9.9 Arbitrage Is Just Projection: One Calculation Gives Trade, Profit, and Target Prices

The best arbitrage trade is the closest fair price to the unfair one. One projection returns the trade, the profit, and the target prices at once, measured with KL divergence, not a straight ruler.

The article "The Marginal Polytope" gave you a yes/no test: are the prices inside the arbitrage-free shape or outside it. This article answers the three questions you actually care about once the answer is "outside." What is the best possible trade. How much profit does it guarantee. What should the prices be. All three fall out of a single calculation: find the closest point in the shape to the current prices. That closest-point operation is a projection, and the entire structural edge in this pillar reduces to it. This is the keystone. Every earlier article is a prerequisite for it and every later article implements or defends it.

From "best trade" to "closest point"

Set up the problem the way a trader would. You hold a portfolio, call it delta, where a positive entry buys a contract and a negative entry sells it. The market maker charges you for the trade through a cost function. Against that, the worst-case payout is the least the portfolio collects across all outcomes. Guaranteed profit is worst-case payout minus what you paid.

$$ \Pi(\delta) = \min_{z \in Z}\, \delta \cdot z \;-\; \big[\, C(\theta + \delta) - C(\theta) \,\big] $$

The first term is the worst payout, the minimum over valid outcomes z of the portfolio's payout. The bracket is the cost of moving the market state from theta to theta plus delta, where C is the market maker's cost function. If that difference is positive under every outcome, you have risk-free profit. The best trade maximizes it, and the structure is a fight: you pick the portfolio to maximize, nature picks the worst outcome to minimize.

$$ \max_{\delta}\; \min_{z \in Z}\; \big[\, \delta \cdot z - C(\theta + \delta) + C(\theta) \,\big] $$

You choose delta. Nature, seeing your choice, chooses the outcome that hurts you most. You want the portfolio that still profits after nature does its worst. A min-max fight like this looks intractable, because your best move depends on nature's response, which depends on your move. Convex duality cuts the knot.

The duality swap, and why it turns into a projection

Strong duality is a result that lets you swap the order of the min and the max without changing the answer. On the left, "pick the best portfolio, assuming nature picks the worst outcome." On the right, "pick the closest fair-price vector, then find the best portfolio for that target." Same number, different problem, and the right-hand version is one you can solve.

$$ \max_{\delta}\, \min_{p \in M} \big[\cdots\big] \;=\; \min_{p \in M}\, \max_{\delta} \big[\cdots\big] $$

Work the inner maximization over delta with a target price p held fixed. Setting the gradient to zero gives the trade that moves the market to that target, and the profit from it turns out to equal a specific distance between the target and the current state. The distance is the Bregman divergence, and after the dust settles the whole min-max reduces to this.

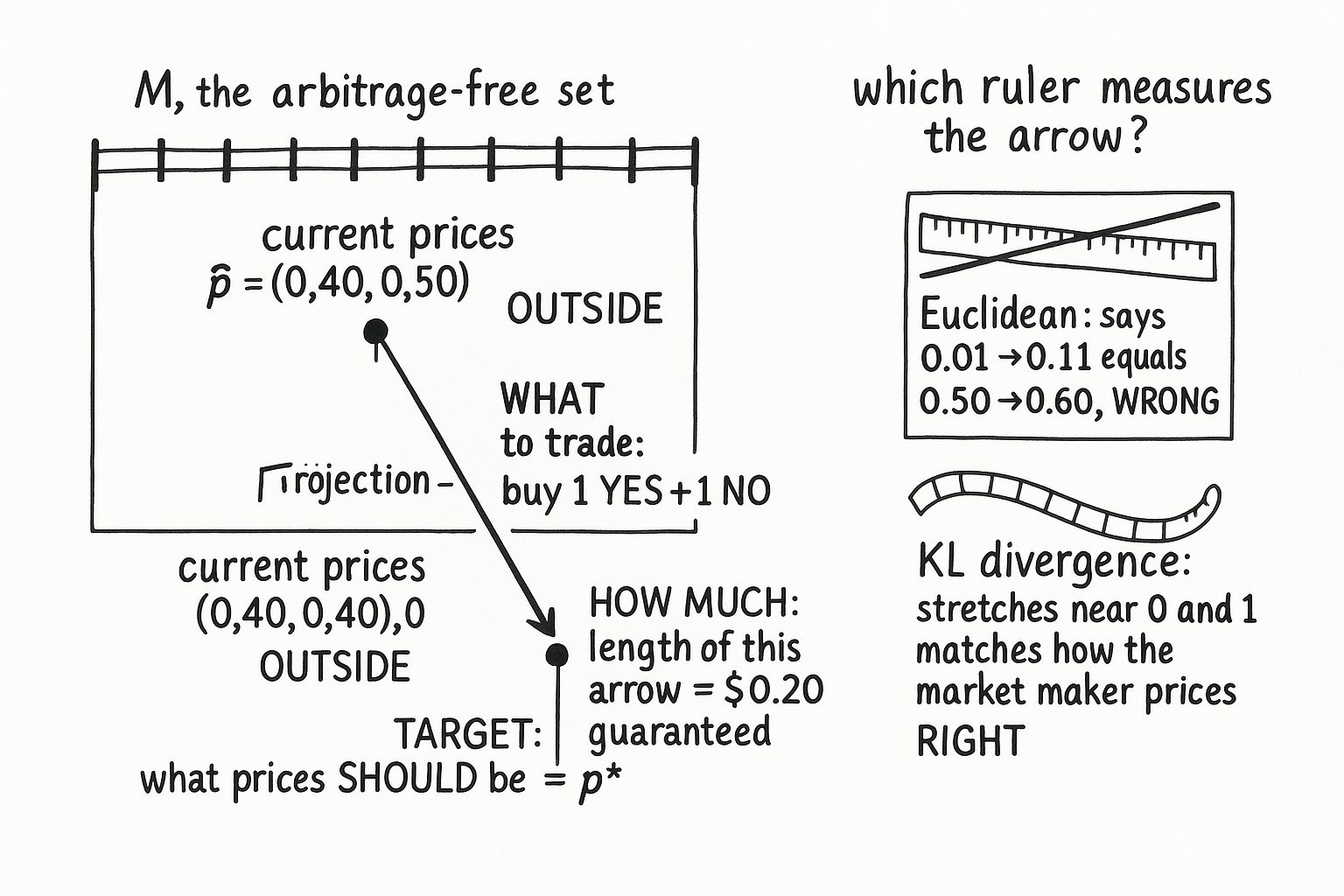

$$ \Pi^* = \min_{p \in M}\, D(p \,\|\, \theta) = D(p^* \,\|\, \theta), \qquad p^* = \arg\min_{p \in M} D(p \,\|\, \theta) $$

Read it slowly. D is a distance, the Bregman divergence, measuring how far a candidate fair price p is from the current market state theta. You minimize that distance over all fair prices p in the polytope M. The minimizing point p-star is the projection of the current state onto the arbitrage-free set, the closest legal price to the illegal one you observe. And the punchline: the maximum guaranteed profit equals that minimum distance. Closer prices, less profit. Prices already inside M, distance zero, no arbitrage. The best trade and the best profit are the same object seen two ways.

One projection, three answers

The projection does not give you a number. It gives you the complete trade.

$$ \text{Trade: } \delta^* = \nabla C^*(p^*) - \theta, \qquad \text{Profit: } D(p^* \,\|\, \theta), \qquad \text{Target: } p^* $$

First, what to trade: the portfolio delta-star that moves the state to the projected price. The gradient of the conjugate function C-star maps a target price back to the market state that produces it, an inverse lookup, and the trade is the difference between that state and where the market is now. Second, how much: the divergence, the distance you projected across, is the guaranteed profit in dollars. Third, where prices should be: p-star itself is what a coherent market would show. If the projection lands exactly on the current prices, the distance is zero and there is nothing to do. One calculation, three outputs, no separate steps for detection, sizing, and pricing.

A concrete anchor. Binary market, YES at 40 cents and NO at 40 cents, summing to 80. The arbitrage-free set requires the sum to be one. Project the (0.40, 0.40) point onto that line and you land at (0.50, 0.50). The distance you crossed is the profit: buy both for 80 cents total, collect a dollar at resolution, keep 20 cents. The projection produced the trade (buy one of each) and the profit (20 cents) in the same motion.

Why the distance is not a ruler you'd expect

The obvious way to measure "closest" is straight-line distance, the Euclidean one. It is wrong here, and the reason matters because using the wrong ruler produces the wrong trade.

Prices in these markets are probabilities, and probabilities do not move on a linear scale. A shift from 1 percent to 11 percent is an enormous change in what the market believes; in log-odds it moves roughly from minus 4.6 to minus 2.1. A shift from 50 percent to 60 percent is a small change; in log-odds, from 0 to about 0.4. Straight-line distance calls both of them the same 10-cent move. They are not the same, and a trade sized as if they were will misprice the tails badly.

The right ruler for a log-scoring market maker is the Kullback-Leibler divergence, which measures distance in the same information units the market maker itself uses.

$$ D(p \,\|\, \theta) = \sum_i \mu_i \ln \frac{\mu_i}{p_i(\theta)} $$

The sum runs over securities. Each term weights the log-ratio of the target probability to the current implied probability. Near the boundaries, where prices approach 0 or 1, this ruler stretches, so a 10-cent move at the extremes counts for far more than a 10-cent move in the middle. That is the correct accounting, because that is how the market maker prices risk. Measure with KL and you get the optimal trade. Measure with Euclidean distance and you leave money on the table or overtrade the tails. The stretching near the boundaries also causes a numerical problem that the article "Why Your Arbitrage Solver Crashes at 99 Cents" is entirely about, so file that away.

The guarantee is real, but it leaks

Two honesty checks, because the word "guaranteed" invites carelessness.

First, you will not compute the exact projection in practice. The article "Frank-Wolfe: Solving a Quintillion-Vertex Problem in 100 Steps" returns an approximate projection with a measured gap between where it stopped and the true optimum. The profit you can count on is the approximate distance minus that gap.

$$ \Pi \;\ge\; D(\hat{p} \,\|\, \theta) - g(\hat{p}) \;\ge\; 0 $$

The first distance is the profit you'd get if the approximation were exact. The gap g is what you are leaving on the table by stopping early. The difference is what you keep no matter what, and convex duality guarantees it is never negative. An approximate solution can capture less than the maximum, but it never manufactures a fake profit that turns into a loss. That property is what makes stopping early safe.

Which sets up the second check: when to stop and trade. Three rules. Alpha-extraction: stop when the gap is small enough that you have captured at least 90 percent of the available profit, because chasing the last 10 percent costs time and the market moves. Near-free: if the whole guaranteed profit is under 5 cents, do not trade at all, because execution risk and fees will eat it. Forced stop: a time limit or an incoming order forces you out with the best iterate you have. The 5-cent floor is not a rounding convenience. It is the line below which the theoretical guarantee stops surviving the real costs cataloged in the article "Execution Is Part of Expected Value."

The reason the discipline matters shows up in the data. The top account in the 2024 to 2025 Polymarket study cleared $2,009,631 across 4,049 trades at a win rate above 90 percent. A 90-plus percent win rate is what this machinery produces when you only pull the trigger on a large, established profit guarantee and skip everything below the floor. It is not a forecasting record. It is the signature of a projection that refused to trade the marginal cases.

KEY POINTS

- The best arbitrage trade is the projection of the current market state onto the arbitrage-free set: find the closest legal price to the illegal one you observe. Maximum guaranteed profit equals the distance you project across.

- A min-max fight (you pick the portfolio, nature picks the worst outcome) becomes a solvable projection through strong duality, which swaps the order of min and max without changing the answer.

- One projection returns three things at once: the trade (the portfolio that moves the state to the projected price), the profit (the divergence in dollars), and the target prices (what a coherent market would show). Distance zero means no arbitrage.

- Measure distance with KL divergence, not straight-line distance. Probabilities move on a log scale, so a move from 0.01 to 0.11 dwarfs a move from 0.50 to 0.60; the KL ruler stretches near the boundaries to match how the market maker prices, and Euclidean distance gives the wrong trade.

- The guarantee survives approximation: guaranteed profit is the approximate distance minus the solver gap, and convex duality keeps that quantity non-negative, so stopping early never fabricates a loss.

- Stop on three rules: capture at least 90 percent of the profit, skip anything under a 5-cent guarantee, and bail out on a time limit or incoming order. The 90-plus percent win rate of the top real account is what this discipline looks like, not a forecasting skill.

References

- Arbitrage-Free Combinatorial Market Making via Integer Programming - Kroer et al. (2016)

- An Optimization-Based Framework for Automated Market-Making - Abernethy et al. (2011)

- Logarithmic Market Scoring Rules for Modular Combinatorial Information Aggregation - Hanson (2007)

- Convex Optimization - Boyd and Vandenberghe (2004)