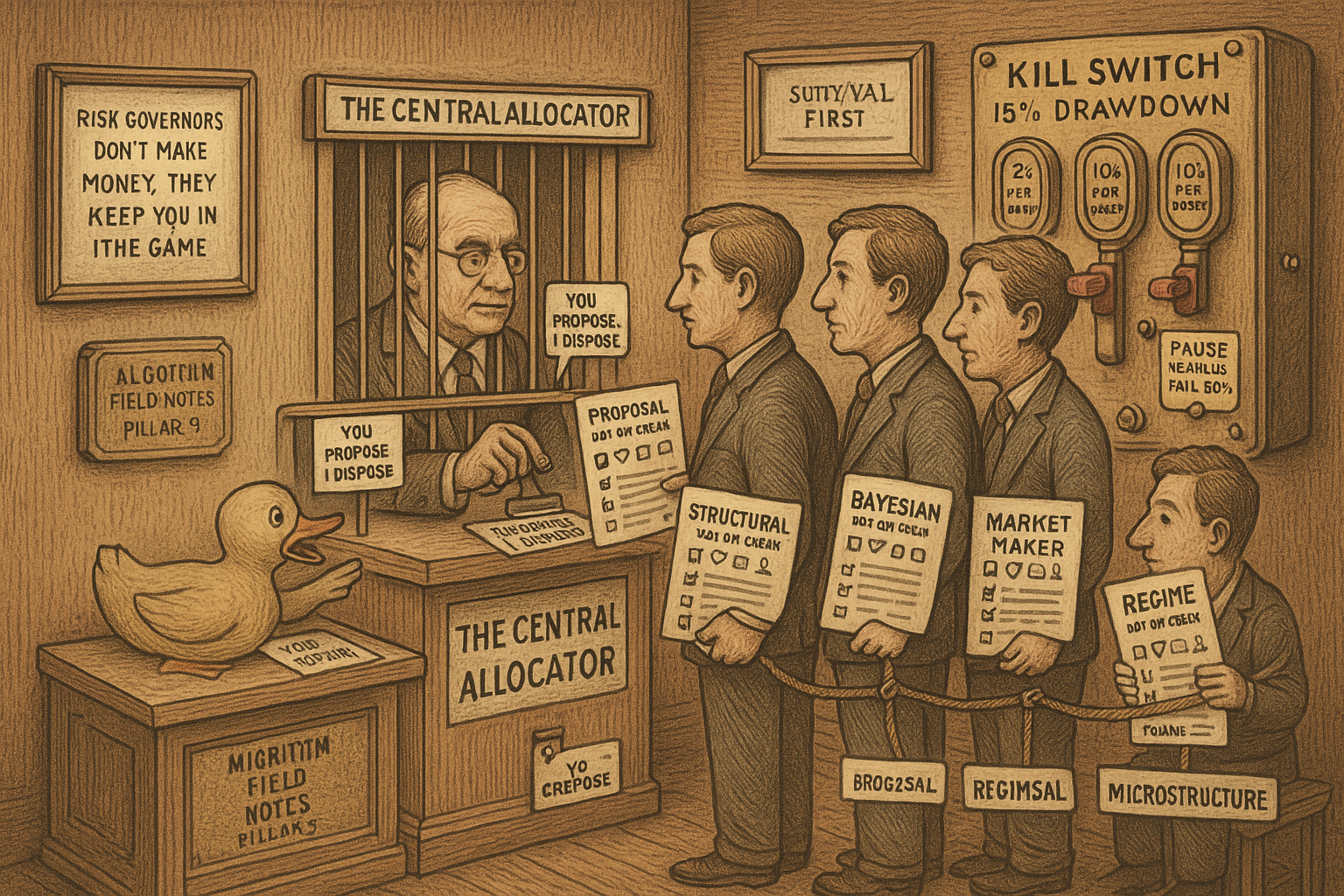

9.22 The Central Allocator and Non-Negotiable Risk Governors: Proposals, Not Orders

Let five agents touch the wallet and they overspend, stack correlated risk, and breach the tail budget. A single allocator funds proposals by one optimization, and hard risk governors override it to keep you solvent.

Give five agents direct access to the wallet and they will each size their trade as if the other four do not exist. The structural solver wants 4 percent on a clean arb, the Bayesian agent wants 3 percent on a directional bet, the market maker wants inventory on six books, and none of them can see that three of those positions are the same election wearing different jerseys. Each is individually reasonable. Together they blow the capital budget, stack correlated exposure, and breach the tail-risk limit nobody was watching. The fix is a rule of authority: agents do not spend money. They ask. A single allocator holds the wallet and decides who gets funded, at what size, subject to every constraint at once.

This is the operational half of the architecture from "Separate Detection from Execution: A Three-Layer, Typed-Agent Architecture." That article said agents emit proposals across a narrow interface. This one is what sits on the other side of the interface, reading every proposal, solving one optimization, and enforcing the limits that keep a good week from turning into a blown account.

Proposals, not orders

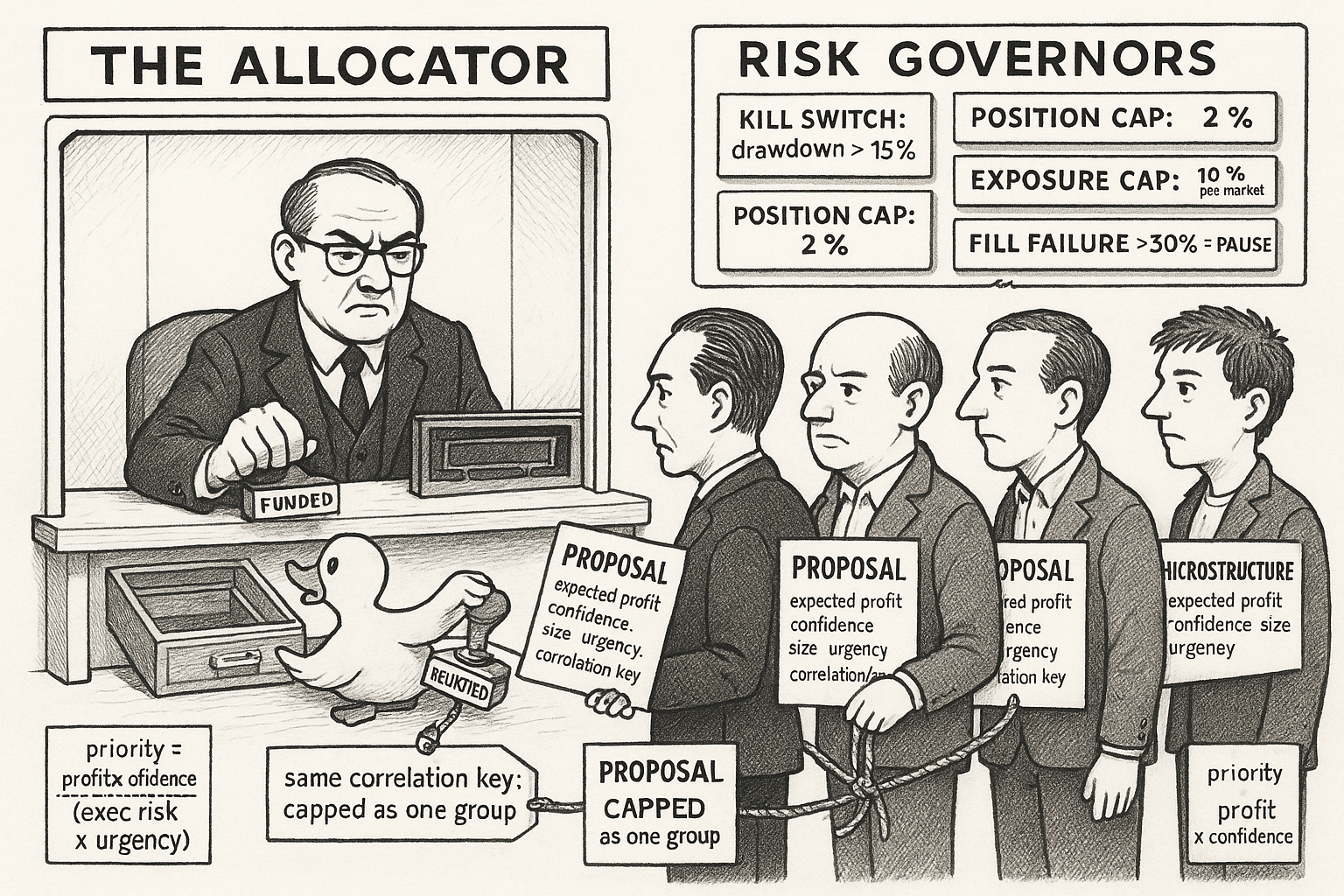

An agent does not send an order. It sends a proposal, a structured request for capital that carries everything the allocator needs to rank and size it. Eight fields.

The strategy tag, so the allocator knows the edge source. Expected profit and confidence, the two numbers that drive the objective. Requested size and minimum viable size, because some trades are worthless below a threshold, a combinatorial arb that needs all legs or none. Execution risk, the probability this fills cleanly. Urgency, how fast the opportunity decays, so a structural arb dying in one block outranks a directional bet good for hours. And a correlation key, the field that groups proposals sharing a hidden risk factor so the allocator can cap them together.

The allocator is the sole authority over capital. Agents propose; it disposes. That single rule is what lets you reason about total risk at all, because there is exactly one place where every position is visible at once.

One optimization funds the book

Each cycle, the allocator solves a constrained optimization: pick the sizes that maximize confidence-weighted expected profit without breaking any limit.

$$ \max_{\{s_i\}} \; \sum_i s_i \cdot \pi_{\text{exp},i} \cdot \gamma_i \quad \text{subject to} \quad \begin{cases} \sum_i s_i \le W_{\text{available}} \\[2pt] s_i \le s_{\text{req},i} \\[2pt] s_i \ge s_{\text{min},i} \;\text{ or }\; s_i = 0 \\[2pt] \sum_{i \in \text{group}(\kappa)} s_i \le E_{\max}(\kappa) \\[2pt] \mathrm{CVaR}(\text{portfolio} + \text{new}) \le C_{\max} \end{cases} $$

Read the objective as: choose each trade's size so the total of size times expected profit times confidence is as large as possible. Then read the constraints top to bottom, each one a way the naive per-agent sizing kills you. Total size cannot exceed available capital. No trade gets more than it asked for. Each trade is funded at or above its minimum viable size, or not at all, which is the min-size-or-zero rule. Everything sharing a correlation key is capped as a group, so five state-election arbs cannot each look small while jointly betting the whole account on one national shock. And the tail-risk measure of the whole book, including the new trades, stays under budget.

That third constraint, size at least the minimum or exactly zero, is what makes this a mixed-integer program rather than a smooth one, because it forces a discrete yes-or-no on each trade. With a moderate number of proposals it still solves in milliseconds. The correlation-group cap and the tail-risk constraint are where this connects to "Kelly Isn't Enough: Drawdown- and CVaR-Constrained Sizing and the Portfolio QP." The tail-risk term here is the CVaR from that article, and the correlation key is the operational form of the tail-dependence lesson from "Correlation Lies, Tail Dependence Tells the Truth," because grouping by a shared risk factor is how you stop the allocator from funding five trades it wrongly believes are independent.

When capital runs short and not every good proposal can be funded, rank them by priority.

$$ \text{Priority}_i = \frac{\pi_{\text{exp},i} \times \gamma_i}{\rho_{\text{exec},i} \times \left(1 + \tau_i^{-1}\right)} $$

Read that as: priority rises with expected profit and confidence, and falls with execution risk and with how long you can afford to wait. The urgency term in the denominator, one over tau, means a fast-decaying opportunity gets pushed up the queue, because a slow one can wait for the next cycle. Fund highest priority first until the capital or a risk limit binds.

Conflicts resolve by rule, not by argument

Two agents will collide, and the allocator settles it mechanically.

| Conflict | Resolution |

|---|---|

| Same market, opposite directions | Net the positions |

| Capital competition | Fund higher priority first |

| Risk limit reached | Cut size to a compliant level, or reject |

Same market opposite directions net out, so you are not paying spread twice to hold offsetting bets. Capital competition goes to priority. A binding risk limit shrinks the trade to fit or drops it. No discretion, no override, no agent lobbying for special treatment.

Risk governors are non-negotiable

The optimization maximizes profit. The governors below do not care about profit at all. They exist to keep you alive, and they override everything.

The kill switch halts all trading if portfolio drawdown passes 15 percent. The position cap forbids any single trade above 2 percent of capital. The exposure cap forbids any single market above 10 percent of capital. The failure-rate monitor pauses trading and forces a diagnosis if execution failures exceed 30 percent, because a system missing a third of its fills is broken in a way more capital will not fix. The solver-timeout monitor shrinks the opportunity window when integer-programming solves start timing out, so you stop chasing problems you cannot compute in time.

These do not increase returns. They dramatically improve survival, and survival is the whole game. This is the same message as the old article "Why Loss Control Is the Only Thing You Fully Control," that you cannot control the edge but you can control the size and the stop, and it is the operational core of the old article "When to Switch Off a Trading System," which is exactly what a kill switch automates. Operational discipline is the ninth source of edge in "The Nine Sources of Edge, Ranked Cleanest to Dirtiest," ranked last not because it makes money but because skipping it eventually loses all of it. The governors are that edge, written as code that cannot be argued with at 3 a.m. during a drawdown.

KEY POINTS

- Agents propose, they do not execute. A single allocator holds the wallet, which is the only way to reason about total risk, because it is the one place every position is visible at once.

- A proposal is eight fields: strategy tag, expected profit, confidence, requested size, minimum viable size, execution risk, urgency, and a correlation key for grouping shared risk.

- The allocator maximizes confidence-weighted expected profit subject to five constraints: total capital, per-trade requested cap, min-size-or-zero, per-correlation-group exposure cap, and a portfolio CVaR tail-risk budget. The min-or-zero rule makes it a mixed-integer program that still solves in milliseconds.

- The correlation-key cap is the operational form of tail dependence: it stops the allocator from funding five trades it wrongly believes are independent. The CVaR term is the same tail-risk budget from the portfolio-QP article.

- Under capital scarcity, rank by priority: profit times confidence, divided by execution risk times a term that rises as urgency falls. Fast-decaying opportunities jump the queue.

- Conflicts resolve by rule: net opposite positions in one market, fund higher priority under capital competition, shrink or reject when a risk limit binds.

- Risk governors are non-negotiable and override the optimization: kill switch at 15 percent drawdown, 2 percent per-trade cap, 10 percent per-market cap, pause above 30 percent fill failures, shrink the window on solver timeouts. They do not raise returns; they keep you solvent, which is the operational edge.