9.6 Outcome Geometry: Why Two Fair Markets Can Be Jointly Unfair

Two prediction markets can each sum to a fair dollar and still be jointly riggable. The reason is geometry: logic deletes impossible outcomes, and the prices can land outside what's left.

Take two prediction markets that each look priced correctly. "Candidate A wins State X" trades at 52 cents for YES, 48 for NO, and the two add to a dollar. "Party P wins State X by more than 5 points" trades at 32 and 68, also a clean dollar. Read either book on its own and you find nothing to trade. Read them together and there can be a guaranteed profit sitting in plain sight, because the two markets describe the same world and the platform priced them as if they didn't. That gap is the entire subject of this pillar, and it starts before any probability, any forecast, any opinion about who wins. It starts with the geometry of what these contracts pay.

The first question a trader has to answer about any contract is mechanical: what does it pay in every possible state of the world? Not "what do I think will happen." What does the ticket pay if the world turns out one way, and what does it pay if it turns out another. Answer that for a set of related contracts and the shape of the opportunity is already fixed, whether or not anyone has looked.

The outcome space is the list of ways the world can end

Call the set of every possible joint resolution the outcome space. For one binary market, "Will A win X?", there are two ways the world lands: A wins, A loses. Two outcomes. For a single multi-candidate primary with four names on the ballot, four outcomes. Nothing subtle yet.

The subtlety arrives the moment markets multiply. Put three binary markets side by side and the naive count of joint outcomes is 2 times 2 times 2, eight combinations. Ten binary markets give a thousand. This is the count that matters, and it grows the way compounding grows.

$$ |\Omega|_{\text{naive}} = 2^{n} $$

Here the vertical bars mean "the size of," the Greek omega is the outcome space, and n is the number of binary markets. Each market doubles the count. Ten markets, 1,024 joint outcomes; twenty markets, over a million; the 63 games of an NCAA bracket, about 9.2 quintillion. The number runs away from you fast, and most of this pillar is about taming it. Hold that thought.

The count above is the naive count, and the word naive is doing real work. It assumes the markets are logically independent, that any combination of results can happen. Reality does not grant that.

Payoff vectors turn a contract into a row of ones and zeros

To reason about a bundle of contracts at once, stop thinking in prose and start thinking in a table. For each way the world can end, write down what each contract pays: a 1 if it pays out, a 0 if it does not. That row of ones and zeros is the payoff vector for that outcome.

$$ \varphi_i(\omega) = \begin{cases} 1 & \text{if security } i \text{ pays out under outcome } \omega,\\ 0 & \text{otherwise.} \end{cases} $$

Read it as a lookup, not a formula. The symbol phi with subscript i is the payoff of contract i; omega is one specific way the world ends. Feed in a world and a contract, get back a 1 or a 0. Do this for every contract and you have one row. Do it for every possible world and you have the whole table. A programmer would call each row a boolean array indexed by contract, and that is exactly the right mental model.

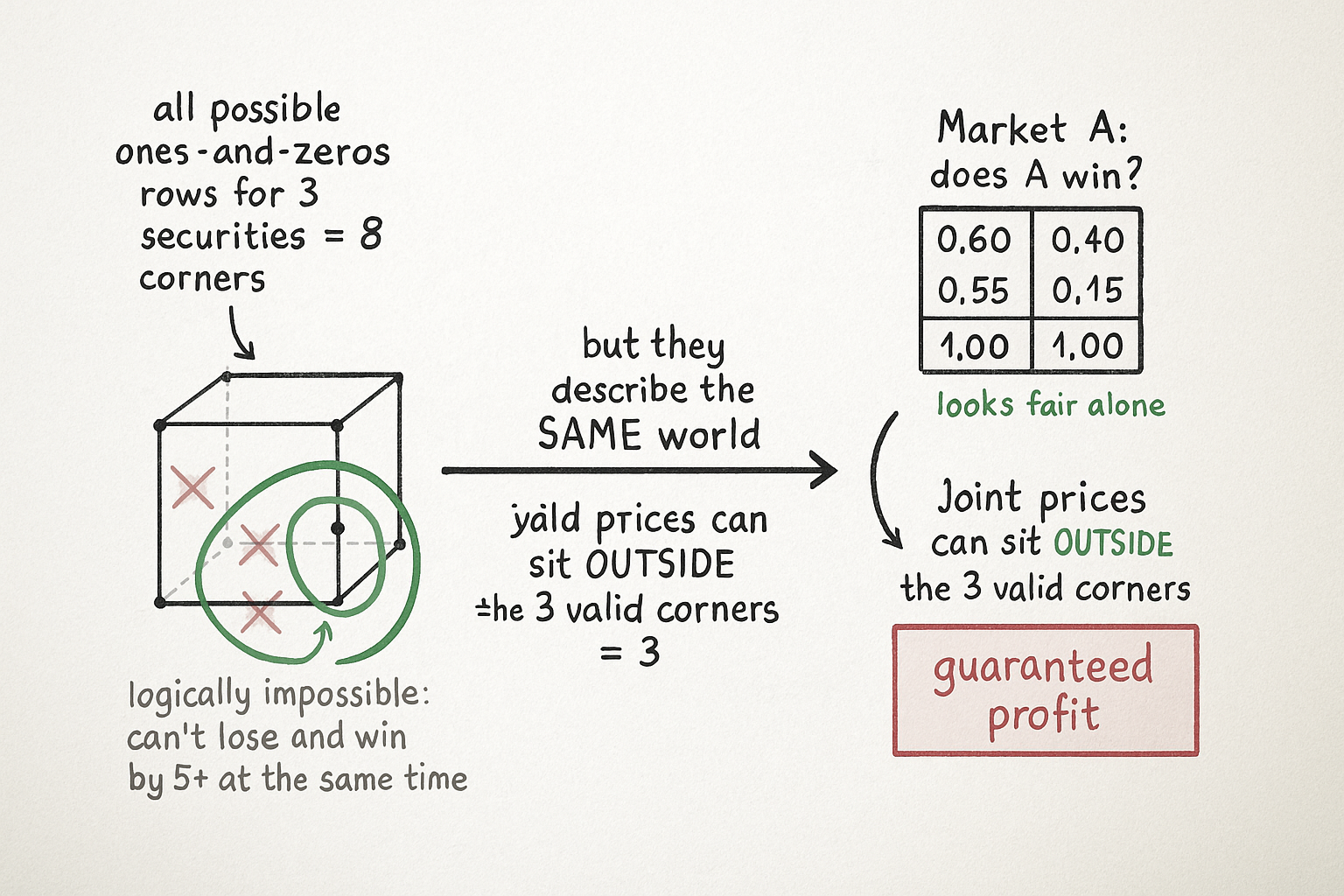

Now the example that carries the whole idea. Two markets on State X. The first has YES (A wins) and NO (A loses). The second has one security, YES on "Party P wins X by more than 5 points." Three tradeable securities. Write the table.

| Outcome | A wins (YES) | A loses (NO) | Margin > 5 |

|---|---|---|---|

| A wins by more than 5 | 1 | 0 | 1 |

| A wins by 5 or less | 1 | 0 | 0 |

| A loses | 0 | 1 | 0 |

Count the rows. Three, not four. The missing row is the one where A loses and the margin is greater than 5, and it is missing because it cannot happen. You cannot win by more than 5 points and also lose. The logic of the contracts deleted a row that a naive count would have kept.

The valid payoff set, and where the money hides

Collect the rows that actually survive and you get the valid payoff set. Every row is a corner of a cube whose dimension equals the number of securities, but most corners of that cube never appear, because logic forbids them.

$$ Z = \{\varphi(\omega) : \omega \in \Omega\} \subset \{0,1\}^{|\mathcal{I}|}, \qquad |Z| \ll 2^{|\mathcal{I}|} $$

Z is the set of valid rows. The curly-brace expression on the right is the full cube of all possible ones-and-zeros rows across the securities; the double-less-than sign says Z is far smaller than that cube. Three securities give a cube with eight corners. Our table used three of them. Five corners of the cube are logically impossible and simply do not exist as tradeable outcomes.

That collapse is the point. The number of valid outcomes sits far below the number of ways you could arrange the securities on paper, and the size of the collapse measures how tightly the contracts are wired together. When two contracts share no logic, nothing collapses and there is no structural edge to find. When they are wired together, the valid set shrinks, and the shrinkage is precisely the room in which a platform can misprice one contract relative to another without any single book looking wrong.

Here is the mechanism stated plainly. Polymarket lists and prices each contract in its own book, with its own order flow, as if it were alone in the universe. "Party P wins by more than 5" implies "A wins," but the market maker running the first book does not consult the second. So the joint set of prices can drift into a combination that no probability distribution over the three real outcomes could ever produce. The individual books stay coherent. The pair does not. Two fair markets, jointly unfair.

The structural pre-check

Before you form any view about who wins anything, run four questions on any set of related markets. This is the whole chapter reduced to a checklist you can execute in a minute.

First, list the contracts. What can you actually buy and sell. Second, describe the possible worlds, the outcome space, either by listing them or by writing down the constraints that link them. Third, compute the valid payoff set, the surviving rows. Fourth, compare the size of that set to the naive cube. If the valid set is smaller than the cube, dependencies exist, and structural edge may be present. If it equals the cube, the markets are genuinely independent and structural arbitrage across them is impossible, no matter how wrong the prices feel.

That last clause matters more than it looks. A market can be badly mispriced in your opinion and still offer no structural trade, because your opinion is a forecast, and forecasting is the dangerous, low-ranked source of edge this pillar treats last. Structural edge does not care what you believe. It only asks whether the prices are internally consistent with the geometry of what the contracts pay. If you cannot answer the four questions, you cannot know whether an edge exists, and trading on the feeling that something is off is how accounts donate money to the people who ran the check.

The empirical scale is worth stating so the geometry does not stay abstract. A 2024 to 2025 study of the US election markets on Polymarket found 1,576 logically dependent market pairs in the presidential race alone, and that was one race in one cycle. No human prices thousands of pairs against each other in their head. The collapse of the valid set is happening constantly, across far more contracts than anyone can track by hand, which is exactly why the edge is mechanical rather than a matter of insight.

What this buys you, and what it does not

Outcome geometry hands you a verdict on whether a trade can exist, not on whether you can capture it. The three-row table tells you the shape of the opportunity. It says nothing about whether the second leg will still be there at the price you need when your first leg fills, nothing about the fee to move on-chain, nothing about the two other bots watching the same pair. Those live in later articles, and they are where most of the theoretical profit leaks away.

What you have after this article is the right first question. Not "what will happen," but "what does each contract pay in every state, and is the joint set of prices consistent with the small set of states that can actually occur." The next article, the article "The Dutch Book Theorem, Plainly," turns the smallest version of that inconsistency, prices that fail to sum to one, into a guaranteed-profit portfolio you can write down. The one after that, the article "The Marginal Polytope," generalizes the whole thing into a single shape that contains every fair price and a single test for whether you are outside it.

KEY POINTS

- The first question about any contract is mechanical, not predictive: what does it pay in every possible state of the world. Answer that for a bundle of related contracts and the shape of the opportunity is already fixed.

- The naive count of joint outcomes for n binary markets is 2 to the n, which explodes fast (ten markets, 1,024; an NCAA bracket, about 9.2 quintillion), but that count assumes the markets are logically independent.

- Write each outcome as a payoff vector, a row of ones and zeros over the securities. Logical links between contracts delete impossible rows, so the valid payoff set is far smaller than the full cube of arrangements.

- The size of that collapse is where structural edge lives. Platforms price each contract in its own book; when contracts share logic that no single book enforces, the joint prices can land outside the small set of states that can actually happen.

- Run the structural pre-check: list contracts, describe the worlds, compute the valid set, compare it to the naive cube. Smaller than the cube means dependencies and possible edge; equal to the cube means no structural trade exists regardless of how mispriced it feels.

- A 2024 to 2025 Polymarket study found 1,576 logically dependent market pairs in the presidential race alone. No human tracks that many pairs, which is why this edge is mechanical, not a matter of having a better opinion.