved 85% of the time, never shrank the estimate toward the market. Kelly sizes the bet for 33 points of edge. If your true edge is 5 points, you are roughly 6.6 times too large, and the growth penalty is quadratic in that error.

$$ G(f^* + \Delta) \approx G(f^*) - \frac{\Delta^2}{2\sigma^2}, \qquad 6.6\times \text{ overbet} \;\Rightarrow\; G < 0 $$

Read that as: deviating from the optimal fraction by delta drops your long-run growth by about delta-squared over twice the variance, and at 6.6 times the correct size the growth rate crosses below zero, which is a path to certain ruin even when your direction was right. Breaks invariant 1 (name and quantify the edge) and invariant 4 (size for error). Fix: build a reliability diagram from your last 50-plus predictions. If your 80% bin resolves at 60%, you are overconfident. Shrink, or stop trading on beliefs. The old article "Why Trading Is a Probability Business, Not a Certainty Business" is the general form of this discipline.

2. Arbitrage without execution modeling

You see YES plus NO priced at $0.92 and buy both, expecting $0.08 risk-free. Leg one, YES at $0.30, fills. That fill moves the market, others update, and when you submit leg two the best ask on NO has climbed from $0.62 to $0.71. Total cost $1.01 against a $1.00 payout. You detected real arbitrage and still lost a cent.

$$ \text{leg 1: } \$0.30 \text{ fills} \;\to\; \text{leg 2 ask } \$0.62 \to \$0.71 \;\Rightarrow\; \text{cost } \$1.01 > \$1.00 \text{ payout} $$

Read that as: the first fill is not free information; it tips the market, the second leg reprices against you, and the arithmetic that looked like an $0.08 lock becomes an $0.01 loss once both legs are priced at what you actually pay. Breaks invariant 3 (executable under real liquidity). Fix: never compute profit without VWAP at target size across all legs, and require the residual edge after slippage, gas, and partial-fill cost to clear $0.05. Below that, skip. The article on execution as part of expected value formalizes the threshold.

3. Kelly without error bounds

Kelly returns a fraction of 0.20 and you deploy the full 20% of capital. Kelly assumes your edge estimate is exactly right. It never is. If the truth supports 0.04, you are five times too large.

$$ \text{true } f^* = 0.04, \quad \text{deployed } 0.20 \;\Rightarrow\; 5\times \text{ overbet} \;\Rightarrow\; P(\text{ruin over 100 trades}) > 30\% $$

Read that as: betting five times the fraction the real edge justifies pushes the probability of ruin over a hundred trades above 30%, because the error compounds multiplicatively in a way underbetting never does. The asymmetry is the whole lesson: underbetting slows growth but preserves capital, overbetting past a threshold destroys it. Breaks invariant 4. Fix: fractional Kelly. Half-Kelly keeps about 75% of the growth at roughly half the variance; quarter-Kelly is robust to large estimation error. The article on Kelly under model error works this in detail, and the old article "Why Volatility-Adjusted Position Sizing Matters" is the continuous-market cousin.

4. Correlation blindness

You hold arbitrage positions across five US state-election markets and call it diversified. It is not. A national shock, a scandal or a health event, moves all five at once. Linear correlation of about 0.75 hides a tail dependence near 0.85 to 0.95, and that gap is where portfolios die.

$$ \text{normal P\&L} \approx \pm\$0.10, \qquad \text{joint-tail loss} \approx \$2.50 \;\Rightarrow\; \text{ratio } 25{:}1, \text{ not the } 5{:}1 \text{ independence predicts} $$

Read that as: under normal conditions the five positions bob around plus or minus ten cents as if roughly independent, but in a joint tail event they all lose together for a combined $2.50, a 25-to-1 ratio versus the 5-to-1 that assuming independence would give. Breaks invariant 2, because the joint downside was never bounded. Fix: model dependence with a copula, use a Student-t with four to six degrees of freedom to capture the fat joint tails, and cap correlated exposure. The article on tail dependence and Student-t copulas builds this; the old article "Fat Tails: Why Gaussian Thinking Breaks Trading Systems" is the foundation.

5. Equating backtest and live performance

Your backtest shows $500 a day at a 94% win rate, so you deploy immediately. Backtests assume perfect fills at quoted prices. Live trading pays VWAP slippage, suffers partial fills, and eats adverse selection. Execution efficiency, the ratio of realized profit to the profit the math guaranteed, drops from 1.00 to somewhere around 0.65 to 0.80.

$$ \eta = \frac{\Pi_{\text{realized}}}{\Pi_{\text{guaranteed}}}, \qquad \text{backtest } \eta = 1.00 \;\to\; \text{live } \eta \approx 0.65\text{--}0.80 $$

Read that as: efficiency eta is what you actually kept divided by what the theory promised, it sits at one in a backtest that assumes flawless fills, and it falls to roughly two-thirds or three-quarters in live trading once slippage and adverse selection bite. The backtest also omits competition, since the other bots running your strategy were not in the historical tape, and it omits regime shift, since a 2024 edge can be gone by 2025. Breaks invariant 5. Fix: discount backtest profit by at least 30%, paper-trade two weeks, track eta from day one, and halt if it falls below 0.60. The old article "When to Switch Off a Trading System" covers the shutdown discipline.

6. Trading without a named edge

"The market feels wrong at $0.52. I am buying." "Feels wrong" is not a source. Without a named mechanism you cannot quantify the edge, cannot size the trade, and cannot tell skill from luck afterward. You are handing capital to the participants who can name their edge. Breaks invariant 1. Fix: before every trade, finish the sentence "my edge is ___ because ___." If you cannot, do not trade. This one discipline removes a large fraction of losing activity.

The common structure

Every anti-pattern is a skipped step in the trade life cycle. The map is exact.

$$ \begin{aligned} &\text{1. Belief w/o calibration} \to \text{skipped: Quantification}\\ &\text{2. No execution modeling} \to \text{skipped: Execution feasibility}\\ &\text{3. Kelly w/o error bounds} \to \text{skipped: Sizing-error analysis}\\ &\text{4. Correlation blindness} \to \text{skipped: Portfolio dependency check}\\ &\text{5. Backtest = live} \to \text{skipped: Execution reality check}\\ &\text{6. No named edge} \to \text{skipped: Detection} \end{aligned} $$

Read that as: each of the six failures corresponds to exactly one omitted stage in the life of a trade, from detection through quantification, sizing, execution, and the reality check against live conditions. The life cycle exists because each step guards one failure mode. Skip the step and that mode goes unguarded. The article on the nine sources of edge lays out the full life cycle these steps belong to.

KEY POINTS

- Losses on prediction markets come from six recognizable anti-patterns, each a skipped step in the trade life cycle and each breaking a specific invariant.

- Belief without calibration: a felt probability, not a computed one, oversizes the bet; at 6.6 times too large the growth rate goes negative. Build a reliability diagram and shrink.

- Arbitrage without execution modeling: the first fill moves the price, the second leg reprices, and a detected lock becomes a loss. Require residual edge over $0.05 after VWAP, gas, and partial fills.

- Kelly without error bounds: deploying full Kelly on a wrong estimate risks ruin above 30% over 100 trades. Use fractional Kelly.

- Correlation blindness: five "diversified" election bets share a joint tail near 0.85 to 0.95, turning a ten-cent wobble into a $2.50 loss. Model dependence with a Student-t copula and cap correlated exposure.

- Backtest equals live: perfect-fill backtests ignore slippage, competition, and regime shift; efficiency drops to two-thirds. Discount 30%, paper-trade, and halt below 0.60.

- Trading without a named edge: "feels wrong" cannot be sized or evaluated. Finish "my edge is ___ because ___" or do not trade.

References

- Efficient Market Making via Convex Optimization, and a Connection to Online Learning

- An Optimization-Based Framework for Automated Market-Making

- Automated Market Making for Parlay-style Joint Contracts

- A New Understanding of Prediction Markets Via No-Regret Learning

- Who Wins and Who Loses in Prediction Markets? Evidence from Polymarket and Kalshi

- Price Discovery and Trading in Modern Prediction Markets

- Microstructure Evidence from the Polymarket Order Book

- Comonotonic Book-Making with Nonadditive Probabilities