9.8 The Marginal Polytope: One Shape That Contains Every Fair Price

Every arbitrage question reduces to one: is the price inside the marginal polytope or outside it. Inside means no trade; outside, the wall separating you from the shape is your portfolio.

Every arbitrage-detection question you can ask about a set of prediction markets collapses into one geometric question. Is the price vector inside a certain shape, or outside it. Inside, no structural trade exists and you should stop looking. Outside, a guaranteed-profit portfolio exists and the boundary of the shape hands you the exact trade. The shape has a name, the marginal polytope, and learning to think in it replaces a pile of ad-hoc coherence checks with a single test.

The article "The Dutch Book Theorem, Plainly" handled the toy case, prices that fail to sum to one. That rule misses most of what happens in real markets: implications, mutual exclusions, conditionals, tangled combinatorial dependencies. This article generalizes all of it into one object and one theorem, and it is the intellectual center of the structural half of this pillar.

Building the shape from the valid outcomes

Start where the article "Outcome Geometry" left off, with the valid payoff set, the small collection of ones-and-zeros rows that describe what the contracts pay under each outcome that can actually happen. Those rows are corners. The marginal polytope is the solid shape you get by filling in everything between them.

$$ M = \text{conv}(Z) = \Big\{ \sum_{\omega} \lambda_\omega\, \varphi(\omega) \;:\; \lambda_\omega \ge 0,\; \sum_\omega \lambda_\omega = 1 \Big\} $$

The word conv is convex hull, the smallest shape with no dents that wraps a set of points. The formula spells it out: take the valid payoff vectors phi, weight them with numbers lambda that are all non-negative and sum to one, and add them up. Weights that are non-negative and sum to one are a probability distribution. So every point in M is a weighted blend of valid payoffs, and the weights are a probability over outcomes.

That gives the reading that makes the shape worth caring about. A price vector sits inside M exactly when there is some probability distribution over the outcomes that produces those prices as its implied payout probabilities. Inside M means "these prices are consistent with some coherent view of the world." Outside M means "no probability distribution, however contrived, could ever price things this way." The second case is the mispricing, and it is guaranteed, not a matter of taste.

The characterization theorem, and why the boundary is the trade

One theorem ties membership to arbitrage with no gap between them.

$$ p \text{ is arbitrage-free} \iff p \in M $$

The double arrow is "if and only if." Arbitrage-free is the same statement as inside the polytope. No arbitrage exists precisely when the prices are in the shape, and arbitrage exists precisely when they are out of it. This subsumes the Dutch book: prices failing to sum to one are just one way to fall outside M, the flat face where the sum-to-one constraint lives.

The proof is where the trade comes from, so it is worth walking, not skipping. Suppose the prices are outside M. There is a theorem in convex geometry, the separating hyperplane theorem, that says a point outside a convex shape can always be split off from it by a flat wall. Everything in the shape sits on one side of the wall; the outside point sits on the other.

$$ p \notin M \;\Rightarrow\; \exists\, \delta \text{ such that } \delta \cdot p < \min_{z \in Z}\, \delta \cdot z $$

Read delta as a portfolio again. The left side, delta dot p, is what the portfolio costs at current prices. The right side, the minimum over valid outcomes of delta dot z, is the worst payout that portfolio can ever return. The wall guarantees the cost is strictly below the worst-case payout. You pay less than the least you will ever collect. That is a locked profit, and the direction of the wall is the direction of the trade. The separating hyperplane is not an abstraction. It is the trading strategy, written as a vector.

The other direction is the honesty check. Suppose the prices are inside M. Then they are a probability blend of valid payoffs, and any portfolio's cost is that same blend of the portfolio's payouts across outcomes. A blend sits between the minimum and the maximum of the things blended. So the cost lands between the worst and best payout, and no portfolio can guarantee it collects more than it paid. Inside the shape, the free money is gone.

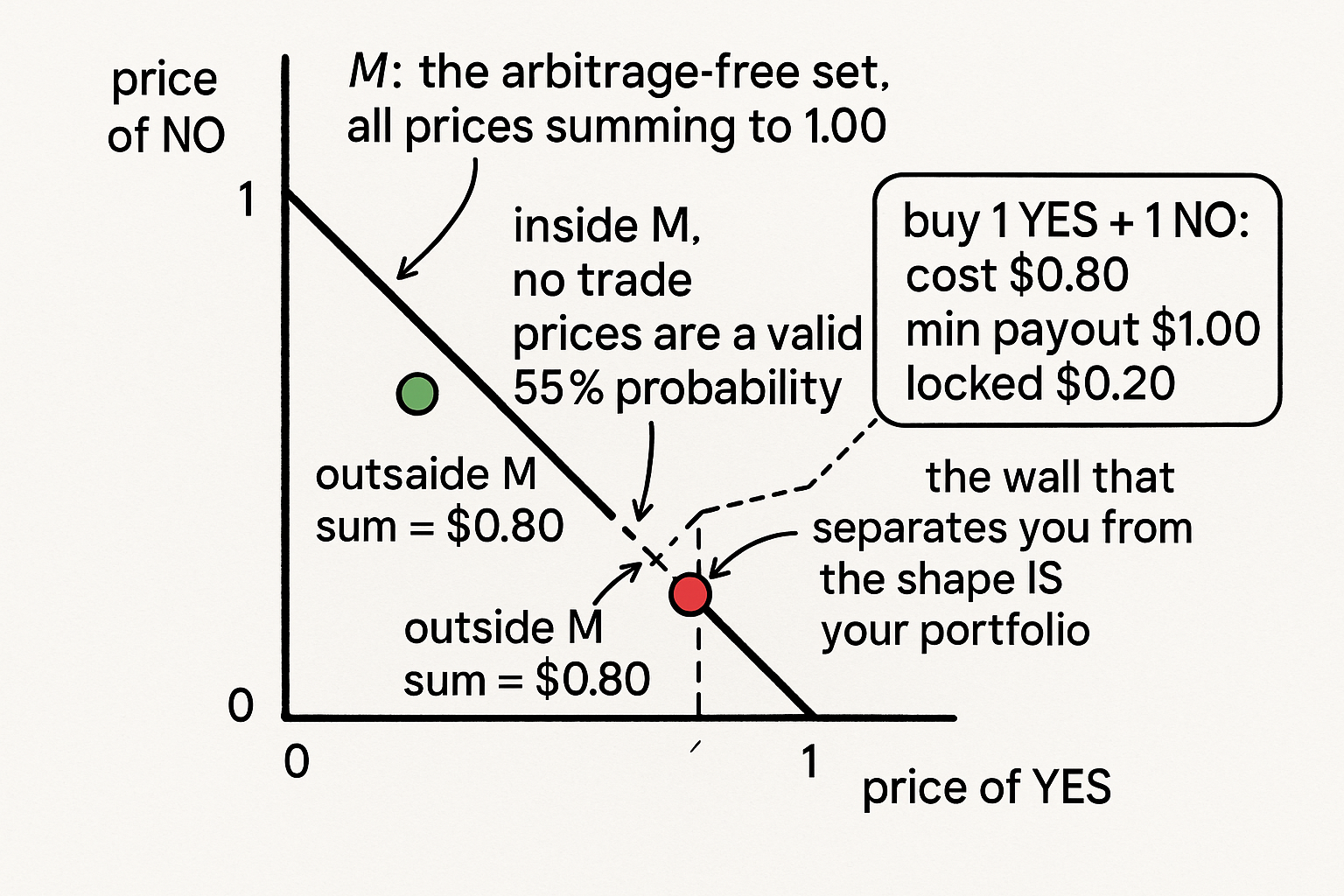

The worked case you can hold in your head

Two securities, YES and NO, on one event. The valid payoffs are (1,0) if YES resolves and (0,1) if NO resolves. Two corners. The convex hull of two points is the line segment between them, and every point on that segment has its coordinates summing to one. So M here is the line "YES price plus NO price equals one." Simple, and it is the whole shape.

Now price the market at (0.40, 0.40). The sum is 0.80, below one, so the point sits below the segment, outside M. The separating wall is the portfolio (1, 1): buy one of each. Cost is 0.40 plus 0.40, which is 0.80. Worst-case payout is the smaller of (1,1) dotted with each corner, which is the smaller of 1 and 1, so 1.00. Cost 0.80, worst payout 1.00, guaranteed profit 20 cents. That is the Dutch book from the previous article, recovered as a point-outside-a-line-segment.

Price it instead at (0.55, 0.45). Sum is 1.00, so the point sits on the segment, inside M. Try to build a winning portfolio and you cannot; every combination that wins if YES resolves loses if NO resolves. The 20 cents is gone because the prices are now consistent with a real probability, namely 55 percent.

Why you cannot just check membership directly

The two-security case fits on a napkin. Real markets do not. The polytope has at most as many corners as there are valid outcomes, and that count is the runaway number from the article "Outcome Geometry."

| Market | Securities | Number of outcomes |

|---|---|---|

| Single binary | 2 | 2 |

| Ten independent binaries | 20 | 1,024 |

| NCAA tournament (63 games) | over 5,000 | about 9.2 quintillion |

Testing membership by listing the corners is hopeless when there are 9.2 quintillion of them. You cannot write down the shape, let alone check whether a point is inside it. This is the wall the rest of the structural pillar spends its time getting around: the article "Trillions of Outcomes, 200 Constraints" describes the shape with a handful of linear rules instead of a list of corners, and the article "Frank-Wolfe: Solving a Quintillion-Vertex Problem in 100 Steps" tests membership and finds the trade by touching only about a hundred of those corners. The polytope is the right object. Enumerating it is not the right method.

The hidden case, and the empirical scale

The dangerous mispricings are not the ones where a single market fails to sum to one. Those are visible. The dangerous ones hide across markets that each look fine. Take Market A, "candidate wins State X," at 0.52 and 0.48, summing to a clean dollar. Take Market B, "wins X by more than 5 points," at 0.32 and 0.68, also a clean dollar. Each is coherent alone. But winning by more than 5 implies winning, so the joint outcome space has three corners, not four, and the joint price vector (0.52, 0.48, 0.32, 0.68) can sit outside the three-corner polytope even though every individual book passes the sum-to-one test.

That is where the money actually was. The 2024 to 2025 Polymarket study found 1,576 logically dependent market pairs in the presidential race, of which 13 were manually confirmed as exploitable for combinatorial arbitrage. Zoom out to single markets and the numbers get larger: across 17,218 conditions examined, 7,051 (41 percent) had single-market arbitrage, with typical mispricing around 60 cents on the dollar of payout. Read that last figure carefully. Buying a dollar of guaranteed payout for roughly 60 cents was a regular occurrence for anyone with the infrastructure to detect it and the speed to act. The edge was real and large. It was also gated behind exactly the computational machinery the next three articles build, which is why 41 percent of conditions being mispriced did not translate into 41 percent of participants making money.

KEY POINTS

- The marginal polytope M is the convex hull of the valid payoff vectors: every point inside it is a probability blend of outcomes, so a price vector is inside M exactly when some coherent view of the world produces those prices.

- The characterization theorem is exact: prices are arbitrage-free if and only if they lie in M. This absorbs the Dutch book as the single flat face where prices sum to one.

- When prices sit outside M, the separating hyperplane theorem gives a wall between the point and the shape, and that wall is the guaranteed-profit portfolio. The geometry hands you the trade, not just a yes/no.

- Worked case: with YES and NO, M is the line "prices sum to one." Prices (0.40, 0.40) sit below it, and the portfolio (1,1) locks 20 cents; prices (0.55, 0.45) sit on it and no winning portfolio exists.

- You cannot test membership by listing corners: an NCAA-scale market has about 9.2 quintillion of them. The polytope is the right object; enumeration is the wrong method, which is why later articles use linear constraints and Frank-Wolfe.

- The costly mispricings hide across markets that each look fair alone. A 2024 to 2025 study found 1,576 dependent pairs in one presidential race and 41 percent of 17,218 conditions carrying single-market arbitrage, typical mispricing near 60 cents on the dollar, all reachable only with the right computational infrastructure.