9.4 The Nine Sources of Edge, Ranked Cleanest to Dirtiest

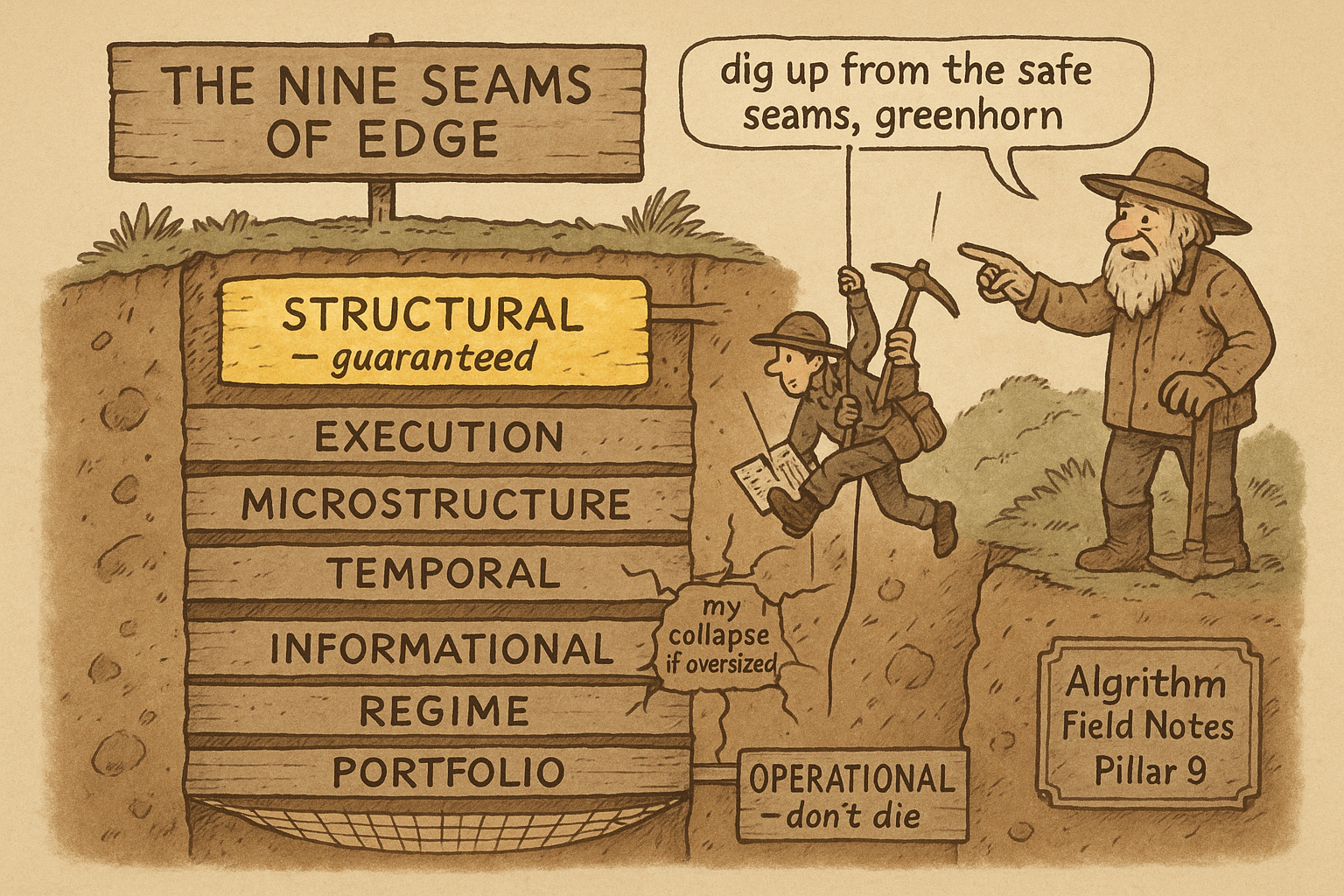

Nine sources of edge in prediction markets, ranked cleanest to dirtiest: structural, execution, microstructure, temporal, informational, regime, portfolio, adversarial, operational. Forecasting is fifth and the most dangerous to size.

A source of edge is a structural reason your expected value is positive before you size the trade and before you execute it. If you cannot name the source, you do not have an edge, you have a position. Prediction markets support nine sources, and they are not equal. Some hand you a mathematical guarantee. Some hand you a fleeting statistical tilt that is lethal to oversize. Ranking them, and knowing which one you are actually exploiting, is the map this whole pillar builds toward.

The ordering below runs cleanest to dirtiest, where clean means the profit is close to guaranteed and the edge is hard to erase, and dirty means the profit is uncertain and the edge decays or blows up if you misjudge it. Most participants start at number five and wonder why they struggle. The correct developmental order runs the other way.

The ranking

Each source answers one question, offers one grade of certainty, persists for one kind of horizon, and gets formalized in specific later articles of this pillar.

$$ \begin{array}{clll} \# & \textbf{Source} & \textbf{Core question} & \textbf{Certainty / persistence}\\ 1 & \text{Structural} & \text{Is the market internally inconsistent?} & \text{Guaranteed / permanent}\\ 2 & \text{Execution} & \text{Do I fill when others do not?} & \text{Measurable / permanent}\\ 3 & \text{Microstructure} & \text{Is the order book mispriced?} & \text{Small, repeatable / medium}\\ 4 & \text{Temporal} & \text{Are prices lagging reality?} & \text{Time-decaying / short}\\ 5 & \text{Informational} & \text{Is my belief better than the market's?} & \text{Uncertain / short--medium}\\ 6 & \text{Regime} & \text{Am I trading only when conditions favor me?} & \text{Meta-edge / long}\\ 7 & \text{Portfolio} & \text{Am I combining trades better than others?} & \text{Meta-edge / long}\\ 8 & \text{Adversarial} & \text{Do I understand how others behave?} & \text{Rare / medium}\\ 9 & \text{Operational} & \text{Do I avoid catastrophic mistakes?} & \text{Prevents loss / permanent} \end{array} $$

Read that as: a nine-row table where each edge names the question it answers, how certain the profit is, and how long it survives, running from structural inconsistency at the top, where the math guarantees a permanent edge, down through information and portfolio construction to operational discipline, whose payoff is avoided disaster rather than gained profit.

Why structural sits at the top

Structural edge exists when prices contradict each other, when the price point sits outside the marginal polytope from the article on convex geometry. The math guarantees profit and no forecast is required. The contradiction is not a transient inefficiency competition will erase, it is a permanent feature of any venue that prices markets fast and independently, because enforcing full cross-market consistency in real time is an NP-hard problem no low-latency exchange will solve per order. The edge regenerates continuously. That is why it ranks first: guaranteed and permanent.

Execution ranks second because infrastructure, not prediction, guarantees you realize the theoretical edge. If your system fills both legs of an arbitrage inside one block while slower systems drift, the profit is measurable and the advantage does not decay as long as you stay fast. Microstructure, reading a mispriced order book, ranks third: small per trade but reliably repeatable. Temporal edge, trading a price that lags reality, ranks fourth: real but fleeting, and it demands speed.

Why informational sits in the middle, not the top

Forecasting is number five, below four sources that require no view on the outcome at all. This ranking offends most traders, who arrive convinced their opinion is the product. The demotion is deliberate. Informational edge is real but dangerous to size, because the edge estimate carries large uncertainty and the penalty for overestimating is asymmetric and severe. The article on the six ways to lose shows how a felt 85% against a market's 52% turns into a 6.6-times overbet and negative growth. A structural arbitrage cannot do that to you. A forecast can. Uncertain profit, short-to-medium persistence, high blow-up risk: middle of the pack, and the most seductive trap in the market.

The meta-edges and the floor

Regime, number six, is a meta-edge: it improves every source above it by telling you when to trade and when to abstain. Not trading during a crowded or thin-liquidity regime beats detecting one more marginal opportunity. Portfolio, number seven, is the other meta-edge: combining trades so a hidden correlation does not blow up the book, the failure the article on tail dependence dissects. Adversarial, number eight, understanding how other participants behave, is rare and powerful but hard to formalize. Operational, number nine, is the floor: avoiding catastrophic mistakes, the kill switches and position caps whose payoff is a loss you never took. Survivorship is the ultimate edge, and the old article "Why Loss Control Is the Only Thing You Fully Control" is the same claim in a different market.

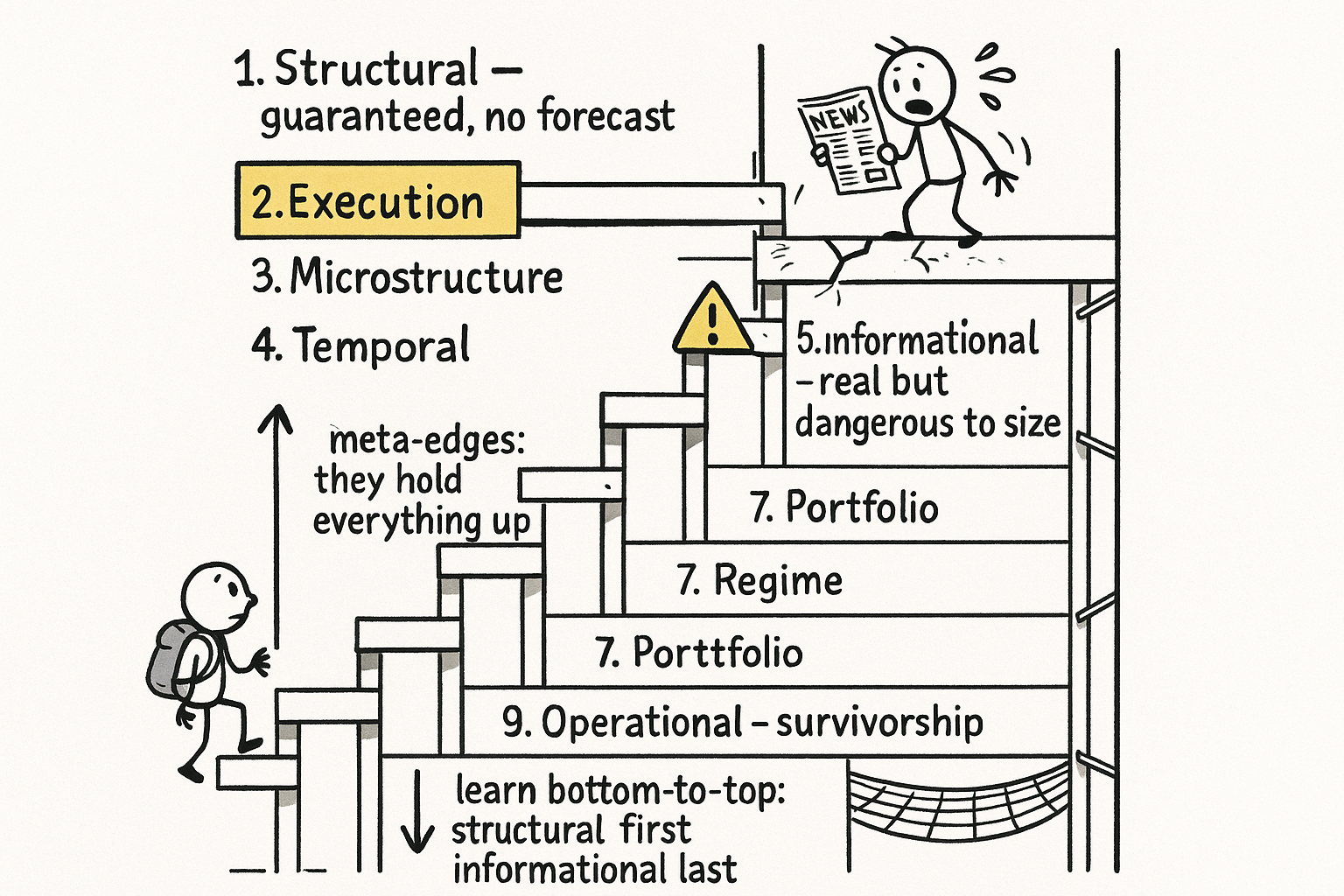

The correct developmental order

The ranking is not the order you learn them. Most participants begin at informational, hold beliefs about outcomes, and lack the detection, infrastructure, and regime awareness to survive. Build the other way.

$$ \text{structural} \;\to\; \text{execution} \;\to\; \text{sizing} \;\to\; \text{regime} \;\to\; \text{informational} $$

Read that as: master detecting guaranteed structural edge first, then the execution infrastructure to capture it, then the sizing math to survive error, then the regime awareness to know when to act, and only last take on the dangerous informational edge, once you have the machinery to size and evaluate it safely.

The life cycle every good trade follows

Whatever the source, a profitable trade passes through six stages, and skipping any one leaves a specific failure mode unguarded, the exact failures catalogued in the article on the six ways to lose.

$$ \begin{aligned} &\text{1. Detection: name the source, quantify the edge}\\ &\text{2. Quantification: } \Pi = D(\hat{p}\,\|\,\text{state}) - g - \mathbb{E}[\text{slippage}] - \text{fees}\\ &\text{3. Sizing: } f = f^* \times P(\text{fill}) \times (1 - s) \times \rho_{\text{regime}}\\ &\text{4. Execution: parallel submission, fill monitoring, partial handling}\\ &\text{5. Attribution: } \eta = \Pi_{\text{realized}} / \Pi_{\text{guaranteed}}, \text{ tag by source}\\ &\text{6. Adaptation: update regime, recalibrate, adjust} \end{aligned} $$

Read that as: detect and name the edge, quantify the profit net of the approximation gap, slippage and fees, size it by scaling the growth-optimal fraction down for fill probability, slippage, and regime, execute all legs in parallel while watching fills, attribute the realized-to-guaranteed ratio and tag it by source, then adapt as the regime shifts. Omit detection and you are gambling. Omit quantification and you cannot size. Omit sizing and you are guessing amounts. Omit execution modeling and you own theoretical profits only. Omit attribution and you cannot improve. Omit adaptation and you are static in a game that is not.

KEY POINTS

- A source of edge is a named structural reason expected value is positive before sizing and execution. No name, no edge.

- Nine sources exist, ranked cleanest to dirtiest by how guaranteed the profit is and how hard the edge is to erase.

- Structural edge ranks first: a mathematical guarantee from price contradictions, permanent because fast, independent pricing cannot enforce consistency in real time.

- Execution, microstructure, and temporal edges follow, none requiring a forecast.

- Informational edge ranks fifth, not first. It is real but dangerous to size, and overconfidence turns it into ruin, which is why most participants who start there struggle.

- Regime and portfolio are meta-edges that improve or protect everything above them; operational discipline is the floor, where the payoff is disaster avoided.

- Learn them in reverse of most people's instinct: structural, then execution, then sizing, then regime, then informational.

- Every good trade passes six stages: detection, quantification, sizing, execution, attribution, adaptation. Each skipped stage is a named way to lose.

References

- Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets - Saguillo et al. (2025)

- Anomalies: The Law of One Price in Financial Markets

- avoiding strategic and dynamic complications, and a comonotonic

- On a participation structure that ensures representative prices in prediction markets

- Complexity of Combinatorial Market Makers

- Who Profits from Prediction? Execution, not Information

- Price Discovery and Trading in Modern Prediction Markets

- Evidence of Persistent Arbitrage in Prediction Markets