9.39 The DePM Design Space: An 8-Stage Microstructure Map

Decentralized prediction markets, cut into eight swappable stages. Seven are engineering trade-offs. The eighth, resolution, is where a handful of token wallets can settle a market against the truth.

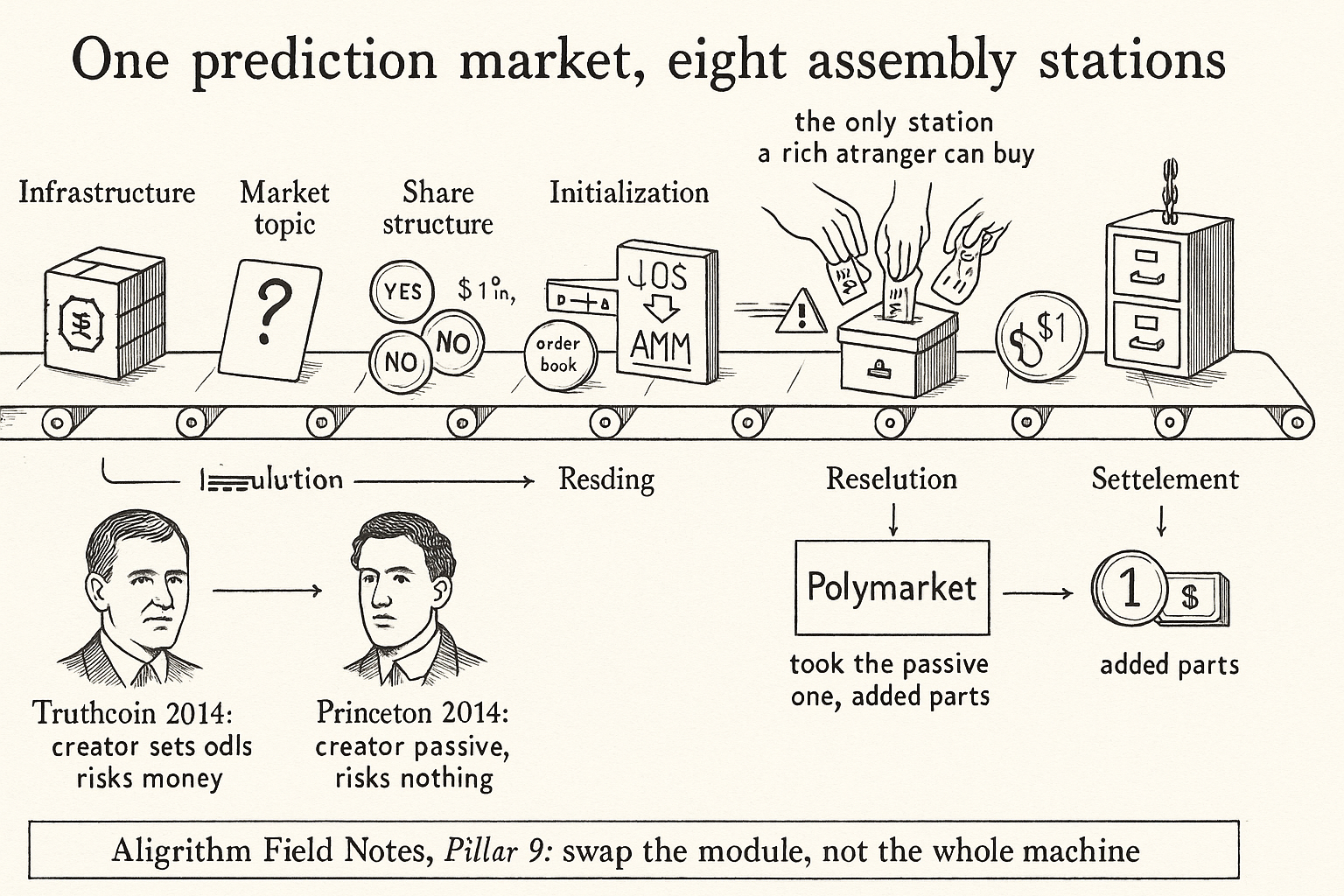

Polymarket looks like the obvious way to build a prediction market on a blockchain. It is not. Rahman, Al-Chami, and Clark went back through the history of decentralized prediction markets, which starts in 2011 and runs to hundreds of proposals, distilled the field down to 35-plus notable systems, and showed that the design everyone now copies bucked the trend rather than following it. The two founding blueprints, both from 2014, point in opposite directions: Truthcoin, where the market creator sets the odds and risks its own money, and the Princeton academic paper, where the creator is passive and risks nothing. Polymarket picked the passive one, then bolted on pieces neither original design had.

To compare systems that disagree on almost everything, the authors do what the old article "Separate Detection from Execution: A Three-Layer, Typed-Agent Architecture" did for a trading bot: they refuse to argue about whole systems and instead cut the machine into modules you can swap and reason about one at a time. Their cut is an eight-stage workflow: underlying infrastructure, market topic, share structure and pricing, initialization, trading, resolution, settlement, and archiving. This article walks that map, pulls out the math that makes a prediction market solvent by construction, and lands on the one stage that is genuinely dangerous.

The eight stages, side by side

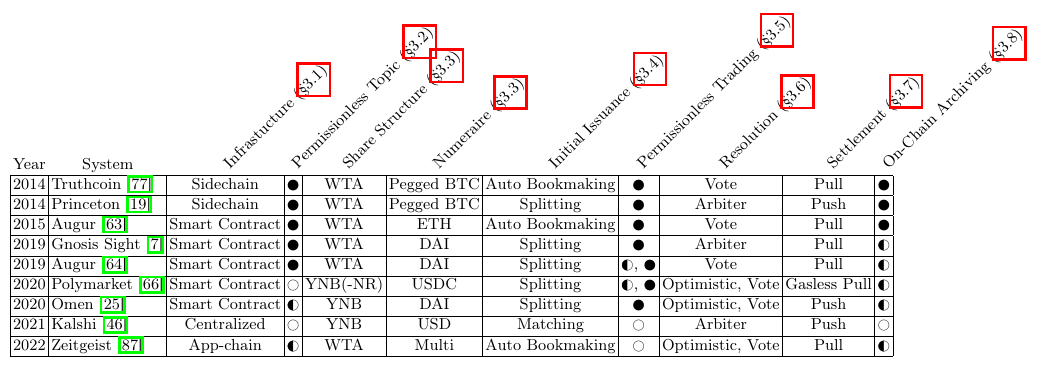

The payoff of a modular workflow is a single table where systems that look nothing alike line up column by column. Read across a row and you get a system's full design; read down a column and you see the menu of choices for one stage.

The table is the argument. Truthcoin and Augur v1 sit on the left with sidechains, winner-take-all shares, automated bookmaking, and reputation-token voting. Polymarket sits apart: a smart contract on Polygon, a negative-risk yes-no share structure, USDC as the numeraire, splitting for initialization, an optimistic vote only when a market is disputed, and gasless push settlement. No single row is the "best" design. Each column is a trade-off between decentralization, expressiveness, and resistance to manipulation, and the authors spend the paper naming those trade-offs and marking ten open research gaps where nobody has a good answer yet.

What a prediction market actually is

Before the design choices, the paper pins down what all these systems have in common with a definition sparse enough to cover every variant. A single market is a tuple of three objects.

$$ M = (\Omega,\; J,\; R) $$

Omega is the outcome space, the set of ways the event can resolve. J is the finite set of contract labels, the shares you can hold. R is the payoff map: it says how many units of the numeraire one unit of share j pays when the world lands on outcome omega. Take the HBO Satoshi documentary market. Omega is the list of people the film might name, J is one share per name plus an "other or multiple" share, and R pays $1 to the share matching whoever the film actually named and $0 to the rest. When Omega is a set of mutually exclusive names and each share pays either 0 or 1 with exactly one winner, you have the winner-take-all special case, the Arrow-Debreu market that most people picture when they think "prediction market."

The load-bearing property is not the payoff, it is the collateral behind it. A bookmaker quotes odds and promises to pay; it does not have to hold the money. A prediction market must hold enough to cover every outcome at all times, starting from the very first trade. The paper writes this as a solvency invariant.

$$ L(S) = \sup_{\omega \in \Omega} \sum_{j \in J} S_j \, R(\omega)_j \qquad\text{and}\qquad \mathrm{Treas} \geq L(S) $$

S is the vector of how many of each share are outstanding. L(S) is the worst-case liability: for each possible outcome you total up what you would owe, then take the largest such total across all outcomes. The treasury must always sit at or above that worst case. Work it: a three-outcome winner-take-all market with 100 shares outstanding of each label owes at most 100 times $1 in every outcome, because only one label wins, so L(S) is $100 and the treasury has to hold at least $100. Any operation that mints more shares has to top the treasury up by at least the increase in worst-case liability. The old article "The Market Maker's Impossibility: Speed Versus Accuracy, and Why Arbitrage Is Tolerated" described why a maker cannot both quote fast and quote right; this invariant is the flip side, the reason a prediction market never has to fight a winning ticket. It is collateralized to pay by construction, so it is financially indifferent to who wins.

Share structures: four ways to slice a bet

The stage with the most quiet consequence is how you structure the shares. The paper lays out three main types and a variant, and the choice determines what markets you can even express.

Winner-take-all issues one share per outcome, and the shares are built to be mutually exclusive and complete, so exactly one pays $1. That is why holding one of every share equals holding $1, the fact the whole splitting mechanism runs on. The prices work as probabilities: if the "A wins" share trades at $0.54, the market implies a 54% chance. The tidy claim that the prices sum to $1.00 is imprecise, though. Shares have a bid and an ask, and the honest statement is that the sum of bids and the sum of asks straddle $1.00, with a spread that can be wide. A single displayed "price," like the last trade or the bid-ask midpoint, need not sum to a dollar across outcomes. That is not a broken market, just a misread screen.

Yes-no bundles issue two shares per outcome, a yes and a no, so each outcome is its own little binary market. This buys flexibility: multiple outcomes can resolve yes, or none can, which is exactly what you want for a market on which words Trump will say in a speech. New outcomes can be added mid-life because the bundle does not have to be complete up front. Polymarket runs a disciplined variant called negative risk, where the yes shares are forced to be complete and mutually exclusive after all, so both a per-outcome constraint and a market-wide one hold.

$$ \sum_{k \in \Omega} R(\omega)_{j_{k_Y}} = 1 \qquad\text{and}\qquad \sum_{k \in \Omega} R(\omega)_{j_{k_N}} = |\Omega| - 1 $$

The yes shares sum to $1, the no shares sum to the number of outcomes minus one. In the six-way HBO market, one "yes" wins and pays $1, while five of the six "no" shares win, so the no shares pay $5 in total, which is the six outcomes minus one. The practical consequence is a conversion gadget: holding a "no" on Hal Finney pays exactly the same as holding a "yes" on every other candidate at once, so a trader can swap a single no share for a portfolio of yes shares and back. That gadget is what quietly aligns yes and no prices and hands arbitrageurs a low-friction way to erase inconsistencies, the same inconsistencies measured at roughly $40M in the combinatorial-arbitrage study.

The fourth type is scalar, where the payout tracks a quantity like a vote share or a temperature, normalized to a 0-to-1 range. Polymarket mostly cheats here, chopping the quantity into buckets and running a yes-no market per bucket. That unifies the interface but creates its own trap: if your forecast of the popular vote straddles two buckets, you have to buy both and dilute your return, and the market jumps hard when consensus crosses a bucket boundary.

Initialization: someone has to be the first counterparty

The stage the authors call the biggest evolution from Truthcoin to Polymarket is initialization, the question of how the very first trade happens when there is nobody on the other side yet. There are three answers, and they trade the same thing the old article "Fast Fills Are Bad Fills: Make vs Take, Adverse Selection, and Why the Spread Is Posterior Variance" worried about: who takes the risk of being first.

Automated bookmaking posts a loss fund and an algorithmic price rule, originally Hanson's logarithmic market scoring rule, so the first trader trades against the operator's money instantly. The operator is the counterparty, which means it can lose, and it carries the burden of setting the opening odds well. Splitting takes the opposite stance: a trader pays $1, receives one share of every outcome, and lists some for sale, so the operator posts zero risk but the first trader has to wait for a second trader to show up. Matching, the third route, mirrors a futures exchange, escrowing each side's maximum loss and minting shares only when a buyer and seller coincide on price and size.

The clean way to see the tension is the paper's insight: if the first trader is going to be able to make a dollar, someone has to be able to lose a dollar, and that someone is either the operator or a later trader. You cannot have instant liquidity and zero operator risk at the same time. Splitting picks zero risk and pays for it with a waiting first trader. Automated bookmaking picks instant liquidity and pays for it with a loss fund. That is the whole design decision, stated in one sentence.

Trading: make and take, on a chain that watches you

Once shares exist, they trade like any blockchain token, and here the old make-take question from centralized order books changes shape. A fully on-chain order book is too expensive to run at scale, so the market maker's world splits three ways: centralized exchanges that custody tokens and run a limit order book, partially decentralized designs like Polymarket that match off-chain but settle on-chain, and fully on-chain automated market makers.

Automated market makers were born out of prediction-market research, but they fit prediction shares badly. A share price is trapped between $0 and $1, it can snap to either end the instant an event resolves, and once resolved it is frozen there forever. When news breaks, an automated market maker gets drained faster than its liquidity providers can pull out, so the maker eats the loss that the old article "The Market Maker's Impossibility: Speed Versus Accuracy, and Why Arbitrage Is Tolerated" said was unavoidable. On-chain trading adds a second tax the centralized world does not have: miners and bots can see your order and front-run it, the maximal-extractable-value problem. The mitigation the Princeton paper proposed back in 2014, before the acronym existed, is the frequent batch auction, which collects orders over a short window and clears them at one uniform price so there is no ordering left to exploit. The whole make-take story you know from a normal exchange still runs here, but every quote is now public, front-runnable, and settled by a chain.

Resolution: the stage that can be bought

Seven of the eight stages are engineering trade-offs. Resolution is where a decentralized prediction market can be attacked outright, because deciding who won is a uniquely decentralized problem: a centralized platform just rules on its own markets, while a decentralized one has to source a truth nobody controls. Polymarket escalates disputed markets to UMA's data verification mechanism, where token holders vote and the majority is paid while dissenters can be slashed.

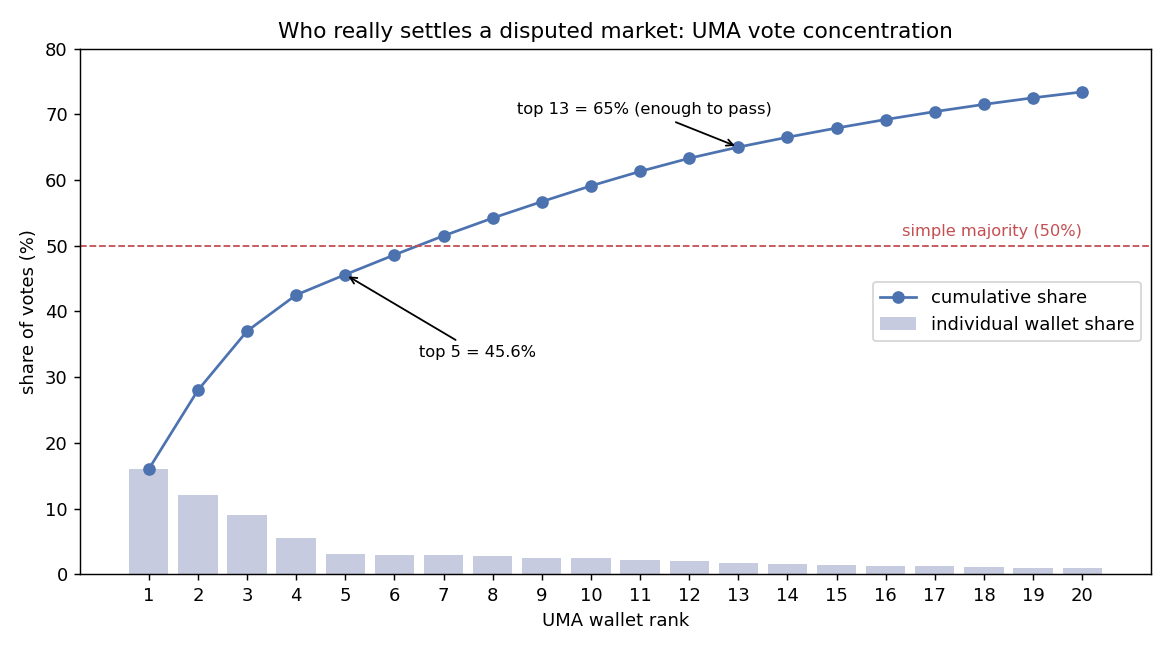

The failure mode is a Keynesian beauty contest. A rational voter is paid for matching the majority, not for reporting the truth, so the system only works when the truth is an obvious focal point everyone expects everyone else to pick. Break that, and voters start guessing what the whales will do. And the whales are concentrated.

At the time of the paper, the top five UMA wallets controlled 45.6% of the votes and the top thirteen exceeded 65%, enough to clear the passing threshold on their own. A market on whether Ukraine agreed to a mineral deal was resolved in a way that raised exactly this alarm: large holders staking early on an outcome can scare honest voters away from the truth, and if a successful attack pushes the token price down, the next attack is cheaper, which is a spiral. This is the concrete reason the "wisdom of the crowd" that a prediction market advertises has a soft spot: the crowd priced the event, but a small committee of token holders decides whether that price pays out. Settlement itself is the easy part after that, a winning share redeems for $1 of stablecoin, and the operator, being collateralized by construction, has no reason to stall the way a bookmaker does.

Where this connects

This SoK is the map that the earlier Pillar 9 pieces were drawing freehand. The old article "Separate Detection from Execution: A Three-Layer, Typed-Agent Architecture" argued for splitting a system into modules you can reason about alone; the eight-stage workflow is that same instinct applied to the market itself, and it lets you say precisely where two platforms differ instead of waving at "Polymarket versus Augur." The old article "Fast Fills Are Bad Fills: Make vs Take, Adverse Selection, and Why the Spread Is Posterior Variance" lives inside the trading and initialization stages, now with the blockchain twist that a full order book is too costly on-chain and every quote is front-runnable. The old article "The Market Maker's Impossibility: Speed Versus Accuracy, and Why Arbitrage Is Tolerated" is the solvency invariant read from the other side: the market is built to pay, so arbitrage and divergence loss are the tax the design accepts rather than a bug it fixes. The one thing the map makes unavoidable is that the danger is not in the pricing math. It is in resolution, where a handful of token wallets, not the crowd, get the last word on what the price meant.

KEY POINTS

- Decentralized prediction markets go back to 2011 and number in the hundreds; the paper distills 35-plus notable systems into one eight-stage workflow: infrastructure, topic, share structure and pricing, initialization, trading, resolution, settlement, archiving.

- Polymarket did not follow the original blueprints. It took the passive-creator Princeton design over the odds-setting Truthcoin design, then added negative-risk shares, USDC, splitting, and an optimistic oracle.

- A market is the tuple (Omega, J, R): outcome space, share labels, and a payoff map. The winner-take-all case pays $1 to one share and $0 to the rest.

- Solvency is built in: the treasury must always cover the worst-case liability, the largest total payout across all outcomes, so a prediction market never has to fight a winning ticket the way a bookmaker does.

- Share structure sets expressiveness: winner-take-all, yes-no bundles, Polymarket's negative-risk variant where yes shares sum to $1 and no shares sum to the outcome count minus one, and rarely-used scalar markets that Polymarket fakes with buckets.

- Initialization forces a choice: instant liquidity with operator risk (automated bookmaking) or zero operator risk with a waiting first trader (splitting). If the first trader can win a dollar, someone else must be able to lose one.

- On-chain trading makes a full order book too expensive, exposes every quote to front-running (MEV), and drains automated market makers when news hits; frequent batch auctions are the standing mitigation.

- Resolution is the attackable stage. UMA's vote is a Keynesian beauty contest, and with the top five wallets at 45.6% and the top thirteen above 65%, a small set of holders can settle a disputed market against the truth.

References

- Prediction Markets (Wolfers and Zitzewitz, 2004)

- Logarithmic Market Scoring Rules for Modular Combinatorial Information Aggregation (Hanson, 2007)

- Efficient Market Making via Convex Optimization, and a Connection to Online Learning (Abernethy, Chen, and Vaughan, 2013)

- On Decentralizing Prediction Markets and Order Books (Clark, Bonneau, Felten, Kroll, Miller, and Narayanan, 2014)

- The High-Frequency Trading Arms Race: Frequent Batch Auctions as a Market Design Response (Budish, Cramton, and Shim, 2015)

- Flash Boys 2.0: Frontrunning, Transaction Reordering, and Consensus Instability in Decentralized Exchanges (Daian et al., 2020)

- Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets (Saguillo, Ghafouri, Kiffer, and Suarez-Tangil, 2025)

- SoK: Market Microstructure for Decentralized Prediction Markets, DePMs (Rahman, Al-Chami, and Clark, 2025)

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.