9.7 The Dutch Book Theorem, Plainly, and Why Polymarket Will Always Have Arbitrage

Prices that don't sum to a dollar are a guaranteed trade, not a rounding error. De Finetti proved it in 1937, and Polymarket's speed-first design guarantees the mispricings keep coming.

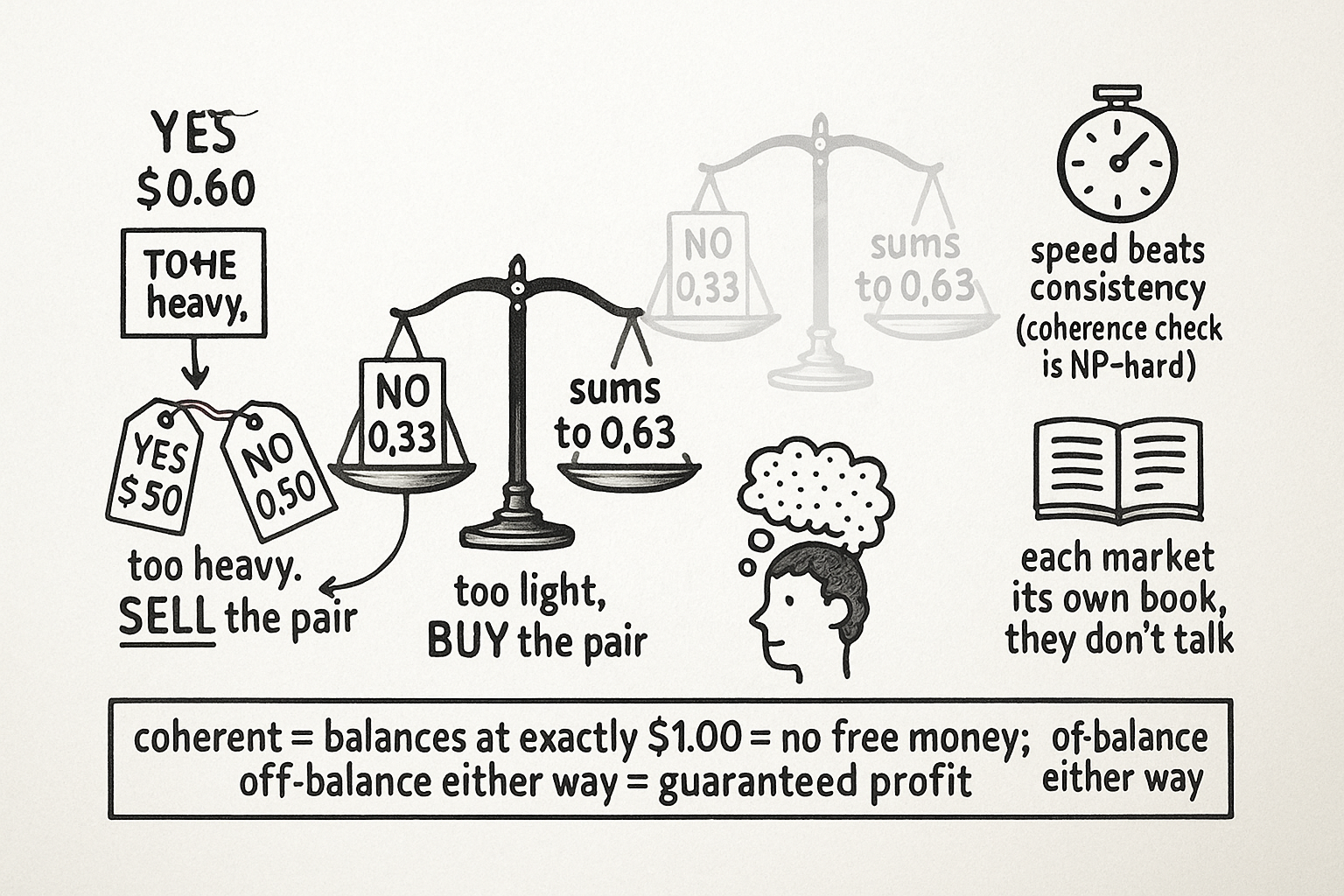

A binary market shows YES at 60 cents and NO at 50 cents. Sum them: $1.10. Exactly one of the two will pay a dollar at resolution. Sell one of each, collect $1.10 now, pay out $1.00 later, keep 10 cents no matter what happens. No forecast. No opinion about the event. The prices contradicted themselves and the contradiction was money. That trade has a name from 1937, and the theorem behind it explains why a platform like Polymarket cannot stop producing these opportunities without breaking the thing that makes it fast.

The article "Outcome Geometry" set up the machinery: contracts, the outcome space, the valid payoff set. This article uses it to answer one decision. Are the prices in front of you logically consistent, or is there a portfolio that wins under every outcome. If the second, the prices are incoherent, and incoherent prices are exploitable by definition.

What coherent prices actually mean

Coherent is a precise word here, not a compliment. A set of prices is coherent if you can read them as probabilities without contradicting yourself. Three conditions have to hold at once.

First, no negative prices. A contract cannot cost less than nothing. Second, normalization: across a set of outcomes that are mutually exclusive and cover every case, the prices sum to one. Exactly one outcome happens, so the implied probabilities have to add to a whole. Third, logical consistency: if event A forces event B to be true, then A cannot be more likely than B, so its price cannot be higher. "Wins by more than 5 points" implies "wins," so it cannot trade above "wins."

Pass all three and the prices correspond to some genuine probability distribution over the outcomes. Fail any one and the prices are incoherent. The 60-and-50 market fails the second condition, and that failure is not a rounding quirk. It is a guaranteed loss for whoever is on the wrong side, which means a guaranteed profit for whoever notices.

The theorem, stated as a trader would use it

The de Finetti result is short and it is the mathematical definition of arbitrage.

$$ \text{If } p \text{ is not a coherent probability measure, then there exists a portfolio } \delta \in \mathbb{R}^{|\mathcal{I}|} \text{ with } \delta \cdot z > 0 \text{ for every outcome } z. $$

Read it in plain terms. The letter p is the price vector, the list of all the prices. The delta is a portfolio, a list of how many units of each contract you buy (positive) or sell (negative). The dot with z is the profit under a specific outcome. The claim: if the prices are incoherent, some combination of buys and sells profits under every single way the world can end. The converse holds too, and it is the half that keeps you honest. If the prices are coherent, no such portfolio exists. You cannot squeeze a guaranteed profit out of prices that already behave like probabilities, no matter how clever the combination.

Two worked books, because the theorem is only useful when you can build the trade.

The over-round case, prices summing above one. YES at 60, NO at 50, sum $1.10. Sell one YES for 60 cents, sell one NO for 50 cents, take in $1.10. One of them resolves true and you pay the holder a dollar. Profit: $0.10, locked, regardless of outcome.

$$ \text{Revenue} = 0.60 + 0.50 = 1.10, \qquad \text{Payout} = 1.00, \qquad \text{Profit} = 0.10 $$

The under-round case, prices summing below one. YES at 30, NO at 33, sum $0.63. Now you buy instead of sell. Buy one YES for 30, buy one NO for 33, pay out $0.63. Exactly one pays you a dollar. Profit: $0.37.

$$ \text{Cost} = 0.30 + 0.33 = 0.63, \qquad \text{Payout} = 1.00, \qquad \text{Profit} = 0.37 $$

Notice the direction flips with the sign of the error. Prices too high, you sell the overpriced bundle. Prices too low, you buy the underpriced bundle. The theorem does not tell you which; the arithmetic does. And notice what is absent from both trades: any view on the event. This is the cleanest edge in the pillar precisely because it survives being completely wrong about the world.

Why the mispricing does not get competed away

The obvious objection: if this is free money, arbitrage should erase it in seconds and the opportunity should not persist. It persists. A 2024 to 2025 study of Polymarket estimated roughly $40 million of arbitrage profit available over a one-year sample. That is not a market that occasionally slips. That is a market that generates incoherence as a structural byproduct of how it is built. Three reasons, and each one is a design choice the platform cannot easily reverse.

First, the speed-accuracy tradeoff. Enforcing coherence across many linked markets means solving integer programs that are NP-hard, the class of problems with no known fast algorithm. A platform that wants to confirm your order in milliseconds cannot run that solve on every incoming trade. Polymarket runs fast, largely independent books instead, and the $40 million is the price of that speed. The later articles in this pillar, the article "Frank-Wolfe: Solving a Quintillion-Vertex Problem in 100 Steps" and its companions, exist because that same hard solve is what an arbitrageur has to run to find the trade the platform skipped.

Second, independent listing. Each market keeps its own order book and its own liquidity. "A wins State X" and "A wins X by more than 5" sit in separate books with separate flow, and no real-time mechanism reconciles them. The books do not talk to each other, so nothing forces their prices to agree.

Third, human local reasoning. A trader prices one market with the information in front of them. Nobody holds hundreds or thousands of linked markets in their head and checks every implication against every other. The same study identified 46,360 candidate market pairs in the 2024 US election alone. No participant, and no market maker chasing latency, evaluates that many relationships by hand.

$$ \text{Candidate market pairs, 2024 US election} = 46{,}360 $$

Put the three together and the conclusion is not that Polymarket is badly run. It is that any market prioritizing speed and accessibility over global consistency will leak arbitrage continuously, and the leak regenerates as fast as it is captured. Incoherence here is a permanent feature, not a bug someone will patch.

The gap between this and the real world

Two cautions, stated flatly because the arithmetic above is seductive and the losses are real.

The 10 cents in the over-round example is the profit if both legs fill at the quoted prices at the same instant. They will not. On a central limit order book you place the legs one at a time, your first fill moves the price, and the second leg can slip past the point where the trade still works. A textbook Dutch book can turn into a directional bet the moment execution is imperfect. The article "Execution Is Part of Expected Value" is where that leak gets measured, and the short version is that a large fraction of theoretical arbitrage never survives contact with the book.

The second caution is scope. The Dutch book handles the simplest incoherence, prices on exclusive outcomes that fail to sum to one. Real markets are richer than that: one event implying another, mutual exclusions across markets, conditional relationships, whole webs of combinatorial dependency. The 60-and-50 trade is the toy case. The general test is not "do the prices sum to one" but "do the prices lie inside the set of all coherent price vectors," a geometric object called the marginal polytope. That object subsumes the Dutch book as one flat face and covers everything the simple sum-to-one rule misses. The article "The Marginal Polytope: One Shape That Contains Every Fair Price" builds it, and from there the pillar stops checking prices by hand and starts projecting onto the shape.

KEY POINTS

- Prices are coherent when you can read them as probabilities without contradiction: no negatives, exclusive outcomes sum to one, and an implication cannot cost more than the thing it implies. Fail any condition and the prices are incoherent.

- The Dutch book theorem (de Finetti, 1937) says incoherent prices always admit a portfolio that profits under every outcome, and coherent prices never do. That is the mathematical definition of arbitrage, and it needs no forecast.

- Over-round prices (sum above one): sell the bundle. YES 60 plus NO 50 gives $1.10 in, $1.00 out, 10 cents locked. Under-round (sum below one): buy the bundle. YES 30 plus NO 33 costs $0.63, pays $1.00, 37 cents locked. The sign of the error picks the direction.

- The edge persists because of design, not oversight: enforcing coherence is NP-hard and too slow for a low-latency platform, each market is an independent book, and no human tracks the 46,360 linked pairs a single election generates.

- A 2024 to 2025 Polymarket study estimated about $40 million of arbitrage available over a year. Incoherence regenerates as fast as it is captured, so it is a permanent structural feature of any speed-first market.

- The quoted profit assumes both legs fill at once; sequential fills on an order book can erase it. And sum-to-one is only the toy case. The general coherence test is membership in the marginal polytope, which the next articles build.

References

- La prevision: ses lois logiques, ses sources subjectives - de Finetti (1937)

- Foundations of the Theory of Probability - Kolmogorov (1933)

- Arbitrage-Free Combinatorial Market Making via Integer Programming - Kroer et al. (2016)

- Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets - Saguillo et al. (2025)