9.35 Kelly When Price ≠ Probability: Why the Gap Persists

A prediction-market price is not a probability. It is where capital-weighted Kelly bets cancel. You bet the gap, not the belief, and getting the probability wrong costs more than mis-sizing.

Open Polymarket's own help page and it tells you the price is the probability. "Prices (odds) on Polymarket represent the current probability of an event occurring." That sentence is wrong, and it is wrong for a reason that has nothing to do with manipulation, wash trading, or dumb money. It is wrong because the people setting the price are sizing their bets with logarithmic utility, and log-utility does not clear a market at the average belief. It clears it somewhere else. A short 2024 paper by Bernhard Meister works out exactly where, and the answer is that the gap between price and probability is a structural feature of how rational bettors allocate capital, not a bug you can arbitrage away.

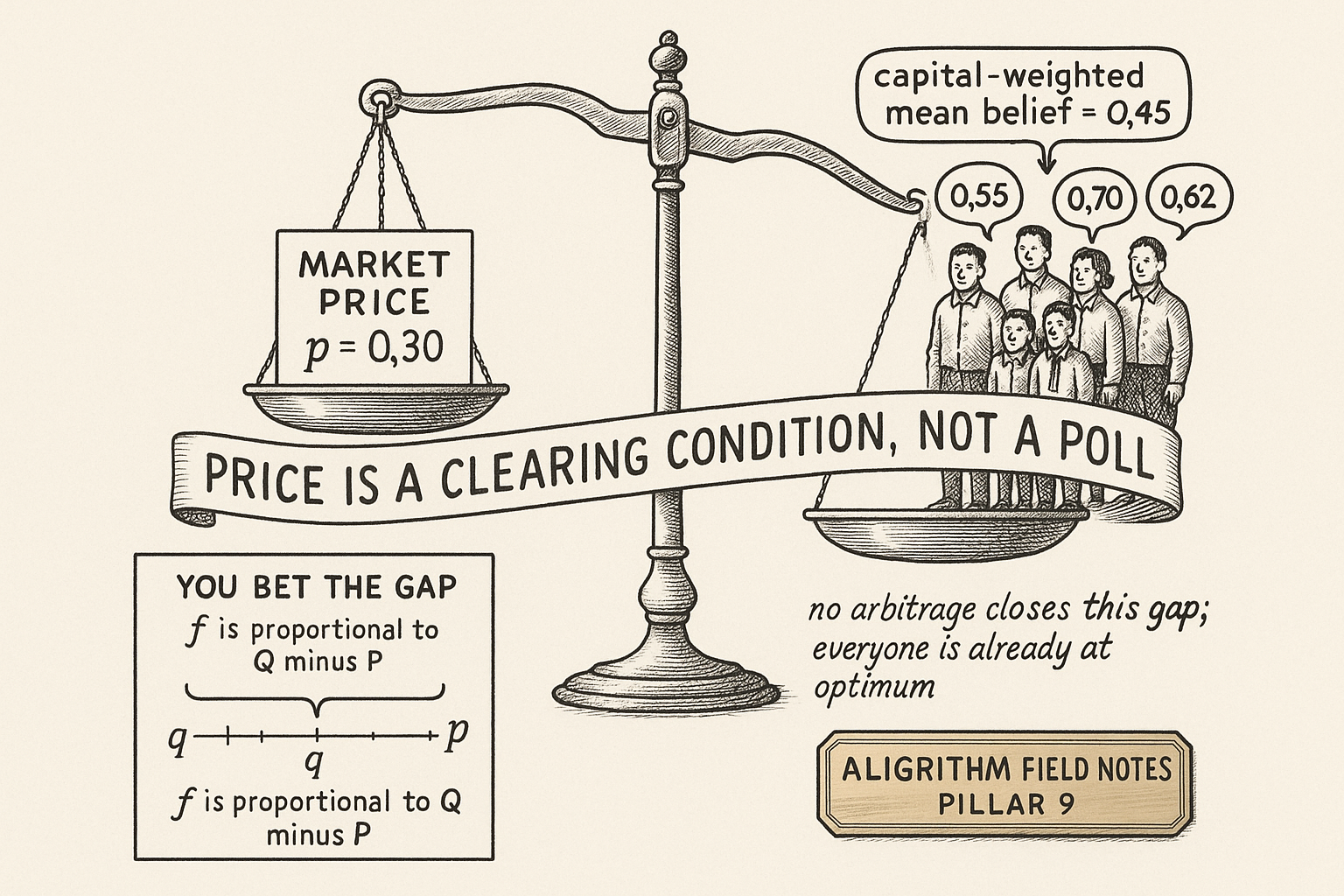

This matters because the whole appeal of prediction markets rests on the claim that the price is a forecast. If a contract trades at 0.30, the pitch is that the event has a thirty percent chance. Meister's point is that a room full of Kelly bettors will push that price to 0.30 even when their capital-weighted average belief is 0.45. The price is a clearing condition, not a poll. This article walks through the optimal fraction that produces the gap, the two-investor toy that shows how wide it gets, and the finite-horizon result that should worry anyone trading these: getting the probability wrong costs you more than getting the bet size wrong.

The fraction you should bet is the gap, not the belief

Start with one contract. It costs p to buy, pays one dollar if the event happens, zero otherwise. You believe the true probability is q. You cannot borrow and you cannot go naked short. A log-utility maximizer picks the fraction f of bankroll that maximizes expected log wealth.

$$ U(q, p, f) = (1-q)\log(1-f) + q\log\!\left(1 + f\,\frac{1-p}{p}\right) $$

The first term is the log of what you keep if the event fails, weighted by your belief it fails. The second is the log of what you hold if it happens, where the payout multiplier is one minus p over p, the odds the market is offering. Maximize over f and the answer collapses to something clean.

$$ f = q - p\,\frac{1-q}{1-p} = \frac{Q - P}{1 + Q}, \qquad P = \frac{p}{1-p}, \quad Q = \frac{q}{1-q} $$

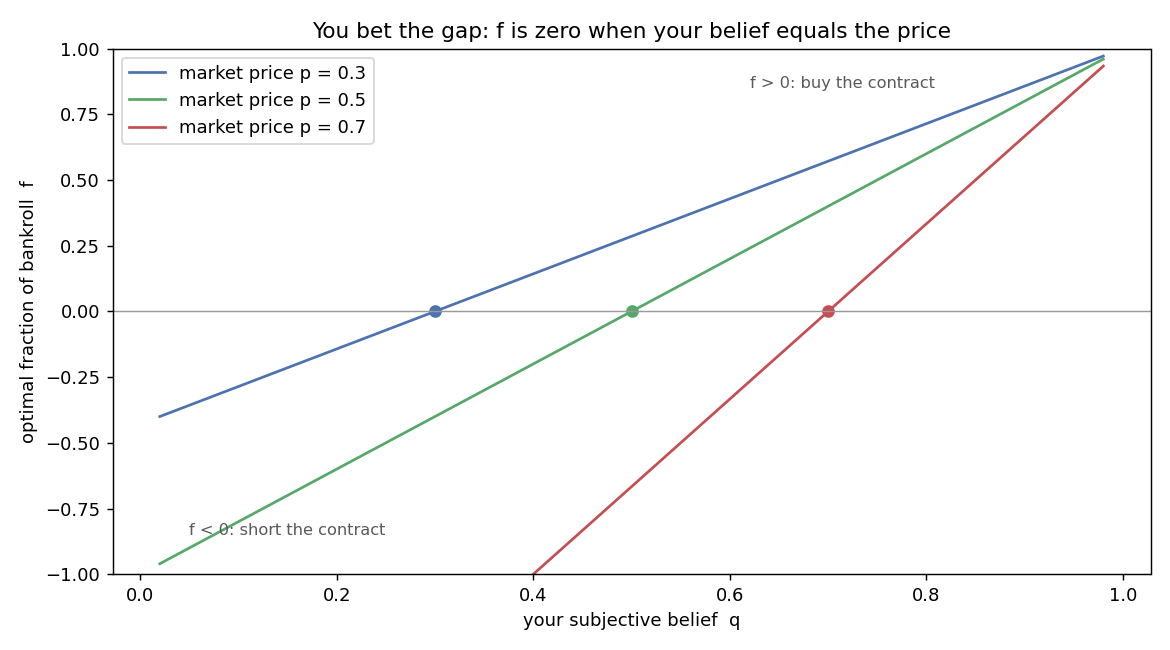

Read the right-hand form. Capital-P is the market's odds, capital-Q is your odds. You bet a fraction proportional to the gap between your odds and the market's odds. Work a number: the contract trades at p equal to 0.40, you believe q equal to 0.60. Then P is 0.40 over 0.60, about 0.667, and Q is 0.60 over 0.40, which is 1.5. The fraction is 1.5 minus 0.667, over 1 plus 1.5, which is 0.833 over 2.5, about 0.333. You put a third of your bankroll long.

Now set your belief equal to the price, q equal to p. Then Q equals P, the numerator is zero, and f is zero. You bet nothing. This is the whole thesis in one line. You do not bet because you think the event is likely. You bet because your probability differs from the price, and you bet the gap. The old article "Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't" made the same point from the stock-market side: Kelly hands you a zero when the edge is gone. Here the edge is literally the distance between q and p.

The figure draws f against your belief for three fixed prices. Each line crosses zero exactly at its price and tilts positive above, negative below. When your belief sits under the price you want to short the contract, and the no-short rule in real binary markets is why platforms list a mirror contract instead. The slope also changes with the price, and that asymmetry is what pries price and probability apart.

Why the crowd's average belief is not the price

Meister defines the mean belief honestly: the capital-weighted average of everyone's subjective probability. Investor i brings capital C-i and belief q-i, so the mean belief is the sum of C-i times q-i. Their position in the market is C-i times their fraction f-i. The market clears when those positions net to zero.

$$ \sum_{i=1}^{N} C_i\, f_i(p, q_i) = 0 $$

In plain terms: the price p is whatever value makes all the Kelly bets cancel. Longs equal shorts in capital terms. Nothing in that condition forces p to equal the capital-weighted mean belief, because each f-i is a nonlinear, asymmetric function of p. To see how far apart they can drift, take the simplest possible market: two investors, one of them dead certain, the other with belief q. Solve the clearing condition for the case where the confident investor is certain the event will not happen, and the capital-weighted expectation lands at

$$ E_-(q_1^-, p) = \frac{1-p}{\,q_1^- - 2p + 1\,}\, q_1^- $$

Work it. Say the price is p equal to 0.30, and the second investor genuinely believes q equal to 0.70. Plug in: the numerator is 0.70 times 0.70, which is 0.49; the denominator is 0.70 minus 0.60 plus 1, which is 1.10. The mean belief is 0.445. So the capital-weighted crowd believes 0.445, but the market prints 0.30. That is a fourteen-point gap with only two rational participants and no manipulation. Meister shows the mean belief in this setup can range across the whole interval from 0 to one-half whenever the price sits below one-half. Flip the confident investor to certain-yes and the algebra gives the mirror result, with the expectation pinned back at p. The lesson is not the exact number, it is that a market can clear at a price nowhere near what its own participants, on average and weighted by their money, actually believe.

This is a different failure than the incoherence the old article "The Dutch Book Theorem, Plainly, and Why Polymarket Will Always Have Arbitrage" described. There the prices across related contracts violated the probability axioms and left a standing arbitrage. Here a single price is internally fine, it just is not the average belief, and no arbitrage closes the gap because every bettor is already at their optimum. You cannot trade against rationality.

Bending the payout to pull liquidity

If the gap is a product of the payout structure, you can change the payout structure. Meister floats a one-parameter deformation: raise the market's odds multiplier to a power alpha.

$$ U_\alpha(q, p, f) = (1-q)\log(1-f) + q\log\!\left(1 + f\left(\frac{p}{1-p}\right)^{\!\alpha}\right) $$

At alpha equal to one you recover the standard contract. Push alpha below one and the payout near the extremes gets compressed, so a high-probability bet with a normally tiny relative payout becomes more attractive; a bettor who would otherwise ignore a contract priced at 0.95 now has a reason to size into it. Push alpha above one and you do the opposite. The practical idea is that an exchange sitting on a lopsided market, price hugging a boundary where liquidity dries up, could tune alpha to make the unloved side worth trading and pull depth back in.

Be skeptical about how far this goes, and Meister is. He calls it explicitly not a panacea: the moment the market flips toward the other boundary, the same deformation that attracted liquidity now repels it, and depth drains from the side you just starved. He also notes the full effect on the price-belief gap requires working through several cases he defers to a later paper. So treat alpha as a suggestive knob, not a solved market-design fix. It shows the gap is a function of contract terms, which is the useful insight, without pretending anyone has found the right terms.

Finite time is where the theory bites

Kelly's guarantee is asymptotic. Over infinite rounds the log-optimal bettor beats every other strategy with probability one. Nobody trades infinite rounds. Meister models the finite case as a biased coin flipped N times, k of them favorable, and asks how likely you are to fall short of a growth target. The tail probability of too few favorable steps is bounded by the Chernoff inequality, whose exponent is the Kullback-Leibler divergence.

$$ F(k, N, p) \le e^{-N\,D\!\left(\frac{k}{N}\,\middle\|\,p\right)}, \qquad D\!\left(\frac{k}{N}\,\middle\|\,p\right) = \frac{k}{N}\log\frac{k}{pN} + \left(1-\frac{k}{N}\right)\log\frac{1-\frac{k}{N}}{1-p} $$

The left side is the probability that you get k or fewer favorable steps out of N. The bound says that probability decays exponentially in N, at a rate set by the KL divergence D between the fraction you need, k over N, and the true bias p. Work it: a favorable coin with p equal to 0.55, over N equal to 100 flips, and you want to know the odds of ending underwater with 45 or fewer wins, so k over N is 0.45. The divergence is 0.45 times log of 0.45 over 0.55, plus 0.55 times log of 0.55 over 0.45, which comes to about 0.020. The bound is e to the minus 100 times 0.020, which is e to the minus 2.0, about 0.135. Even with a real edge, you have roughly a one-in-seven chance of a hundred-flip stretch leaving you behind. That is the finite-horizon reality the asymptotic theorem hides.

The asymmetry that should change how you trade

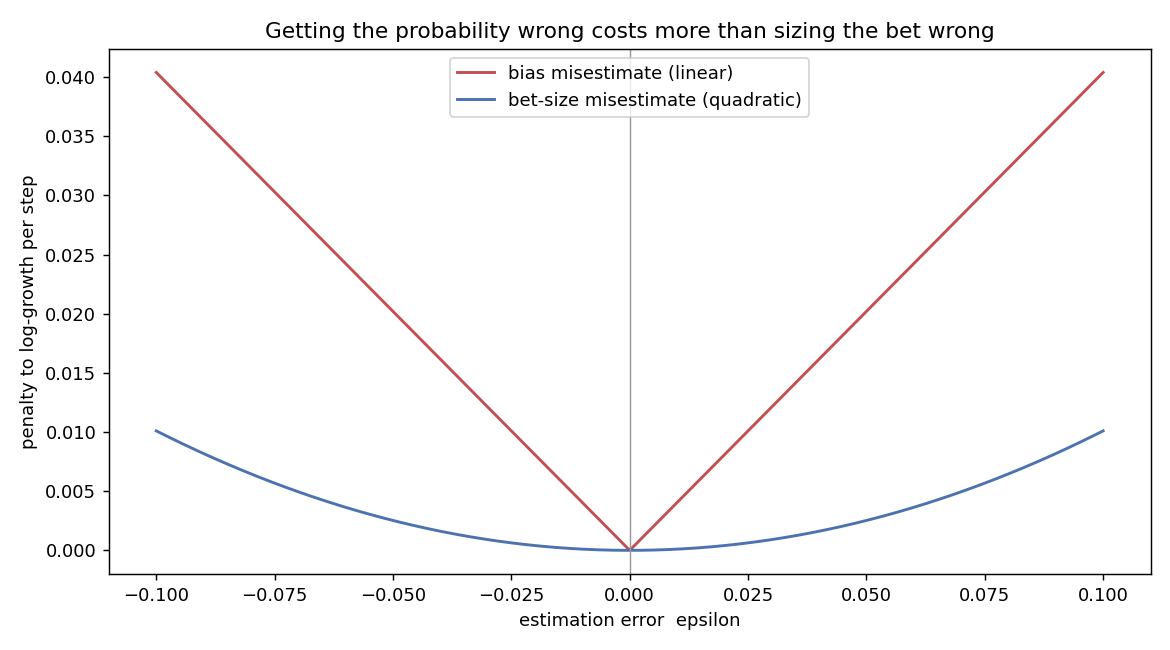

Now the result worth the whole paper. Meister perturbs the growth calculation two ways and compares the leading terms. First, hold your bet size fixed and get the probability wrong by a small amount epsilon. The change in the divergence, which controls your achievable growth, is linear in epsilon.

$$ D\!\left(\frac{k}{N}\,\middle\|\,p+\epsilon\right) - D\!\left(\frac{k}{N}\,\middle\|\,p\right) = \frac{p - \frac{k}{N}}{p(1-p)}\,\epsilon + O(\epsilon^2) $$

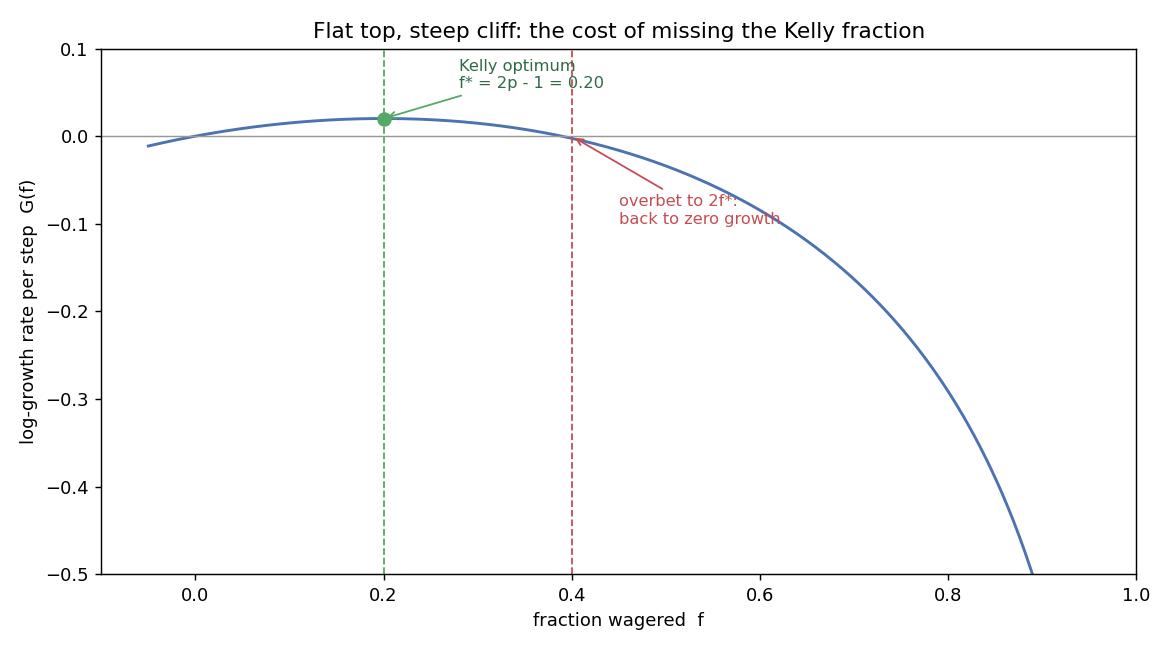

Second, hold the probability fixed and get the bet fraction wrong by epsilon, around the optimum f-star equal to 2p minus 1. The change in the growth rate is quadratic.

$$ U(p,\, 2p-1+\epsilon) - U(p,\, 2p-1) = -\frac{1}{4(1-p)p}\,\epsilon^2 + O(\epsilon^3) $$

Put the two side by side. A probability error hits you at first order; a bet-size error only at second order. Work the numbers with p equal to 0.55 and k over N equal to 0.45. The bias slope is 0.55 minus 0.45, over 0.55 times 0.45, which is 0.10 over 0.2475, about 0.40. So an epsilon of 0.02 in your probability estimate costs about 0.008 per step, linearly. The bet-size penalty coefficient is one over four times 0.55 times 0.45, about 1.01, so the same 0.02 error in fraction costs only 1.01 times 0.0004, about 0.0004 per step. The probability mistake is roughly twenty times more expensive at that scale.

The figure makes the ranking visual. Near zero error the quadratic bet-size curve is almost flat while the linear bias curve climbs immediately. This is the same flat-topped growth curve the old article "The Overbet Runs Through Everything" traced across shrinkage, asymmetry, and anti-patterns: the penalty for missing the Kelly fraction is quadratic, so small sizing errors barely register.

That flat top is exactly why practitioners bet half-Kelly and sleep fine: giving up a little size costs almost nothing in growth but slashes variance. Meister's contribution is to put the other error on the same axes and show it is worse. Fine-tuning your stake is second-order comfort. The first-order danger is your probability estimate, and in a prediction market that estimate is what you are supposedly better at than the crowd. If you are not, the market's price, gap and all, will take your money at linear speed while you fuss over bet sizing at quadratic speed.

Where this connects

This paper is the bridge between the Kelly pillar and the prediction-market pillar. The optimal fraction f equal to the gap over one plus your odds is the same Kelly logic the old article "Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't" laid out, specialized to a contract whose price is bounded above as well as below. The linear-versus-quadratic asymmetry is the growth-penalty geometry from the old article "The Overbet Runs Through Everything," now carrying a second lesson: the overbet penalty is quadratic, but the probability-estimate penalty is linear, so estimation error dominates sizing error.

The practical takeaway is a warning about reading prices. A prediction-market price is a capital-weighted clearing point for log-utility bettors, not a probability, and the gap does not vanish because it is nobody's mistake. If you are going to trade these, spend your effort on the probability, because that is the error the math punishes first and hardest, and treat any exchange's claim that "price equals probability" as marketing rather than mathematics.

KEY POINTS

- A prediction-market price is not the probability. It is the point where capital-weighted Kelly bets cancel, and log-utility does not clear at the average belief.

- You bet the gap, not the belief. The optimal fraction is f equals Q minus P over one plus Q, where P and Q are the market's and your odds. When your belief equals the price, you bet exactly zero.

- The price-belief gap is structural, not an arbitrage. A two-investor toy market with one certain participant prints a price of 0.30 while the capital-weighted mean belief is 0.445, and no trade closes it because everyone is already optimal.

- Bending the payout with a power alpha can pull liquidity toward an unloved boundary, but it is explicitly not a panacea: flip the market and the same knob drains depth from the other side.

- Finite horizons kill the Kelly guarantee's comfort. Even a real edge, p equal to 0.55 over 100 flips, leaves roughly a one-in-seven chance of ending behind, bounded by a Chernoff exponent equal to the KL divergence.

- The asymmetry that matters: misjudging the probability hurts growth at linear order, mis-sizing the bet only at quadratic order. Getting the probability wrong is roughly twenty times more expensive than the same-sized bet error in the worked case.

- Trade accordingly. Half-Kelly sizing is cheap insurance because the growth top is flat, but your probability estimate is where the money is won or lost.

References

- A New Interpretation of Information Rate (Kelly, 1956)

- Interpreting the Predictions of Prediction Markets (Manski, 2004)

- Prediction Markets (Wolfers and Zitzewitz, 2004)

- Interpreting Prediction Market Prices as Probabilities (Wolfers and Zitzewitz, 2006)

- A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins (Meister and Price, 2024)

- Application of the Kelly Criterion to Prediction Markets (Meister, 2024)

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.