9.5 Match Your Edge to Your Resources

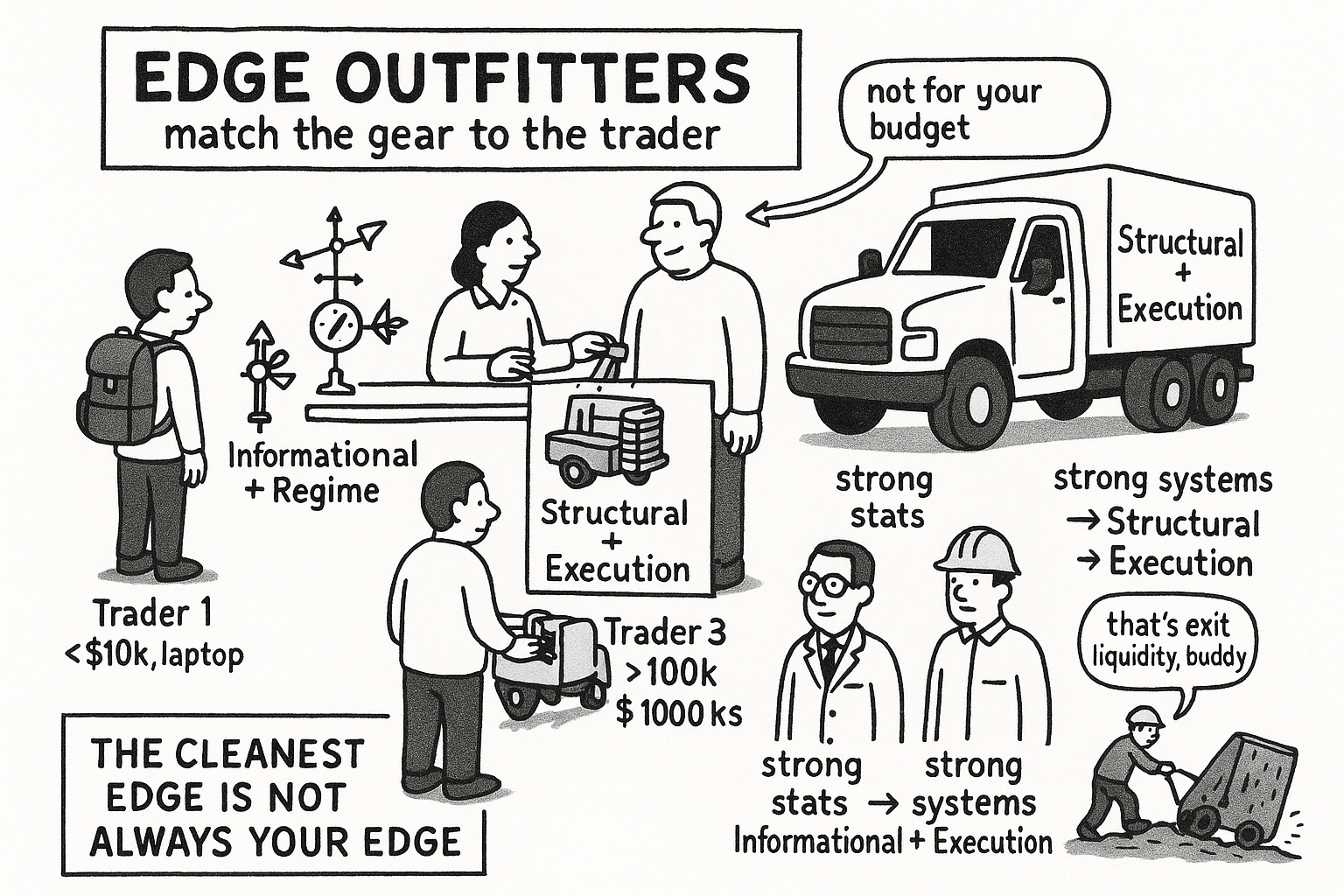

The cleanest edge is not always yours. Match the source to your resources: small accounts trade informational and regime, large accounts with infrastructure run structural and execution, and specialists play to their skill.

The article on the nine sources of edge ranks structural arbitrage first and forecasting fifth. That ranking is not a personal instruction. It describes which edge is cleanest in the abstract, not which edge you should chase with the capital and infrastructure you actually have. A trader with $5,000 and a laptop who reads "structural is best" and tries to run an integer-programming arbitrage engine against bots colocated near the Polygon sequencer is about to donate money. The right edge is a function of your resources, and choosing wrong is its own way to lose.

Structural edge is the cleanest and also the most capital- and infrastructure-hungry. The two facts do not conflict. Cleanest means the profit is guaranteed once you capture it. Capturing it means winning a latency race that costs real money to enter. Match the edge to what you can afford to build.

The selection table

Read your row by the resources you have, then read what to pursue and what to avoid.

$$ \begin{array}{lll} \textbf{Resources} & \textbf{Pursue} & \textbf{Avoid}\\ <\$10\text{K, no infra} & \text{Informational + Regime} & \text{Structural (infra cost} > \text{capital)}\\ \$10\text{K--}\$100\text{K, basic infra} & \text{Microstructure + Execution} & \text{Adversarial (too little data)}\\ >\$100\text{K, production infra} & \text{Structural + Execution} & \text{Informational alone (not scalable)}\\ \text{Strong ML / stats} & \text{Informational + Temporal} & \text{Structural (wrong skill set)}\\ \text{Strong systems eng.} & \text{Structural + Execution} & \text{Informational (play to strengths)} \end{array} $$

Read that as: a small account with no infrastructure should trade informational and regime edges and stay away from structural arbitrage, because the infrastructure to compete costs more than the account holds; a mid-size account should chase microstructure and execution; a large account with production infrastructure should run structural and execution and avoid informational trading alone because it does not scale; and if your strength is modeling, lean into informational and temporal, while if your strength is systems engineering, lean into structural and execution.

The counterintuitive rows are the small account and the strong-modeler. The cleanest edge, structural, is the wrong target for the trader with the least money, because the guarantee is worthless if the two or three fastest bots capture it before your order confirms. The small account's realistic edge is informational, exactly the source the ranking called dangerous, because that trader has no faster option and must lean on judgment plus the discipline to abstain during bad regimes. A strong quant is told to avoid structural not because it is bad but because it rewards a different skill: winning structural arbitrage is a systems-engineering problem, low-latency I/O and solver speed, not a statistics problem.

Why the small account cannot buy the clean edge

Structural arbitrage on Polymarket closes fast. The opportunity can vanish inside one Polygon block, and the decision-to-mempool window that decides who wins is on the order of tens of milliseconds. Winning that race requires monitoring infrastructure, a fast integer-programming solver, and order routing tuned to submit all legs inside one block. That is a fixed cost measured in tens of thousands of dollars and ongoing engineering, and profits are concentrated: the fastest two or three systems on any given opportunity take the large majority, and the slower entrants lose on adverse fills. The article on regimes and crowding quantifies the winner-take-most math. A $5,000 account entering that race is exit liquidity.

The same account can trade informational edge because that edge decays over hours or days, not milliseconds, so latency stops being the binding constraint. The binding constraint becomes calibration and discipline, which cost time rather than capital. The old article "Why Trading Is a Probability Business, Not a Certainty Business" and the article on the six ways to lose spell out the calibration bar that edge demands.

The six-stage life cycle applies to every row

Whatever edge your row points to, the trade still passes through the same six stages, and skipping any stage is the same failure regardless of resources.

$$ \text{Detection} \to \text{Quantification} \to \text{Sizing} \to \text{Execution} \to \text{Attribution} \to \text{Adaptation} $$

Read that as: name and quantify the edge, size it for error, execute all legs, measure realized against guaranteed profit, and adapt as the regime shifts, in that order, every time. A small informational trader skips execution modeling at the same peril as a large structural desk. The stages do not scale with account size. Only the edge you feed into them does.

Attribution keeps you honest about your row

Pick a row, trade it, then check whether the edge you claimed is the edge you got. Tag every trade by source and track execution efficiency, realized profit over guaranteed profit, per source.

$$ \eta = \frac{\Pi_{\text{realized}}}{\Pi_{\text{guaranteed}}}, \qquad \eta > 0.85 \text{ excellent}, \quad 0.60\text{--}0.85 \text{ fix infra first}, \quad <0.60 \text{ stop} $$

Read that as: efficiency eta is what you kept divided by what the setup promised, above 0.85 is excellent, between 0.60 and 0.85 means improve your infrastructure before adding capital, and below 0.60 means execution is destroying edge faster than the math creates it, so stop and fix it before deploying more. A large account whose structural eta keeps printing below 0.60 is not out-resourced on paper, it is losing the latency race in practice and should reconsider its row. The article on execution efficiency and regret builds the full attribution dashboard.

KEY POINTS

- The nine-source ranking says which edge is cleanest, not which edge you should trade. The right edge depends on your capital, infrastructure, and skill set.

- Structural arbitrage is the cleanest and the most infrastructure-hungry at once. The guarantee is worthless if faster systems capture it first.

- Small accounts with no infrastructure should trade informational and regime edges, because those decay over hours not milliseconds, so discipline and calibration matter more than latency.

- Mid-size accounts should pursue microstructure and execution; large accounts with production infrastructure should run structural and execution and avoid informational-alone, which does not scale.

- Match the edge to your strength: modelers to informational and temporal, systems engineers to structural and execution. Winning structural arbitrage is an engineering problem, not a statistics one.

- Every row runs the same six-stage life cycle. The stages do not scale with account size; only the edge you feed them does.

- Track execution efficiency per source. Above 0.85 is excellent, 0.60 to 0.85 means fix infrastructure before scaling, below 0.60 means stop, and a persistently low structural efficiency is a signal you are in the wrong row.

References

- Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets - Saguillo et al. (2025)

- Price Discovery and Trading in Modern Prediction Markets

- Evidence of Persistent Arbitrage in Prediction Markets

- Statistical Arbitrage in Binary Prediction Markets: Three Systematic Trading Strategies

- An Optimization-Based Framework for Automated Market-Making

- Automated Market Makers for Decentralized Finance (DeFi)

- Market Microstructure for Decentralized Prediction Markets (DePMs)

- Microstructure Evidence from the Polymarket Order Book